Importance of Ethics in Internal Audit Practices

Ethics play a crucial role in internal audit, ensuring good governance, trust, and accountability. This article explores the definition of ethics, ethical culture, the IIAs Code of Ethics for Internal Auditors, and the significance of upholding ethical standards in conducting internal audit work.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. Download presentation by click this link. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

E N D

Presentation Transcript

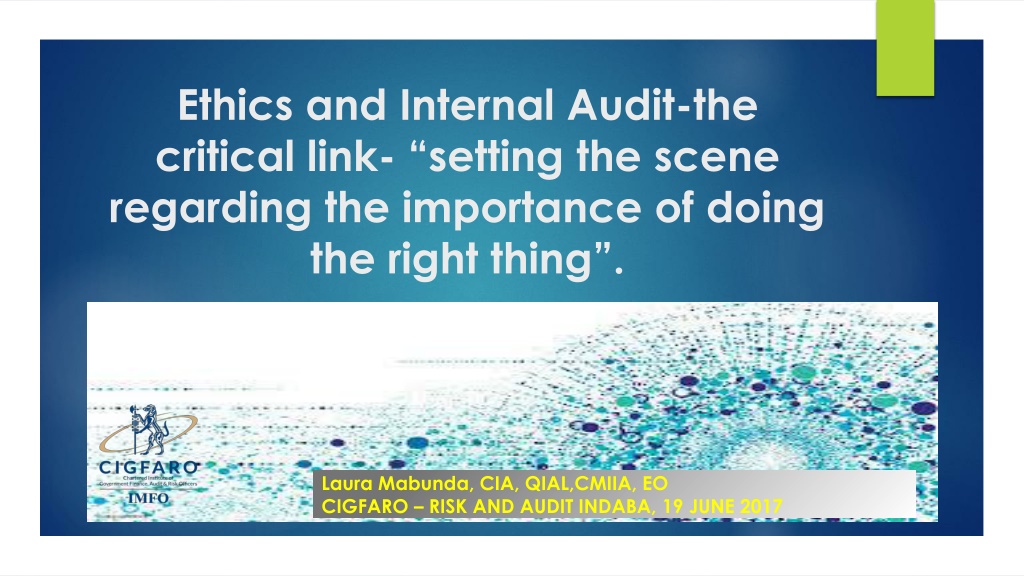

Ethics and Internal Audit-the critical link- setting the scene regarding the importance of doing the right thing . Laura Mabunda, CIA, QIAL,CMIIA, EO CIGFARO RISK AND AUDIT INDABA, 19 JUNE 2017

What is Ethics The definition of ethics is that ethics concerns itself with what is good or right in human interaction it resolves around three different concepts: good, self and other. Ethical behavior results when one does not merely consider what is good for oneself but also what is good for others Ethics is all about behavior, choices and doing what is right.

Ethical culture A strong is the foundation of good governance. An ethical culture is created through a robust ethics program that sets expectations for acceptable behaviors in conducting business within the organization and with external parties. It includes effective board oversight, strong tone-at-the-top, senior management involvement, organization wide commitment, a customized code of conduct,

Ethical culture timely follow-up and investigation of reported incidents, consistent disciplinary action for offenders, ethics training, communications, ongoing monitoring systems, and an anonymous incident reporting system.

IIAs Code of Ethics for Internal Auditors Practice What We Preach The IIA s Code of Ethics underlies the conduct of internal audit work and compliance with the Code is mandatory. Compliance with the Code of Ethics is mandatory because of the trust placed by internal and external stakeholders in the internal audit profession and the activity. Internal audit must be viewed as a role model and an advocate of strong ethics

IIAs Code of Ethics for Internal Auditors Practice What We Preach The IIA s Code of Ethics is applicable to the internal audit activity and its staff. Internal auditors must apply the principles to all aspects of their work and their relationships with the audit committee, management, employees, and other stakeholders. Noncompliance can result in disciplinary actions, including expulsion from The IIA and withdrawal of the Certified Internal Auditor (CIA) designation.

Code of Ethics The Code of Ethics of the Institute exceeds the definition of internal audit that includes two basic components: 1. Principles that are relevant to the profession and practice of internal audit; 2. Rules of Conduct that describe behavior norms expected of internal auditors

1. Integrity The integrity of internal auditors establishes trust and thus provides the basis for reliance on their judgment. Rule of Conduct 1.1. Shall perform their work with honesty, diligence, and responsibility. 1.2. Shall observe the law and make disclosures expected by the law and the profession. 1.3. Shall not knowingly be a party to any illegal activity, or engage in acts that are discreditable to the profession of internal auditing or to the organization. 1.4. Shall respect and contribute to the legitimate and ethical objectives of the organization.

2. Objectivity Internal auditors exhibit the highest level of professional objectivity in gathering, evaluating, and communicating information about the activity or process being examined. Internal auditors make a balanced assessment of all the relevant circumstances and are not unduly influenced by their own interests or by others in forming judgments

2. Objectivity continues Rules of Conduct 2.1. Shall not participate in any activity or relationship that may impair or be presumed to impair their unbiased assessment. This participation includes those activities or relationships that may be in conflict with the interests of the organization. 2.2. Shall not accept anything that may impair or be presumed to impair their professional judgment. 2.3. Shall disclose all material facts known to them that, if not disclosed, may distort the reporting of activities under review.

