Snapshot of GST Issues, JDA, Redevelopment, and Real Estate Taxation

National Conference on Indirect Taxes highlighted GST issues, Joint Development Agreements, and Redevelopment for Builders and Developers. The event presented key insights on the amended scheme of taxation for ongoing and new projects, along with the tax implications of transferring DR/TDR/FSI/Lease for residential apartments post-April 2019.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. Download presentation by click this link. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

Presentation Transcript

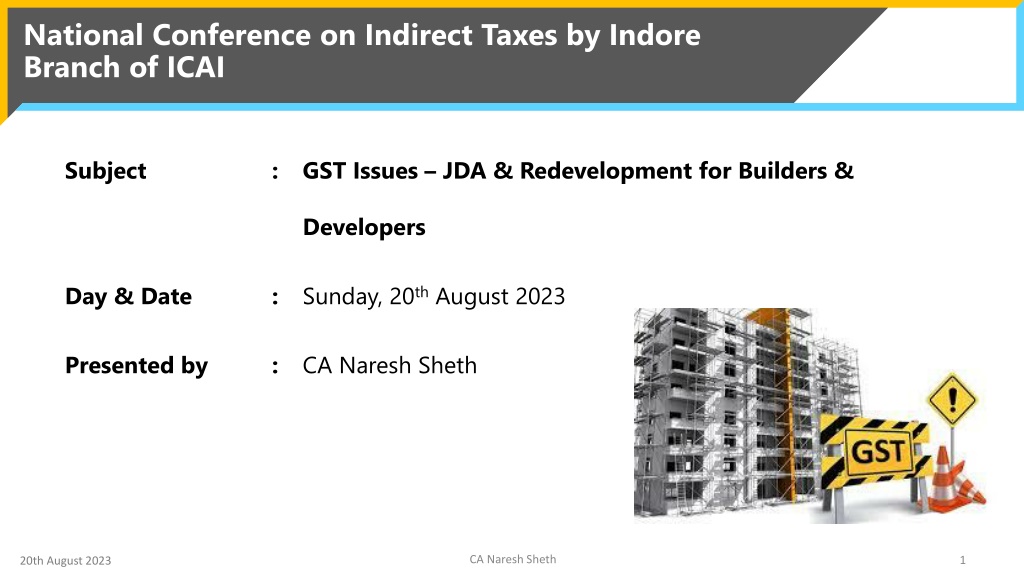

National Conference on Indirect Taxes by Indore Branch of ICAI Subject : GST Issues JDA & Redevelopment for Builders & Developers Day & Date : Sunday, 20th August 2023 Presented by : CA Naresh Sheth CA Naresh Sheth 1 20th August 2023

Snapshot of Real Snapshot of Real Estate Taxation Estate Taxation [W.e.f. 01.04.2019] [W.e.f. 01.04.2019] 20th August 2023 CA Naresh Sheth 2

Snapshot Amended Scheme of Taxation Projects Ongoing projects (Option not exercised) or New Projects - Subject to specified conditions Ongoing projects (Option exercised for old scheme) Commercial Projects: 12% With ITC Commercial Projects: 12% With ITC Residential Projects: - Affordable 1% - Non-Affordable 5% (No ITC) Residential Projects: - Affordable 8% - Non-Affordable 12% (With ITC) Mixed Projects(REP): - Res. Affordable 1% - Res. Non-Affordable 5% - Commercial 12% (Proportionate ITC) Mixed Projects(RREP): - Res. Affordable 8% - Res.Non-Affordable12% - Commercial 12% (With ITC) Mixed Projects(REP): - Res. Affordable 8% - Res.Non-Affordable12% - Commercial 12% (With ITC) Mixed Projects(RREP): - Res. Affordable 1% - Res. Non-Affordable 5% - Commercial 5% (NO ITC) Sale of completed flats/ commercial units (Post OC) Not liable to GST 20th August 2023 CA Naresh Sheth 3

