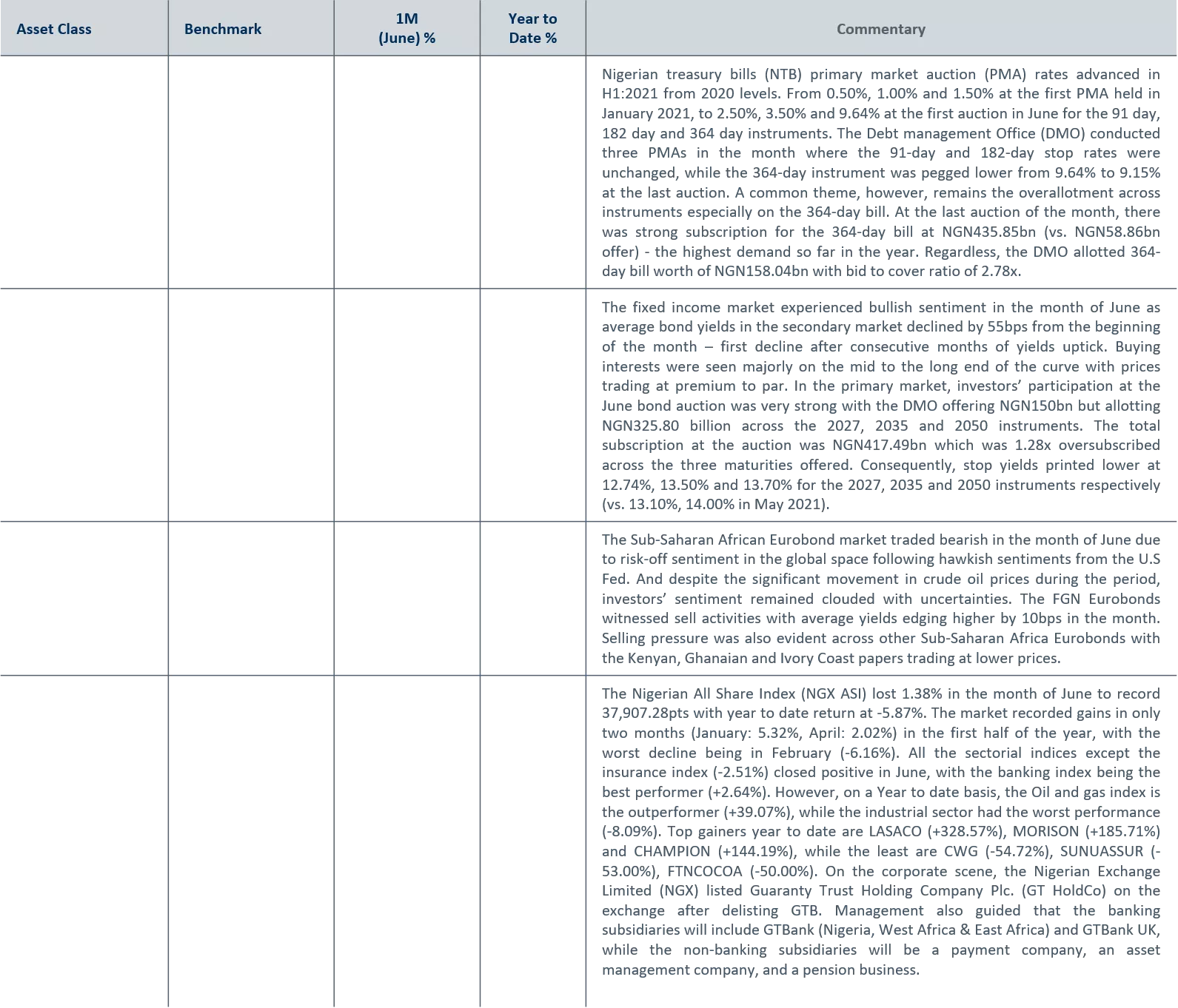

Global Economic and Financial Market Update - June 2021

•

It is the end of the first half of the year 2021 and the biggest vaccination campaign is still underway. According to Bloomberg, more than 3.05billion doses have been

administered across 180 countries by H1 – enough to fully vaccinate 19.9% of the global population. Although, vaccine distribution has been lopsided with new strains

threatening renewed outbreaks, Covid cases have generally flattened or declined where vaccination rates are highest. At the current pace of vaccination, experts

estimate that it would take another year to achieve a high level of global immunity.

