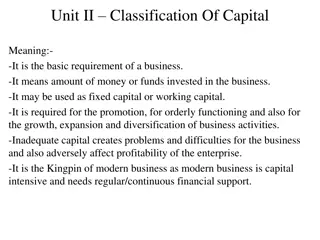

Piecemeal Distribution in Partnership Accounts: Surplus Capital Method Example

In partnership dissolution, assets are realized gradually, leading to uncertainty in profit or loss distribution. Piecemeal distribution methods like Surplus Capital Method help allocate cash among partners based on surplus capital. In this situation, a case study illustrates how partners A, B, and C's assets were realized over time, showcasing a step-by-step approach to distribution under the Surplus Capital Method.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. Download presentation by click this link. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

E N D

Presentation Transcript

Partnership Accounts-Piecemeal Distribution Ms. Meenakshi Assistant Professor Commerce Department Kanya Mahavidyalaya Kharkhoda

Introduction of Piecemeal Distribution The assumption that all assets are realized immediately on the date of dissolution and all the liabilities are paid on that date is unrealistic. In actual practice, assets are realized gradually and cash is distributed among different parties as and when realized. There may be a gap of few months between the realization of two assets. Hence, final result (profit or loss on realization) of business is not known till all assets are realized. In such situation, piecemeal adopted. As per this system first, all creditors/outside liabilities are paid, then loans given by the partners are returned and then if cash is realized further it would be distributed immediately among partners without waiting for the completion of all realizations. distribution system is

Continues The difficulty is how to distribute the available cash among the ascertainment of profit or loss on realization. And the same can not be ascertained until all assets are realized. In such situation, any of the following methods may be adopted for payment to partners. partners without Proportionate Capital Method/ Surplus Capital method Maximum Loss Method

Proportionate Capital Method I In this method, the capitals of partners are adjusted in their profit sharing ratio. (This is done by taking one partner s capital as base.) II The partner whose capital is in excess of others (after adjusting in profit sharing ratio) is refunded his excess capital. III After refunding the excess capitals, the capitals will be automatically left in profit sharing ratio. After this , the cash realized from assets will be distributed among all the partners in their profit sharing ratio. IV The unpaid balance of the capital accounts will represent loss on realization and this loss will be exactly in profit sharing ratio.

Illustration A, B and C were in partnership sharing profits and losses of 3:2:1. The following is their Balance Sheet as at 31st Dec.,2014 on which date they dissolved the partnership: Liabilities Amount (Rs.) Assets Amount (Rs.) Sundry Creditors A s Loan General Reserve Capitals : A 94,000 B 20,000 C 23,000 25,000 8,000 12,000 Cash Debtors Stock Fixed Assets 3,000 34,800 52,500 91,700 1,37,000 1,82,000 1,82,000 It was agreed to repay the amounts due to the partners as and when the assets are realized.

Continues Assets realized as follows: Month Debtors Stock Fixed Assets Expenses February March May July 4,000 12,000 8,000 6,000 5,000 10,000 17,000 9,000 10,000 32,000 20,000 22,000 800 1,200 1,500 1,000 Prepare a statement showing how the distribution should be made according to Surplus Capital Method..

Solution Cash Available each Month Month Debtors + Stock + Fixed Assets Expenses = Cash Available Feb March May July 4,000 12,000 8,000 6,000 5,000 10,000 17,000 9,000 10,000 32,000 20,000 22,000 800 1,200 1,500 1,000 18,200 52,800 43,500 36,000

Calculation of Surplus or excess capital A B C Partners Profit Sharing ratio Capitals as per Balance Sheet (Rs.) Add : General Reserve (12,000) in 3:2:1 Actual Capitals Capitals in profit Sharing ratio i.e.3:2:1 (taking B s capital as base ) B s capital 24,000 Total capital = 24,000 *6/2=72,000 72,000 divided in 3:2:1 Surplus Capitals Capitals of A and C in profit sharing ratio i.e. 3:1 (taking C s capital as base) 13,000 *4/1=52,000 Rs. 52,000 divided in 3:1 Ultimate surplus capital to be refunded first 3 94,000 6,000 1 ,00,000 2 20,000 4,000 24,000 1 23,000 2,000 25,000 36,000 64,000 24,000 --------- 12,000 13,000 39,000 25,000 13,000 ---------- -----------

