Understanding Supply and Demand in Economics

undefined

undefined

Economics – Unit 2

Supply and Demand

Law of Supply

Law of Demand

Remember Market Systems? - Market Economy

What are the characteristics of Free Markets?

What is Supply and Demand?

Supply

How much the market can offer

At $1,000 per iPhone, Apple can

supply 50,000 iPhone 11s.

Demand

How much (quantity) of a product or

service is desired by

buyers (consumers)

Willing and able to purchase a product

at a particular price

How many iPhone 11s does the public

want at $1,000?

Law of Supply

•

As a good's price increases (goes up) the quantity suppliers are willing and able to supply

increases.

A new toy at Christmas time... price increases, and there are more of the certain toy to buy.

•

As a good's price decreases, (goes down) the quantity suppliers are willing and able to

supply decreases.

Apple's iPhone 8.... price drops, Apple does not make too many more, supply drops

•

Quantity supplied is usually directly related to its price

•

So... If the price increases, supply increases... vice versa If the price decreases, supply

decreases.

•

Producers supply more at a higher price because selling a higher quantity at a higher

prices increases

revenue

.

Supply or

Demand

schedule

•

Displays the quantity of

the product supplied or

demanded at each price

Supply curves

•

Graphic representation

of the quantities of a

good supplied at various

prices.

•

Low price, low quantity

of the item

•

High price, high supply

of the item

Factors that determine SUPPLY

•P.I.G. T.O.E.S”

•

•– P roductivity (workers, machines, and/or assembly)

•

•– I nputs (Change in the price of materials needed to make the

•

•good)

•

•– G overnment Actions (Subsidies, Taxes, and Regulations)

•

•– T echnology (Improvements in machines and production)

•

•– O utputs (Price changes in other products)

•

•– E xpectations (outlook of the future)

•

•– S ize of Industry (Number of companies in the industry)

Law of Demand

•

If all other factors remain equal, the higher the price of a good, the less people will demand that

good

•

The higher the price the lower the quantity demanded

•

As the price of a good goes up, so does the opportunity cost of buying that good.

•

People will naturally avoid buying a product that will force them to not buy something else they

value more.

•

Higher prices drive potential consumers from the market if their resources do not allow them to

even consider a purchase.

•

Will you buy the $1,00 iPhone 11 or spend that $1,000 elsewhere?

•

At a high price, there is not much demand for the product

Demand Curve

•

High price, low demand

•

Low price, more

demand

Factors which determine DEMAND

•

“P.O.I.N.T.”

•

•– P rice of other goods (substitute or complementary)

•

•– O utlook (consumer expectation of the future)

•

•– I ncome (normal goods versus inferior goods)

•

•– N umber of potential customers (pop.of market)

•

•– T aste (fads or trends)

Supply and Demand

Relationship

•

Excess Supply =

Surplus

•

If price is too high, excess supply will be created

•

Excess Demand =

Shortage

•

Price is too low – too many consumers want the

good

Law of Supply and

Demand

a quick view

Equilibrium

Price

•

Supply and demand are

equal

•

Allocation of goods is at

its most efficient

•

Sellers are selling all the

goods they produced and

consumers are getting all

the goods that they

demand

Why would

a supply

curve

"shift"?

Causes of

a Supply

Shift

Why would

a supply

curve

"shift"?

Causes of

a Supply

Shift

Causes of Demand Shifts

•

Price right?

•

Yes

•

Higher price, less demand

•

Lower price, more demand

•

All can cause a sift in the demand curve

•

BUT...... There are other variables other than price

•

If the price stays constant......

Causes of

Demand

Shift with a

Constant

Price

(Market

variables

other than

price)

•

Change in taste & preference – things go out

of style

•

Change in the number of consumers –

change in population in an area

•

Change in price in related goods

•

Complementary product – new iPhone 11 cover

for new iPhone 11; old covers decrease because of

a new complementary product to the new product

•

Supplementary product – Roku stick (cheaper)

instead of Amazon stick (more expensive)

Causes of

Demand

Shift with a

Constant

Price

(Market

variables

other than

price)

•

Change in income levels

•

I get paid more; I want a Lexus instead of a

Honda

•

I lose my job; I eat at the diner instead of the steak

house

•

Change in expectations

•

Freeze in Florida wipes out orange crop; I'm

buying orange juice now before the price increases

Elasticity

(think rubber band)

Remember Opportunity costs?

How does it relate to Elasticity?

•

Cost of a good or service

•

Buying a prom dress $1,000

•

What can I do with the $$ instead of buying that Prom Dress?

•

Cruise on Carnival

•

Goods or Services may not be purchased because of a less of a necessity which

then makes the opportunity costs too high.