Transfer of DR/TDR/FSI/Lease on or after 01.04.2019 for Construction of Residential apartments Taxability Transfer of DR / TDR / FSI / Lease used for sale of under construction residential units is exempt [Notification No. 04/2019 CT (R)] Taxable to the extent of unsold residential flats on the date of issuance of completion certificate or first occupation, whichever is earlier - presuming it is a supply (not falling under Sch. III of CGST Act) and hence leviable to tax Due date for Payment of Tax Not later than tax period in which Completion certificate is issued or First occupation in the project whichever is earlier - In area sharing, revenue sharing or outright purchase of DR/TDR/FSI/Lease [Notification No. 6/2019 CT (R) amended by Notification No. 03/2021 CT (R) dated 02.06.2021] Promoter Developer (to be paid under RCM) Person liable to pay Tax Credit of tax paid under RCM by Developer on or after 01.04.2019 New Scheme ITC not eligible; Old Scheme ITC eligible 20th August 2023 CA Naresh Sheth 4

Transfer of DR/TDR/FSI/Lease on or after 01.04.2019 for Construction of Residential apartments Tax on transfer of DR/ TDR/ FSI/Lease pertaining to unsold flats on completion of project Lower of: [Notification No. 04/2019 CT (R)] 18% on Value of DR/TDR/FSI* in proportion to carpet area of such unsold flats to total carpet area of residential flats; or 1% / 5% of Value of such unsold flats** * Valuation of DR/TDR/FSI/Lease Outright purchase: value of monetary consideration paid for outright purchase Revenue sharing: monetary consideration paid to the Landowner as revenue share; Area sharing: value of similar apartments charged by promoter from independent buyers nearest to the date of transfer of DR/TDR/FSI; **Value of unsold flats is deemed as equal to value of similar apartments charged by the promoter nearest to the date of completion certificate or first occupation, whichever is earlier 20th August 2023 CA Naresh Sheth 5

Transfer of DR/TDR/FSI/Lease on or after 01.04.2019 for Construction of Commercial apartments Taxability Due date for payment of Tax Taxable Outright purchase: Date of transfer of DR/TDR/FSI/Lease Area Sharing: Not later than the tax period in which: Completion certificate is issued; or First occupation of project. Whichever is earlier Revenue Sharing (probable views): Date of execution of DA/JDA (Value may be unascertained on such date) Actual date of payment of revenue share Completion of project Promoter Developer (to be paid under RCM) Person liable to pay Tax 20th August 2023 CA Naresh Sheth 6

Transfer of DR/TDR/FSI/Lease on or after 01.04.2019 for Construction of Commercial apartments Tax rate 18% on Value of DR/TDR/FSI/Lease Valuation of Outright purchase: value of monetary consideration paid for outright purchase DR/TDR/FSI Revenue sharing: monetary consideration paid to the Landowner as revenue share; Area sharing: value of similar apartments charged by promoter from independent buyers nearest to the date of transfer of DR/TDR/FSI; Credit of tax paid under For exclusive commercial projects - ITC is eligible [subject to reversal on completion of project u/R RCM by Developer 42] For REP ITC attributable to Commercial portion can be claimed [subject to reversal on completion of project u/R 42] For RREP (with Commercial portion less than 15%) - ITC not eligible for developer opting New scheme. However, same is eligible for developer opting Old scheme; 20th August 2023 CA Naresh Sheth 7

Implications of JDA on or after 01.04.2019 for Developer on Area allotted to Landowner/ Leaseholder Taxability: Construction of owner s apartments is a service by developer to landowner/leaseholder which is liable to GST Implications of decision of Hyderabad CESTAT in case of Vasantha Green Projects where it was held that service tax is not payable on owner s area Time of Supply: Developer shall pay tax on owner s area not later than tax period in which Completion certificate is issued or First occupation in the project whichever is earlier Value of Supply: GST to be paid on the value of total amount charged for similar apartments in the project to independent buyers nearest to the date of transfer of development rights Rate of Tax: Developer is liable to GST at 5% or 1% or 12% CA Naresh Sheth 8 20th August 2023

Implications of JDA on or after 01.04.2019 for Landowner on sale of Owner sarea Landowner is liable to GST on sale of under-construction apartments / units at 5% or 1% or 12% Landowner is required to register under GST Developer will charge GST @ 5% or 1% or 12% on apartments allotted to landowner Landowner is entitled to input tax credit of GST levied by developer on construction of owner s flat subject to cap of output tax payable on Residential apartments sold under construction Notification No. 03/2021-Central Tax (Rate) dated 02.06.2021 allows developer to pay tax and raise invoice on landowner on the dates before the completion of project. This enables landowner to match the ITC with its output tax on sale of his flats 20th August 2023 CA Naresh Sheth 9