Statement showing piecemeal distribution of Cash Date/ Month Particulars Cash Creditors A s Loan A B C Jan Balances as per balance sheet Add: Gen. Reserve (12,000 in 3:2:1) Balances Cash in hand paid to creditors Balances Gross Realization Paid to creditors Balances Gross Realization Paid to creditors and A s Loan Balances Paid to A, his surplus capital Balances 3,000 25,000 8,000 94,000 20,000 23,000 --- --- --- 6,000 4,000 2,000 3,000 25,000 8,000 1,00,000 24,000 25,000 Jan -3,000 --- 18,200 - 18,200 --- 52,800 -11,800 3,000 22,000 --- -18,200 3,800 ---- - 3,800 --- 8,000 --- --- 8,000 ---- -8,000 ---- 1,00,000 --- --- 1,00,000 ---- ---- --- 24,000 --- --- 24,000 ----- ----- --- 25,000 --- --- 25,000 ---- ---- Feb Feb March March 41,000 -25,000 ---- ---- ---- ---- 1,00,000 - 25,000 24,000 ----- 25,000 ---- March 16,000 ---- ---- 75,000 24,000 25,000

continues.. Date/ Month Particulars Cash Cr A s Loan A B C March Balances paid to A & C in the ratio of 3:1 Balances Gross Realization Paid to A & C in the ratio of 3:1 to bring their proportionate to B Balances Balance distributed to all partners in their profit sharing ratio 3:2:1 16,000 75,000 24,000 25,000 -16,000 --- 43,500 -36,000 7,500 -12,000 63,000 ----- ---- 24,000 ----- - 4,000 21,000 ----- May capital -27,000 36,000 ----- 24,000 -9,000 12,000 -7,500 - 3,750 - 2500 - 1250 Balances ---- 36,000 -36,000 ----- 32,250 ----- -18,000 21,500 ----- - 12,000 10,750 ----- -6,000 Gross realization Rs.36,000, distributed in 3:2:1 Balance Left (Loss on realization) 14,250 9,500 4750

Maximum Loss Method An alternative method of piecemeal distribution amongst partner is to calculate the maximum possible loss on every realization after the outside liabilities and the partners loan has been paid off. The amount available for distribution is compared with the total amount of capital payable to the partners and maximum loss is ascertained on the assumption that in future assets will not fetch any amount. The maximum possible loss is deducted from the capital balances of the partners in their profit and loss sharing ratio. The balance left in the capital account after deducting the maximum possible loss will be the amount payable to the partner.

Which method should be adopted If it is not specifically mentioned in the question as to which method is to be adopted, then any of the two methods may be adopted. But, if it is clearly stated in the question to apply the rule of Garner vs. Murray or distribution of cash is to be made assuming that no further realization of assets will be made, maximum loss method will be used.

Illustration Taking the same problem which has been solved by applying surplus capital method ,show the distribution of cash under Maximum loss method. Solution: Cash available each month Month Debtors + Stock + Fixed Assets - Expenses = cash available Feb March May July 4,000 12,000 8,000 6,000 5,000 10,000 17,000 9,000 10,000 32,000 20,000 22,000 800 1,200 1,500 1,000 18,200 52,800 43,500 36,000

Statement showing piecemeal distribution of Cash Date/ Month Particulars Cash Creditors A s Loan A B C Jan Balances balance sheet Add: Gen. Reserve (12,000 in 3:2:1) Balances Cash in hand paid to creditors Balances Gross Realization Paid to creditors as per 3,000 25,000 8,000 94,000 20,000 23,000 --- --- --- 6,000 4,000 2,000 3,000 25,000 8,000 1,00,000 24,000 25,000 Jan -3,000 --- 18,200 - 18,200 --- 52,800 -11,800 3,000 22,000 --- -18,200 3,800 ---- - 3,800 --- 8,000 --- --- 8,000 ---- -8,000 ---- 1,00,000 --- --- 1,00,000 ---- ---- --- 24,000 --- ----- 24,000 ----- ------ 24,000 --- 25,000 --- --- 25,000 ---- ---- Feb Feb Balances March March Gross Realization Paid to creditors and A s Loan Balances 41,000 ---- ---- 1,00,000 25,000 March Maximum loss (1,08,000 in 3:2:1) {1,00,000+24,000+25 ,000 = 1,49,000} [1,49,000-41,000 =1,08,000] -54,000 46,000 -36,000 -18,000 -12,000 7,000

continues.. Month Particulars Cash Cr. A s Loan A B C March Balances +46,000 -12,000 +7,000 B s deficiency borne by A and C in their capital ratio i.e.1,00,000: 25,000 or 4:1 Thus, payment of 41,000 to A & C - 9,600 36,400 +12,000 ---- -2,400 4,600 41,000 Balance due ------- 43,500 63,600 --- --- 24,000 ------ 20,400 ------ Gross Realization Maximum loss 64,500 in ratio 3:2:1 (63,600+24,000+ 20,400 = 1,08,000) {1,08,000-43,500 =64,500} Thus, Payment of 43, 500 to A ,B & C May -32,250 31,350 -21,500 2,500 -10,750 9,650 43,500 Balance Due ---- 36,000 32,250 ------ 21,500 ------ 10,750 ----- Gross realization Final loss 28,500 in 3:2:1 (32,250+21,500+10,750= 64,500) {64,500-36,000=28,500} July -14,250 -9,500 -4,750