•

TV price is too high, do not need a new TV, could use one but... I need that $$ to buy food

•

Goods or services which are not as much as a necessity are more affected by

elasticity and high opportunity costs

Crash Course: Supply and Demand

Explore the fundamental concepts of supply and demand in economics, including the laws that govern them. Learn about the characteristics of free markets, the factors that determine supply, and how prices influence the quantities supplied and demanded. Gain insights into the law of supply and law of demand, supply and demand schedules, and the impact of various factors on market dynamics.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. Download presentation by click this link. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

E N D

Presentation Transcript

Economics Unit 2 Supply and Demand Law of Supply Law of Demand

Remember Market Systems? - Market Economy What are the characteristics of Free Markets? PRIVATE PROPERTY PROFIT MOTIVE FREE ENTERPRISE

What is Supply and Demand? Supply How much the market can offer At $1,000 per iPhone, Apple can supply 50,000 iPhone 11s. Demand How much (quantity) of a product or service is desired by buyers (consumers) Willing and able to purchase a product at a particular price How many iPhone 11s does the public want at $1,000?

Law of Supply As a good's price increases (goes up) the quantity suppliers are willing and able to supply increases. A new toy at Christmas time... price increases, and there are more of the certain toy to buy. As a good's price decreases, (goes down) the quantity suppliers are willing and able to supply decreases. Apple's iPhone 8.... price drops, Apple does not make too many more, supply drops Quantity supplied is usually directly related to its price So... If the price increases, supply increases... vice versa If the price decreases, supply decreases. Producers supply more at a higher price because selling a higher quantity at a higher prices increases revenue.

Supply or Demand schedule Displays the quantity of the product supplied or demanded at each price

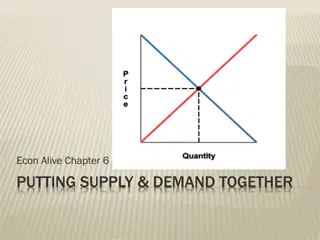

Supply curves Graphic representation of the quantities of a good supplied at various prices. Low price, low quantity of the item High price, high supply of the item

Factors that determine SUPPLY P.I.G. T.O.E.S P roductivity (workers, machines, and/or assembly) I nputs (Change in the price of materials needed to make the good) G overnment Actions (Subsidies, Taxes, and Regulations) T echnology (Improvements in machines and production) O utputs (Price changes in other products) E xpectations (outlook of the future) S ize of Industry (Number of companies in the industry)

Law of Demand If all other factors remain equal, the higher the price of a good, the less people will demand that good The higher the price the lower the quantity demanded As the price of a good goes up, so does the opportunity cost of buying that good. People will naturally avoid buying a product that will force them to not buy something else they value more. Higher prices drive potential consumers from the market if their resources do not allow them to even consider a purchase. Will you buy the $1,00 iPhone 11 or spend that $1,000 elsewhere? At a high price, there is not much demand for the product

Demand Curve High price, low demand Low price, more demand

Factors which determine DEMAND P.O.I.N.T. P rice of other goods (substitute or complementary) O utlook (consumer expectation of the future) I ncome (normal goods versus inferior goods) N umber of potential customers (pop.of market) T aste (fads or trends)

Supply and Demand Relationship Excess Supply = Surplus If price is too high, excess supply will be created Excess Demand = Shortage Price is too low too many consumers want the good

Law of Supply and Demand a quick view

Equilibrium Price Supply and demand are equal Allocation of goods is at its most efficient Sellers are selling all the goods they produced and consumers are getting all the goods that they demand

Change in the price of resources costs go down, price goes down to capture a larger market OR costs go up, price goes up to maintain profit Why would a supply curve "shift"? Causes of a Supply Shift Change in the number of producers more producers = more supply or less producers = less supply Change in technology better technology =more efficient production more supply

Why would a supply curve "shift"? Causes of a Supply Shift Government Intervention new taxes (decrease in supply), subsides (increase in supply), regulations will affect supply Change in Expectations producers change their decision on what to produce based on expectations of change. Ex: more winter jackets ahead of winter-time.

Causes of Demand Shifts Price right? Yes Higher price, less demand Lower price, more demand All can cause a sift in the demand curve BUT...... There are other variables other than price If the price stays constant......

Change in taste & preference things go out of style Change in the number of consumers change in population in an area Change in price in related goods Complementary product new iPhone 11 cover for new iPhone 11; old covers decrease because of a new complementary product to the new product Supplementary product Roku stick (cheaper) instead of Amazon stick (more expensive) Causes of Demand Shift with a Constant Price (Market variables other than price)

Causes of Demand Shift with a Constant Price (Market variables other than price) Change in income levels I get paid more; I want a Lexus instead of a Honda I lose my job; I eat at the diner instead of the steak house Change in expectations Freeze in Florida wipes out orange crop; I'm buying orange juice now before the price increases

Elasticity (think rubber band) Inelastic good or service change in price may not throw off the quantity demanded or supplied of the product Common definition degree to which a demand or supply curve reacts to a change in price Highly elastic slight change in price leads to a sharp in quantity demanded or supplied Usually more of a day to day necessity god or service (milk) Product is available on the market but may not be needed daily (TV)

Remember Opportunity costs? How does it relate to Elasticity? Cost of a good or service Buying a prom dress $1,000 What can I do with the $$ instead of buying that Prom Dress? Cruise on Carnival Goods or Services may not be purchased because of a less of a necessity which then makes the opportunity costs too high. TV price is too high, do not need a new TV, could use one but... I need that $$ to buy food Goods or services which are not as much as a necessity are more affected by elasticity and high opportunity costs