•

Oil markets continue to ride on the tailwind of global reflation, rapid rollouts of Covid-19 vaccines, calibrated OPEC+ output plan and optimism around re-opening of

economies this summer. Both Brent crude and West Texas Intermediate (WTI) traded at the highest level seen in more than two and half years during the month, with

WTI breaching its USD70 per barrel resistance level. Brent crude on the other hand has advanced by 45.54% year to date, surging above USD75 per barrel, its highest

level since 2018.

•

Major global equities maintained strong momentum in H1:2021 with expectations that this will persist through the year, as strong first half year stock performance

historically bodes well for the remainder of the year. At the end of H1:2021, the Dow Jones was up 12.73%, S&P 500 (+14.41%), Nasdaq Composite (+12.93%), CAC 40

(+17.23%), FTSE 100 (+8.93%), JPX Nikkei (+7.74%), DAX (+13.14%). The small cap Russell 2000 also gained 17.00% in H1:2021 amid a strong rotation into value stocks,

as investors continue to shrug off high inflation readings on hopes of a strong economic comeback.

•

Nigeria’s headline inflation rate for the month of May 2021 declined further for the second consecutive month at 17.93% year on year (19 basis points lower than

18.12% recorded in April 2021). Food inflation dropped from 22.72% recorded in April 2021 to 22.28% in May 2021, indicating the second consecutive month of food

disinflation. Conversely, Core inflation continued to tick up, recording 13.15% in May 2021 (41bps higher than 12.74% recorded in April 2021).

