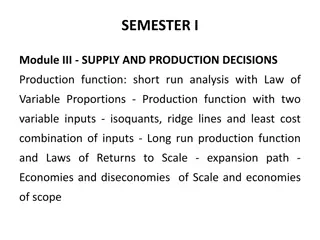

Understanding the Law of Supply in Economics

The Law of Supply states that as the price of a good or service increases, the quantity supplied by producers also increases, assuming all other factors remain constant. This fundamental economic principle highlights the relationship between price and supply, emphasizing how producers strive to maximize profits in response to price changes. The concept of ceteris paribus underscores the assumptions on which the Law of Supply is based, including the constancy of factors like technology, production costs, and market conditions.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. Download presentation by click this link. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

E N D

Presentation Transcript

Law of Supply Law of supply in economics states that supply will increase as price increases, due to the fact that producers want to maximize profits. In this instance, the law assumes that all other factors are equal and price is the only independent element, meaning supply is completely dependent on the price. The concept of "quantity supplied" refers to the amount of the item that is available. Quantity has a close relationship with the price of the item. According to supply law, the quantity supplied will decrease when price decreases, as there's less opportunity for sellers to profit.

Assumptions of Law of Supply The phrase keeping other factors constant or ceteris paribus is used when describing the law of supply. This expression refers to the following presumptions that the law is based on: The price of other commodities is constant. The state of technology has not changed. The price of factors of production is constant. The taxation laws remain the same. The producer s objectives are constant.