Understanding Economics: Demand, Supply, and Equilibrium

Explore the fundamental concepts of economics, including the nature and scope of economics, demand, and its determinants. Learn about normative and positive economics, microeconomics, macroeconomics, and the factors affecting demand such as income, price of the good, and complementary goods. Gain insights into how economic agents make decisions based on their willingness and ability to pay for goods and services in various economic scenarios.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. Download presentation by click this link. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

E N D

Presentation Transcript

INTRODUCTION TO ECONOMICS: DEMAND, SUPPLY, EQUILIBRIUM PRESENTATION FOR ECONOMICS HONOURS STUDENTS, SEMESTER I

CONCEPTS: NATURE OF ECONOMICS Traditional economic theory has developed along two concepts; (1) Normative and (2) Positive. Normative economics focuses on prescriptive statements, and help establish rules aimed at attaining the specified goals of business. Positive economics focuses on description it aims at describing the manner in which the economic system operates without staffing how they should operate.

CONCEPTS: SCOPE OF ECONOMICS Microeconomics Macroeconomics: International economics Public finance Development economics Health economics Environmental economics Urban and rural economics 1. 2. 3. 4. 5. 6. 7. 8.

DEMAND In economics, demand is the utility for a good or service of an economic agent, relative to his/her income. Demand is a buyer's willingness and ability to pay a price for a specific quantity of a good or service. Demand refers to how much (quantity) of a product or service is desired by buyers at various prices.

DETERMINANTS OF DEMAND 1. Income: Income is one of the factors that affect the demand for a given product. Normally, we expect that as one's income rises (falls), the demand for a product will rise (fall). This statement is true in case of normal good. Occasionally, this statement is not true for some goods. These goods are called inferior goods; for these goods, as income rises (falls), the demand for the product falls (rises).

DETERMINANT OF DEMAND (CONTD.) 2. Price of the good: If the price of a good increases, its demand falls and if price decreases, demand increases. So, there is inverse relationship between price of a commodity and its demand However, this statement does not hold in case of Giffen good. In this case, the relationship is positive.

DETERMINANT OF DEMAND (CONTD.) 3. Price Complementary good: Substitutes are different goods that compete with the one under consideration. Tea and Coffee are substitutes. As the price of the substitute rises (falls), the demand for the product rises (falls). Complements are goods that are consumed together. Tea & Sugar are complements. As the price of the complement rises (falls), the demand for the product falls (rises). of Substitute Good and

DETERMINANT OF DEMAND (CONTD.) 4. Tastes or Preferences: Tastes or Preferences involves the fact that there are certain psychological reasons for liking or disliking a particular good. Our principle is: the more (less) we like a good or service, the greater (less) is our demand for it

DETERMINANT OF DEMAND (CONTD.) 5. Expectations The buyer expects the price to rise. If buyers expect the price to rise (fall), the demand rises (falls) today. If one expects that the product will soon be out of market, the demand will rise. If one expects that his income will fall, the demand for most products will fall. 6. Population The last of the factors affecting demand is the population (number of buyers). Therefore, if there are more buyers, there must be more market demand.

MEANING OF SUPPLY In economics, supply refers to the amount of a product that producers and firms are willing to sell at a given price when all other factors being held constant.

DETERMINANT OF SUPPLY 1. Number of Sellers Greater the number of sellers, greater will be the quantity of a product or service supplied in a market and vice versa. Increase in number of sellers increases supply and shift the supply curve rightwards whereas decrease in number of sellers decrease the supply and shift the supply curve leftwards.

DETERMINANT OF SUPPLY (CONTD.) 2. Technology Improvement efficient production of goods and services. Reducing the production costs and increasing the profits. As a result supply is increased and supply curve is shifted rightwards. in technology enables more

DETERMINANT OF SUPPLY (CONTD.) 3. Suppliers' Expectations Change in expectations of suppliers about future price of a product or service may affect their current supply. When farmers suspect the future price of a crop to increase, they will withhold their agricultural produce to benefit from reducing the supply. When manufacturers expect the future price to increase, they will employ more resources to increase their output and this may increase current supply as well. higher price thus

DETERMINANT OF SUPPLY (CONTD.) 4. Selling Price: Selling price is decided after adding certain amount of profit in the cost. If selling price is increased, the profit will also increases. This increase the profit of the seller, which motivates to supply more quality .So, increase in selling price increase the supply of good. 5. Price of Raw Material: Price of raw materials directly effects the quality supplied in the market. If the prices of raw materials increases, the seller will produce less amount of goods and consequently, the quantity of supply gets reduced.

LAW OF DEMAND The law of demand states that, all other factors determining demand remaining constant, as the price of a product increases, quantity demanded falls and as the price of a product decreases, quantity demanded increases.

LAW OF SUPPLY The law states that, all other factors determining supply remaining constant, as the price of a product increases, quantity demanded falls and as the price of a product decreases, quantity demanded increases.

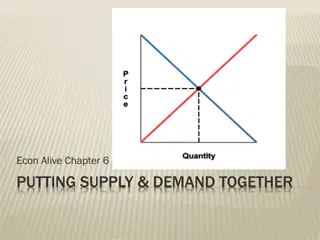

EQUILIBRIUM When supply and demand are equal (i.e. when the supply function and demand function intersect) the economy is said to be at equilibrium. At this point, the allocation of goods is at its most efficient because the amount of goods being supplied is exactly the same as the amount of goods being demanded.

EQUILIBRIUM (CONTD.) Equilibrium occurs at the point of intersection of demand and supply curves.

EQUILIBRIUM (CONTD.) At this point, the price of the goods will be P* and the quantity will be Q*. These are known as equilibrium price (P*) and quantity (Q*). Even if there is deviation from equilibrium, with time equilibrium will be re-attained. However, in real markets, equilibrium can never be reached, so the prices of goods and services are constantly changing in relation to fluctuations in demand and supply.

")

")

")

")

")

")

")

")

")