All data as at 30 June 2021 unless otherwise stated

*Mean stop rate at the Monthly Nigerian treasury bill auction

** Average of Nigerian treasury bill auction from the beginning of the year

***BNGRI – Bloomberg Nigeria Local Sovereign Bond Index

2.50*

3.50*

9.40*

1.84**

2.98**

7.06**

-

-12.01

BNGRI***

3 Year Federal

Government

Bond

1.99

1.47

0.34

-0.18

-5.87

-3.78

-1.38

1.05

NSEASI

NSE30

91-day T-bill

181-day T-bill

364-day T-bill

Money Market

-

2.74

Fixed Income

Equites

3 Year Nigerian

Sovereign

Eurobond

5 Year Nigerian

Sovereign

Eurobond

Eurobond

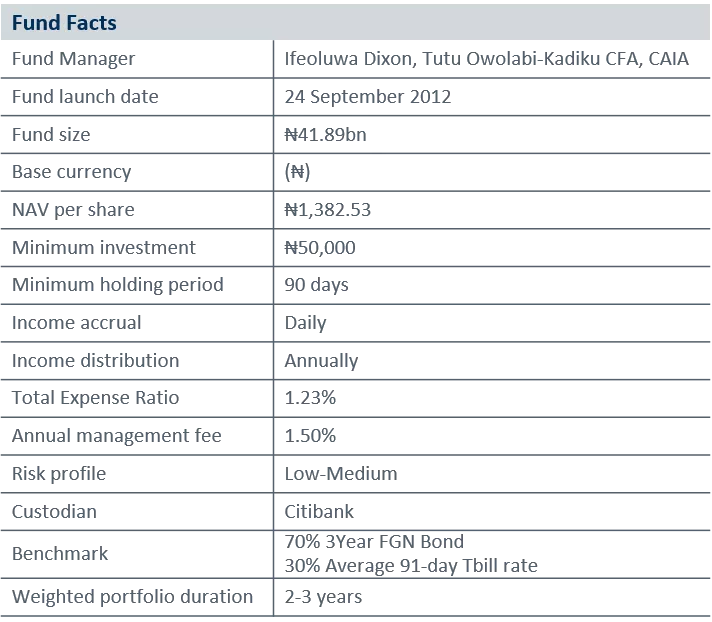

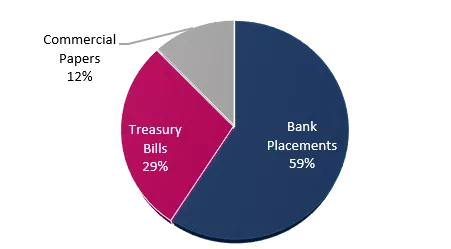

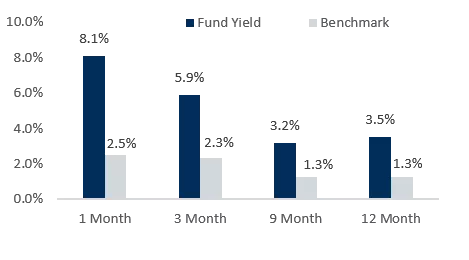

FBN Money Market Fund Overview

Investment Objective

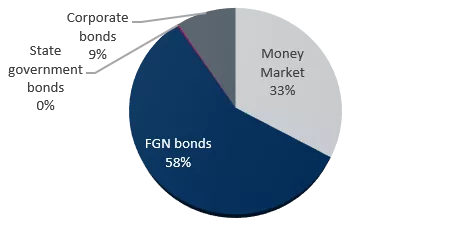

FBN Bond Fund Overview

Investment objective

The Fund seeks to preserve capital and maximise income by offering access to a diversified range of low risk money market instruments in

Nigeria. The Fund also provides liquidity and competitive returns.

The Fund is designed to provide income generation by investing in long tenured debt instruments and short-term high quality money market

securities issued in Nigeria.

Historical Prices & Performance

Historical Prices & Performance

All data as at 30 June 2021 unless otherwise stated

Asset Allocation

Asset Allocation

FBN Eurobond Fund Overview

Investment objective

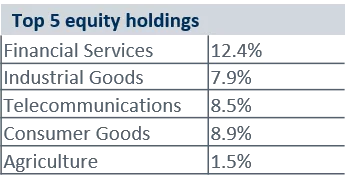

FBN Balanced Fund Overview

Investment objective

The Fund provides capital growth and downside protection to investors seeking exposure to equity. The downside is achieved through

investments in less risky assets such as money market instrument and bonds

The Fund provides an opportunity to diversify across currencies and serve as a hedge through its exposure to USD denominated assets. It

provides income generation by investing in debt instruments issued by the Nigerian government, corporates and financial institutions

Historical Prices & Performance

Historical Prices & Performance

All data as at 30 June 2021 unless otherwise stated

Asset Allocation

Asset Allocation

FBN Smart Beta Equity Fund Overview

Investment objective

The Fund seeks to provide capital growth by selecting the best twenty (20) out of the forty (40) most capitalised stocks listed on the Nigerian

Stock Exchange. The Fund is appropriate for investors who want equities with the aim of outperforming the NSE 30 index.

.

Historical Prices & Performance

FBN Halal Fund Overview

Investment objective

The Fund is designed to provide long-term income generation by investing in Shari’ah compliant instruments such as Sukuks, Ijarah (Lease),

Murabaha (Cost plus mark-up) and Mudarabah (Working Partner) contracts

.

Historical Prices & Performance

All data as at 30 June 2021 unless otherwise stated

Assets Allocation

Assets Allocation

Redemption period: 3 - 5 business days.

No additional charges are applied on redemption. However, units redeemed earlier than the minimum holding period will incur a

processing fee of 20% on the income earned on the value of such redemptions.

The Funds range from ‘Low-High’ risk profile depending on what security it is invested in. The value of securities may change significantly

depending on economic, political, inflationary and interest rate conditions.

Bid prices and yield to maturity are stated net of fees and expenses with dividends reinvested (where applicable).

The yield to maturity (YTM) is the rate of return anticipated on the portfolio if the current bonds in the portfolio were held until the end of

their lifetime. YTM is an annualised rate and takes into account the current market price, par value, coupon interest rate and time to

maturity for each bond in the portfolio. It is also assumes that all coupon payments are reinvested at the same rate as the bond’s current

yield.

Past performance is not a guide to the future. The price of investments and the income from them may fall as well as rise and investors

may not get back the full amount invested

•

With oil prices surging more than 45% in the first half of 2021, there is a likelihood for further rise in the coming period on the back of a

continuous rollout of Covid-19 vaccines and gradual easing of lockdown measures which paves way for more demand recovery. The

immediate sticking point, however, appears to be the disagreements between OPEC and its allies over how the output quotas of some

countries are calculated. The United Arab Emirates officials, for instance, believe they have been bearing a disproportionate burden of

production cuts. Hence, UAE rejected the deal to ramp up oil supply at the recently held meeting until baseline for its production cuts are

changed. Nonetheless, conclusive agreements are expected to be reached at their next meeting and we expect the group to take a cautious

approach to ease supply without depressing prices.

