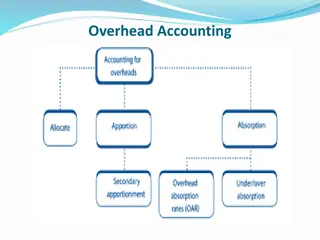

Absorption Costing and Overhead Absorption in Cost Accounting

Absorption costing is a method that includes direct costs and a fair share of production overhead costs in the cost of a product. Overhead absorption rate (OAR) is calculated using budgeted figures and can lead to over/under-absorption. Over-absorption occurs when absorbed overhead is more than actual, while under-absorption is the opposite. This impacts profit calculations in financial statements.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

You are allowed to download the files provided on this website for personal or commercial use, subject to the condition that they are used lawfully. All files are the property of their respective owners.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.

E N D

Presentation Transcript

2 Traditional Costing Chapter

Chapter Content Absorption Costing Marginal Costing Traditional Costing Pricing

Absorption costing Absorption costing is a method of costing in which the cost of a product is built up as the sum of direct costs and a fair share of production overhead cost A fully absorbed cost is used to value inventory and as a basis for pricing Overheads are absorbed across all units using a single cost driver (usually machine or labour hours). Results in a FULL product cost per unit Is an acceptable inventory valuation method as per IAS 2 Suitable costing system for mass produced, homogeneous products - where overheads are largely volume driven.

Standard cost card-Absorption costing $ x x x x x Direct materials Direct labour Variable overheads Fixed production overheads Absorption cost per unit OAR

Overhead Absorption Rate (OAR) The OAR is calculated using budgeted figures; OAR = Budgeted Fixed Production Overheads The activity could be based on labour hours, machine hours or sometimes number of units. The choice of activity will depend on whether the operation is labour intensive or machine intensive. Once the OAR has been ascertained, absorption occurs as soon as a unit is made. Every unit will absorb the same amount in respect of production overheads Fixed production overheads are absorbed into units using the OAR. Budgeted level of activity

Over/under-absorption Because the OAR is based on budgeted figures it is highly likely that the overhead absorbed during a period may be different from the actual overhead incurred An over-absorption will occur when the absorbed overhead is more than the actual overhead incurred. Under-absorption is when the absorbed overhead is less than the actual overhead incurred. An over-absorption has the effect of understating profits and therefore it is added back to Gross profit in the statement of profit or loss Under-absorptions overstate profits and they are therefore subtracted fro gross profit

Example: under-absorption Identify which of the following statements would be true: fixed production overheads will always be under-absorbed when: A actual output is lower than budgeted output B actual overheads incurred are lower than budgeted overheads C overheads absorbed are lower than those budgeted D overheads absorbed are lower than those incurred

Example.. A company uses a standard absorption costing system. The fixed overhead absorption rate is based on labour hours. Extracts from the company s records for last year were as follows: Fixed production overhead Output Labour hours Budget $450,000 50,000 units 900,000 930,000 Actual $475,000 60,000 units The ______ (choose between 'over' and 'under') absorbed fixed production overheads for the year were $______ (fill in the value).

Proforma of Income Statement Sales Less full production cost of goods sold Opening inventory + Production - closing inventory Gross profit x (x) x x x (x) Over absorption Under absorption Less Variable sales and distribution Fixed non production x (x) (x) (x) Profit/(loss) x/(x)

In a month when actual production was 2,400 units and exceeded sales by 180 units, what is the profit reported under absorption costing?

Marginal Costing costs per unit. Fixed cosys are treated as a period cost and subtracted in full in the income statement Standard cost card Direct materials Direct labour Variable overheads Marginal cost Inventories and production are valued at the variable production $ x x x x Contribution is emphasised.

Contribution Contribution = Sales Less Variable Costs Variable Overheads Direct Materials Direct Labour

Proforma of Income Statement Sales Less variable production cost of goods Opening inventory + Production - closing inventory Gross contribution x (x) x x x (x) Less non production variable cost [sales commission etc] Contribution Less fixed cost Production Non-production (x) x (x) x x Profit/(loss) x/(x)

In a month when actual production was 2,400 units and exceeded sales by 180 units, what is the profit reported under marginal costing?

Reconciliation of profits The only difference between the two approaches is the value of inventories. Absorption costing values inventory at a higher value as it includes the fixed production overhead in the standard cost card. Therefore: increased closing inventory increases current period s profit compared with marginal costing because more fixed cost is deferred to the next period as opening stock. decreased inventory decreases current period s profit compared with marginal costing because more fixed cost is released in the current period.

Differences in profit 1. If Opening Stock > Closing Stock then MC Profit > AC Profit 2. If Opening Stock < Closing Stock then MC Profit < AC Profit 3. If Opening Stock = Closing Stock then MC Profit = AC Profit Difference in profit = (opening closing stock) x FOAR

Solution.. a. OAR = $5000/1000 = $5/unit profit per unit = 50 15 10 5 5 = $15 total profit = 1000 x 15 = $15,000 b. contribution/unit = 50 15 10 - 5 = $20 total contribution = $20 x 1000 = $20,000 profit = $20,000 - $5000 = $15,000 As expected, if opening stock = closing stock, the profits for the period will be the same

Example.. A company produces a single product called the Genie. Budgeted output for August is 30,000 units. Budgeted fixed production costs for the month were $150,000. Opening stock was 6000 units and closing stock was 4200 units. Profit reported under marginal costing was $165,000. What would be the profit reported using absorption costing?

Pricing using absorption costing Add a mark up to total budgeted factory cost Key advantages ensures all production costs are covered can be used to justify price rises Key disadvantages ignores customers and competitors doesn t reflect the incremental cost of new orders

Pricing using marginal costing Add a mark up to the variable production cost Key advantages useful for incremental orders avoids arbitrary overhead allocations Key disadvantages ignores customers and competitors doesn t cover all costs in the long run

Mark-up and margin A margin is a % on sales A mark-up is a % on cost E.g . If a baker s margin is 20%, what is her mark-up?

")