Implications of JDA (Revenue sharing) GST on transfer of development rights: Landowner transfers development rights to Developer Landowner receives consideration in form of revenue share Revenue share in respect of JDA prior to 31.03.2019 is taxable in the hands of landowner @ 18% as consideration for transfer of development rights Revenue share in respect of JDA on or after 01.04.2019 is not taxable in the hands of landowner Development rights in respect of JDA on or after 01.04.2019 is taxable under RCM in the hands of Developer to the extent attributable to: Construction of commercial premises Construction of Residential flats intended for sale after completion CA Naresh Sheth 10 20th August 2023

Implications of JDA (Revenue sharing) Tax on sale of flats/units : In given case, all the flats and units are sold by developer and hence liability to discharge GST thereon will be that of Developer As there are no allotment of flats or units to the landowner, there is no GST Liability in respect of same As landowner is neither providing any construction services nor selling under-construction flats or units, he will not be liable to register for GST and discharge any liability thereon CA Naresh Sheth 11 20th August 2023

Issues Issues 20th August 2023 CA Naresh Sheth 12

Issues Whether development rights are taxable? If yes, who is liable to pay the tax thereon? Whether construction services provided in respect of owner s area can be regarded as Works contract services where landowner has retained his FSI and/or development rights resulting in following advantages: Valuation will be cost of construction + 10% and not market value of flat Corresponding ITC will be available Whether value of land can be excluded from the value of flats and liability can be discharged at 7.5% or 1.5% on value of flat? The joint development agreement executed with landowner is silent on the point that who will bear the tax on area allotted to landowner. Who will be liable to bear GST payable on flats/units allotted to landowner? CA Naresh Sheth 20th August 2023 13

Issues After insertion of Notification No. 3/2019 to 8/2019 CT (R) dated 29.03.2019, Rule 27 to 30 is still on statute book. Can developer follow Rule 27 for valuing construction services provided to landowner? In case of RREP (Residential Real Estate Project having commercial area not exceeding 15% of total project area), what will be rate of tax on commercial units when all the residential flats are affordable residential apartments? Whether developer is entitled to exemption in respect of development rights attributable to commercial units in RREP? A project is completed in January 2019. The department is insisting on reversal of ITC of entire project in the proportion of unsold area to the total area of the project. Whether this is in consonance with the law? CA Naresh Sheth 20th August 2023 14

Issues Whether the developer is liable to discharge tax under reverse charge on following payments made to Municipal Corporation: Development charges Incentive FSI premium Chief Fire Officer fees Water and Sewerage Charges Pest Control charges Tree cutting charges CA Naresh Sheth 20th August 2023 15

Issues The residential project is commenced after 01.04.2019 and developer is paying tax at the rate of 5% on flats sold under-construction. He is liable to discharge GST under reverse charge on purchases from unregistered supplier when such purchases exceed 20% of total procurement. Whether following amounts are to be considered for calculating the shortfall: Development FSI payment Rights/ Lease premium Electricity charges Diesel generator for Premiums paid to local authority Corpus, hardship compensation etc. paid to landowner and society members Salaries & Wages Water Charges Interest Loan on Payment to unregistered GTA, Lawyers ,Security agencies Whether owner of malls, warehouses, hotels, theatres etc. is entitled to take Input tax credit in respect of goods or services used for construction of said buildings or structures? CA Naresh Sheth 20th August 2023 16

Word of Caution Views expressed are the personal views of faculty based on his interpretation of law Presentation needs to be revised and revisited on future amendments in GST Law Presentation is made for educational meeting arranged with a clear understanding that neither the Faculty nor Indore branch of ICAI will be responsible for any error, omission, commission and result of any action taken by a participant or anyone on the basis of this presentation Views expressed by the faculty should not be treated as professional advice or legal opinion on the issue discussed CA Naresh Sheth 17 20th August 2023

Any Questions ? THANK YOU naresh.sheth@jtco.co.in 20th August 2023 CA Naresh Sheth 18

")

")

![Town of [Town Name] Real Estate Tax Rates and FY 2024 Budget Summary](/thumb/62211/town-of-town-name-real-estate-tax-rates-and-fy-2024-budget-summary.jpg)