•

Unlike the global equities and most of the other African and regional markets, the Nigerian bourse remained downbeat for most part of half

year 2021. In terms of market valuation, price to earnings (P/E) ratio of the equities market as at half year printed below its peers at 14.17x

(vs. Ghana: 17.06x, Kenya: 14.23x, South Africa: 19.58x), which highlights investors’ bearish sentiment. Similarly, the All Share Index as at

H1:2021 (-5.43%), underperformed its African peers and overall Frontier Market (+0.09%). Going into the second half of the year, we are still

less optimistic about a turnaround except yields in the fixed income market depress significantly to trigger a rotation back to equities.

•

Yields in the fixed income market retreated in the month of June as buy side activities dominated with investors closing out their positions

for half year. We expect the prevailing demand pressure to persist in July given the significant amount of Open Market Operations (OMO)

and bond maturities, as well as coupons that would hit the system. This should spur demand for fixed income instruments in the short term..

•

The SSA Eurobond market enjoyed patronage in the first half of the year on the back of improved oil prices and optimism around recovery in

major economies. There were also new issues during the period especially from Ghana, which further spurred investors’ participation in that

space. Although, uncertainties around monetary policies especially in the US has recently dampened investors’ sentiment, we expect this to

gradually wane off even as Fed officials reassure the market that they have no plans for interest rate hikes yet. We also expect the FGN to

eventually issue the much-anticipated Eurobond expected to fund the budget deficit by H2:2021.

All data as at 30 June 2021 unless otherwise stated

It is the end of the first half of 2021, marked by significant progress in the global vaccination campaign. While economic activities are showing signs of recovery, the oil market, equities, and fixed income markets have experienced notable movements. With inflation rates fluctuating and vaccine distribution disparities, the financial landscape remains dynamic. Major global indices have shown strong performance, and various asset classes have demonstrated resilience amidst changing market conditions.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

You are allowed to download the files provided on this website for personal or commercial use, subject to the condition that they are used lawfully. All files are the property of their respective owners.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.

E N D

Presentation Transcript

INVESTING MUTUAL FUND FACTSHEET PUBLIC All data as at 30 June 2021 unless otherwise stated Executive Summary It is the end of the first half of the year 2021 and the biggest vaccination campaign is still underway. According to Bloomberg, more than 3.05billion doses have been administered across 180 countries by H1 enough to fully vaccinate 19.9% of the global population. Although, vaccine distribution has been lopsided with new strains threatening renewed outbreaks, Covid cases have generally flattened or declined where vaccination rates are highest. At the current pace of vaccination, experts estimate that it would take another year to achieve a high level of global immunity. Oil markets continue to ride on the tailwind of global reflation, rapid rollouts of Covid-19 vaccines, calibrated OPEC+ output plan and optimism around re-opening of economies this summer. Both Brent crude and West Texas Intermediate (WTI) traded at the highest level seen in more than two and half years during the month, with WTI breaching its USD70 per barrel resistance level. Brent crude on the other hand has advanced by 45.54% year to date, surging above USD75 per barrel, its highest level since 2018. Major global equities maintained strong momentum in H1:2021 with expectations that this will persist through the year, as strong first half year stock performance historically bodes well for the remainder of the year. At the end of H1:2021, the Dow Jones was up 12.73%, S&P 500 (+14.41%), Nasdaq Composite (+12.93%), CAC 40 (+17.23%), FTSE 100 (+8.93%), JPX Nikkei (+7.74%), DAX (+13.14%). The small cap Russell 2000 also gained 17.00% in H1:2021 amid a strong rotation into value stocks, as investors continue to shrug off high inflation readings on hopes of a strong economic comeback. Nigeria s headline inflation rate for the month of May 2021 declined further for the second consecutive month at 17.93% year on year (19 basis points lower than 18.12% recorded in April 2021). Food inflation dropped from 22.72% recorded in April 2021 to 22.28% in May 2021, indicating the second consecutive month of food disinflation. Conversely, Core inflation continued to tick up, recording 13.15% in May 2021 (41bps higher than 12.74% recorded in April 2021). 1M Year to Date % Asset Class Benchmark Commentary (June) % Nigerian treasury bills (NTB) primary market auction (PMA) rates advanced in H1:2021 from 2020 levels. From 0.50%, 1.00% and 1.50% at the first PMA held in January 2021, to 2.50%, 3.50% and 9.64% at the first auction in June for the 91 day, 182 day and 364 day instruments. The Debt management Office (DMO) conducted three PMAs in the month where the 91-day and 182-day stop rates were unchanged, while the 364-day instrument was pegged lower from 9.64% to 9.15% at the last auction. A common theme, however, remains the overallotment across instruments especially on the 364-day bill. At the last auction of the month, there was strong subscription for the 364-day bill at NGN435.85bn (vs. NGN58.86bn offer) - the highest demand so far in the year. Regardless, the DMO allotted 364- day bill worth of NGN158.04bn with bid to cover ratio of 2.78x. Money Market 91-day T-bill 2.50* 1.84** 3.50* 2.98** 181-day T-bill 9.40* 7.06** 364-day T-bill The fixed income market experienced bullish sentiment in the month of June as average bond yields in the secondary market declined by 55bps from the beginning of the month first decline after consecutive months of yields uptick. Buying interests were seen majorly on the mid to the long end of the curve with prices trading at premium to par. In the primary market, investors participation at the June bond auction was very strong with the DMO offering NGN150bn but allotting NGN325.80 billion across the 2027, 2035 and 2050 instruments. The total subscription at the auction was NGN417.49bn which was 1.28x oversubscribed across the three maturities offered. Consequently, stop yields printed lower at 12.74%, 13.50% and 13.70% for the 2027, 2035 and 2050 instruments respectively (vs. 13.10%, 14.00% in May 2021). BNGRI*** Fixed Income - - 3 Year Federal Government Bond 2.74 -12.01 3 Year Nigerian Sovereign Eurobond The Sub-Saharan African Eurobond market traded bearish in the month of June due to risk-off sentiment in the global space following hawkish sentiments from the U.S Fed. And despite the significant movement in crude oil prices during the period, investors sentiment remained clouded with uncertainties. The FGN Eurobonds witnessed sell activities with average yields edging higher by 10bps in the month. Selling pressure was also evident across other Sub-Saharan Africa Eurobonds with the Kenyan, Ghanaian and Ivory Coast papers trading at lower prices. 0.34 1.99 Eurobond 5 Year Nigerian Sovereign Eurobond -0.18 1.47 The Nigerian All Share Index (NGX ASI) lost 1.38% in the month of June to record 37,907.28pts with year to date return at -5.87%. The market recorded gains in only two months (January: 5.32%, April: 2.02%) in the first half of the year, with the worst decline being in February (-6.16%). All the sectorial indices except the insurance index (-2.51%) closed positive in June, with the banking index being the best performer (+2.64%). However, on a Year to date basis, the Oil and gas index is the outperformer (+39.07%), while the industrial sector had the worst performance (-8.09%). Top gainers year to date are LASACO (+328.57%), MORISON (+185.71%) and CHAMPION (+144.19%), while the least are CWG (-54.72%), SUNUASSUR (- 53.00%), FTNCOCOA (-50.00%). On the corporate scene, the Nigerian Exchange Limited (NGX) listed Guaranty Trust Holding Company Plc. (GT HoldCo) on the exchange after delisting GTB. Management also guided that the banking subsidiaries will include GTBank (Nigeria, West Africa & East Africa) and GTBank UK, while the non-banking subsidiaries will be a payment company, an asset management company, and a pension business. Equites -1.38 NSEASI -5.87 1.05 -3.78 NSE30 www.fbnquest.com/assetmanagement 16-18, Keffi Street, Off Awolowo Road, S.W. Ikoyi, Lagos, Nigeria Tel: Tel: +234 (1) 2702290-4, +234 (0) 708 065 3100 Email invest@fbnquest.com: An FBN Holdings Company *Mean stop rate at the Monthly Nigerian treasury bill auction ** Average of Nigerian treasury bill auction from the beginning of the year ***BNGRI Bloomberg Nigeria Local Sovereign Bond Index

INVESTING MUTUAL FUND FACTSHEET PUBLIC All data as at 30 June 2021 unless otherwise stated FBN Money Market Fund Overview Investment Objective The Fund seeks to preserve capital and maximise income by offering access to a diversified range of low risk money market instruments in Nigeria. The Fund also provides liquidity and competitive returns. Fund Facts Asset Allocation Fund Manager Ifeoluwa Dixon, Tutu Owolabi-Kadiku CFA, CAIA Commercial Papers 12% Fund launch date 24 September 2012 Fund size 131.74bn Base currency ( ) Bank Treasury Bills 29% NAV per share 100 Placements 59% Minimum investment 5,000 Minimum holding period 30 days Income accrual Daily Income distribution Quarterly Historical Prices & Performance Annual management fee 1.25% Total Expense Ratio 1.36% 10.0% Fund Yield Benchmark 8.1% Risk profile Low 8.0% Custodian Citibank 5.9% 6.0% Average 91-day Treasury Bill (NTB) primary auction stop rates. Benchmark 3.5% 3.2% 4.0% 2.3% 2.5% 1.3% 2.0% 1.3% 0.0% FBN Bond Fund Overview 1 Month 3 Month 9 Month 12 Month Investment objective The Fund is designed to provide income generation by investing in long tenured debt instruments and short-term high quality money market securities issued in Nigeria. Asset Allocation Fund Facts Corporate bonds 9% Fund Manager Ifeoluwa Dixon, Tutu Owolabi-Kadiku CFA, CAIA State Money Market 33% Fund launch date 24 September 2012 government bonds 0% Fund size 41.89bn Base currency ( ) NAV per share 1,382.53 FGN bonds 58% Minimum investment 50,000 Minimum holding period 90 days Income accrual Daily Income distribution Annually Historical Prices & Performance 70.0% Total Return Benchmark Total Expense Ratio 1.23% 62.6% 60.0% Annual management fee 1.50% Risk profile Low-Medium 50.0% 40.3% Custodian Citibank 70% 3Year FGN Bond 30% Average 91-day Tbill rate 2-3 years 40.0% 24.8% Benchmark 30.0% 20.6% 20.0% 12.9% Weighted portfolio duration 12.0% 10.0% www.fbnquest.com/assetmanagement -1.2% -4.1% 0.0% 16-18, Keffi Street, Off Awolowo Road, S.W. Ikoyi, Lagos, Nigeria Tel: Tel: +234 (1) 2702290-4, +234 (0) 708 065 3100 Email invest@fbnquest.com: An FBN Holdings Company Year to Date 2021 Full Year 2020 Full Year 2019 Inception to Date -10.0%

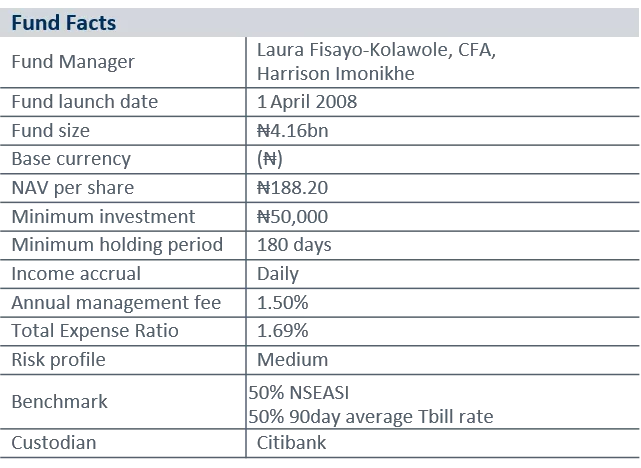

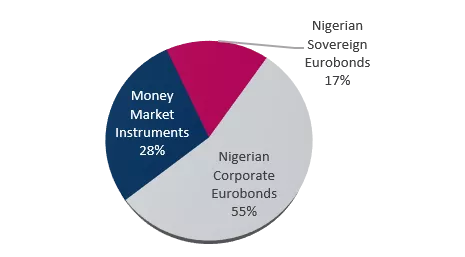

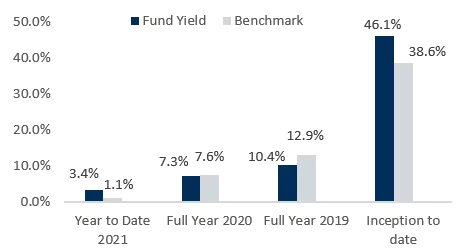

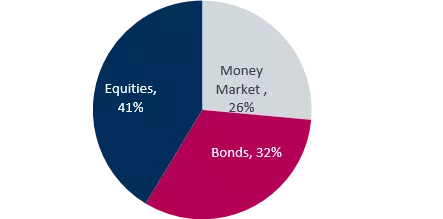

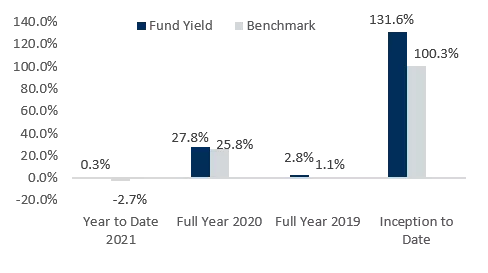

INVESTING MUTUAL FUND FACTSHEET PUBLIC All data as at 30 June 2021 unless otherwise stated FBN Eurobond Fund Overview Investment objective The Fund provides an opportunity to diversify across currencies and serve as a hedge through its exposure to USD denominated assets. It provides income generation by investing in debt instruments issued by the Nigerian government, corporates and financial institutions Fund Facts Asset Allocation Nigerian Sovereign Eurobonds 17% Ifeoluwa Dixon, Tutu Owolabi-Kadiku CFA, CAIA, Adeyemi Roberts CFA Fund Manager Fund launch date 4 January 2016 Money Market Instruments 28% Fund size $15.61mn Base currency US Dollars ($) Nigerian Corporate Eurobonds 55% Unit classes R unit class: Retail NAV per share $125.82 Minimum investment $1,000 Minimum holding period 180 days Historical Prices & Performance 50.0% Risk profile Medium Fund Yield Benchmark 46.1% Income distribution Annually 70% 3 Year FGN Bond 30% Average 1yr US Tbill rate 38.6% 40.0% Benchmark 30.0% Total Expense Ratio 1.68% 20.0% Weighted portfolio duration 1-2 years 12.9% 7.6% 10.4% 7.3% 10.0% 3.4% 1.1% 0.0% Year to Date 2021 Full Year 2020 Full Year 2019 Inception to date FBN Balanced Fund Overview Investment objective The Fund provides capital growth and downside protection to investors seeking exposure to equity. The downside is achieved through investments in less risky assets such as money market instrument and bonds Fund Facts Asset Allocation Laura Fisayo-Kolawole, CFA, Harrison Imonikhe 1April 2008 4.16bn ( ) 188.20 50,000 180 days Daily 1.50% 1.69% Medium Fund Manager Fund launch date Fund size Base currency NAV per share Minimum investment Minimum holding period Income accrual Annual management fee Total Expense Ratio Risk profile Money Market , 26% Equities, 41% Bonds, 32% Historical Prices & Performance 50% NSEASI 50% 90day average Tbill rate Citibank Benchmark 131.6% 140.0% Fund Yield Benchmark Custodian 120.0% 100.3% Top 5 equity holdings Financial Services Industrial Goods Telecommunications Consumer Goods Agriculture 100.0% 12.4% 7.9% 8.5% 8.9% 1.5% 80.0% 60.0% 40.0% 27.8% 25.8% 20.0% 2.8% 0.3% 1.1% 0.0% www.fbnquest.com/assetmanagement -2.7% -20.0% 16-18, Keffi Street, Off Awolowo Road, S.W. Ikoyi, Lagos, Nigeria Tel: Tel: +234 (1) 2702290-4, +234 (0) 708 065 3100 Email invest@fbnquest.com: An FBN Holdings Company Year to Date 2021 Full Year 2020 Full Year 2019 Inception to Date

INVESTING MUTUAL FUND FACTSHEET PUBLIC All data as at 30 June 2021 unless otherwise stated FBN Smart Beta Equity Fund Overview Investment objective The Fund seeks to provide capital growth by selecting the best twenty (20) out of the forty (40) most capitalised stocks listed on the Nigerian Stock Exchange. The Fund is appropriate for investors who want equities with the aim of outperforming the NSE 30 index. . Fund Facts Assets Allocation Laura Fisayo-Kolawole, CFA, Oyelekan Olorunkosebi CFA Fund Manager Equity 77% Fund launch date Fund size Base currency NAV per share Total Expense Ratio Minimum investment Annual management fee Risk profile Benchmark Custodian 4 January 2016 321.97mn ( ) 157.38 1.63% 50,000 1.50% High NSE 30 Standard Chartered Bank Money Market 23% Historical Prices & Performance Fund Yield Benchmark 80.0% 68.9% 70.0% Top 5 equity holdings 60.0% 50.0% Financial Services 32.1% 39.3% 40.0% Consumer Goods 16.6% 30.0% 20.5% Agriculture 13.0% 16.2% 20.0% Telecommunications 8.4% 4.1% 10.0% -5.7% Industrials 4.1% 0.0% -18.9% -2.8% Year to Date 2021 Full Year 2020 Full Year 2019 Inception to Date -10.0% -20.0% FBN Halal Fund Overview -30.0% Investment objective The Fund is designed to provide long-term income generation by investing in Shari ah compliant instruments such as Sukuks, Ijarah (Lease), Murabaha (Cost plus mark-up) and Mudarabah (Working Partner) contracts. Assets Allocation Fund Facts Ifeoluwa Dixon, Tutu Owolabi-Kadiku CFA, CAIA, Adeyemi Roberts CFA 4 May 2020 Fund Manager Shari ah- compliant Fixed Term Investment 30% Fund launch date Fund size 5.07bn Base currency ( ) Sukuk Bonds 70% NAV per share 110.83 Minimum investment 5,000 Minimum holding period 90 days Income accrual Daily Income distribution Semi-annually (April and October) Historical Prices & Performance Total Expense Ratio 1.70% Fund Yield Benchmark 15.0% Risk profile Low-Medium 12.9% Custodian Standard Chartered 10.0% 8.2% Benchmark FGN 3 Year Benchmark Bond 5.0% 1.2% 0.0% Year to Date 2021 Inception to date www.fbnquest.com/assetmanagement -5.0% 16-18, Keffi Street, Off Awolowo Road, S.W. Ikoyi, Lagos, Nigeria Tel: Tel: +234 (1) 2702290-4, +234 (0) 708 065 3100 Email invest@fbnquest.com: An FBN Holdings Company -6.0% -10.0%

INVESTING MUTUAL FUND FACTSHEET PUBLIC All data as at 30 June 2021 unless otherwise stated Outlook With oil prices surging more than 45% in the first half of 2021, there is a likelihood for further rise in the coming period on the back of a continuous rollout of Covid-19 vaccines and gradual easing of lockdown measures which paves way for more demand recovery. The immediate sticking point, however, appears to be the disagreements between OPEC and its allies over how the output quotas of some countries are calculated. The United Arab Emirates officials, for instance, believe they have been bearing a disproportionate burden of production cuts. Hence, UAE rejected the deal to ramp up oil supply at the recently held meeting until baseline for its production cuts are changed. Nonetheless, conclusive agreements are expected to be reached at their next meeting and we expect the group to take a cautious approach to ease supply without depressing prices. Unlike the global equities and most of the other African and regional markets, the Nigerian bourse remained downbeat for most part of half year 2021. In terms of market valuation, price to earnings (P/E) ratio of the equities market as at half year printed below its peers at 14.17x (vs. Ghana: 17.06x, Kenya: 14.23x, South Africa: 19.58x), which highlights investors bearish sentiment. Similarly, the All Share Index as at H1:2021 (-5.43%), underperformed its African peers and overall Frontier Market (+0.09%). Going into the second half of the year, we are still less optimistic about a turnaround except yields in the fixed income market depress significantly to trigger a rotation back to equities. Yields in the fixed income market retreated in the month of June as buy side activities dominated with investors closing out their positions for half year. We expect the prevailing demand pressure to persist in July given the significant amount of Open Market Operations (OMO) and bond maturities, as well as coupons that would hit the system. This should spur demand for fixed income instruments in the short term.. The SSA Eurobond market enjoyed patronage in the first half of the year on the back of improved oil prices and optimism around recovery in major economies. There were also new issues during the period especially from Ghana, which further spurred investors participation in that space. Although, uncertainties around monetary policies especially in the US has recently dampened investors sentiment, we expect this to gradually wane off even as Fed officials reassure the market that they have no plans for interest rate hikes yet. We also expect the FGN to eventually issue the much-anticipated Eurobond expected to fund the budget deficit by H2:2021. Terms and Conditions Redemption period: 3 - 5 business days. No additional charges are applied on redemption. However, units redeemed earlier than the minimum holding period will incur a processing fee of 20% on the income earned on the value of such redemptions. The Funds range from Low-High risk profile depending on what security it is invested in. The value of securities may change significantly depending on economic, political, inflationary and interest rate conditions. Bid prices and yield to maturity are stated net of fees and expenses with dividends reinvested (where applicable). The yield to maturity (YTM) is the rate of return anticipated on the portfolio if the current bonds in the portfolio were held until the end of their lifetime. YTM is an annualised rate and takes into account the current market price, par value, coupon interest rate and time to maturity for each bond in the portfolio. It is also assumes that all coupon payments are reinvested at the same rate as the bond s current yield. Past performance is not a guide to the future. The price of investments and the income from them may fall as well as rise and investors may not get back the full amount invested www.fbnquest.com/assetmanagement 16-18, Keffi Street, Off Awolowo Road, S.W. Ikoyi, Lagos, Nigeria Tel: Tel: +234 (1) 2702290-4, +234 (0) 708 065 3100 Email invest@fbnquest.com: An FBN Holdings Company