3. Confidentiality Internal auditors respect the value and ownership of information they receive and do not disclose information without appropriate authority unless there is a legal or professional obligation to do so. Rules of Conduct 3.1. Shall be prudent in the use and protection of information acquired in the course of their duties. 3.2. Shall not use information for any personal gain or in any manner that would be contrary to the law or detrimental to the legitimate and ethical objectives of the organization.

4. Competency Internal auditors apply the knowledge, skills, and experience needed in the performance of internal audit services. Rule of conduct 4.1. Shall engage only in those services for which they have the necessary knowledge, skills, and experience. 4.2. Shall perform internal audit services in accordance with the International Standards forthe Professional Practice of Internal Auditing. 4.3. Shall continually improve their proficiency and the effectiveness and quality of their services.

Ethical Dilemma Chief Audit Executive and Internal Audit Staff have a responsibility to behave professionally and ethically at all times and will have a particularly important role to play in creating, promoting and maintaining an ethical culture within the practice and, possibly, among the clients of the practice. Internal Auditors have an Impact on the organizational ethics tone and may be subject to scrutiny by the staff of the organization. A high level of professional competence from their Internal Auditors is expected, and to be a trusted advisor requires the Internal Auditor s integrity to be unquestionable.

Ethics intelligence Internal Auditors are challenged to recognize and evaluate ethical and unethical situations often encountered in practice and it is important to be alert to situations that may threaten these fundamental principles. What on earth is ethics intelligence? I would define it as the ability to discern when there are ethical implications in an issue and being able to respond appropriately from an ethical perspective by Dr. C von Eck

Ethics intelligence Speaks to the individuals ability to recognize ethical implications in decisions and situations and respond appropriately It also speaks to the ability to recognize ethical dilemma and being able to find the best means to deal with such a dilemma i.e finding a solution that would have the least adverse impact.

Ethics intelligence The ability to identify ethical and unethical behavior is essential in all professions, internal auditing is no exception!!! IA has an obligations to the organizations they serve, their professions and themselves to exercise sound ethical judgement.

Ethical Treats to Internal Auditor Independence

Ethical Treats to Internal Auditor Independence Familiarity: the threat that, due to a long or close relationship with someone, you will be too sympathetic to that person s interests, or too accepting of their work Intimidation: the threat that you will be deterred from acting objectively because of actual or perceived pressures, including attempts to exercise undue influence over you.

Ethical Treats to Internal Auditor Independence Self-interest: the threat that a financial or other interest will inappropriately influence your judgement or behaviour Self-review: the threat that you will not properly evaluate the results of a previous judgement made or service performed by you (or someone else within your practice) when forming a judgement as part of providing a current service Advocacy: the threat that you will promote a position (usually your client s) to the point that your objectivity is compromised

Internal Auditors Continue to Face Ethical Dilemmas

The IIAs 2015 Global Internal Audit Common Body of Knowledge Survey. Ethics and Pressure: Balancing the Internal Audit Profession states that 23 percent of internal auditors worldwide have been asked at least once to change or suppress an important audit finding, and 11 percent preferred not to answer the question, The survey of more than 14,500 practitioners in 166 countries also indicates that 20 percent of staff auditors have been pressured occasionally or frequently to alter audit findings, while 14 percent declined to answer, which the report suggests could be because of intimidation.

What happens when internal auditors dont want to go along with unethical requests? According to the report, 33 percent said they d be excluded from meetings, 18 percent would lose opportunities, 4 percent saw budget cuts, 1 percent were demoted, another 1 percent had their pay cut, and 13 percent said other.

What happens when internal auditors dont want to go along with unethical requests? While each situation is unique, the report states, some of the more typical other responses included: Reduced communication from executive management. Discrimination via gossip and second-guessing. Job elimination. Audit department outsourcing.

What happens when internal auditors dont want to go along with unethical requests? Hostile working conditions and stress, resulting in health issues. Pay raises for internal audit staff frozen, while others received pay increases. Denied requests for additional internal audit department staff. Internal auditors can often find themselves side-lined or hindered in their quest to ascertain whether the governance around such decisions is adequate. Being asked to reschedule audits, delaying meetings, documents forgotten to be shared or worse still being told that certain areas will not be looked at

Are you facing ethical dilemma? Seek advice from your professional body or obtain independent legal advice. Consider whether your actions in response to the situation and the advice obtained are sufficiently well documented, either by way of minutes or your own records.

Auditing ethics definition Ethics audit is a systematic evaluation of an organization s ethics program and performance to determine whether it is effective. The audit provides an opportunity to measure conformity to the organization s desired ethical standards.

Auditing ethics CBOK 2015 Global Practitioner Survey Institute of Internal Auditors' (IIA) Common Body of Knowledge (CBOK) 2015 Global Practitioner Survey, Mapping Your Career, Competencies Necessary for Internal Audit Excellence. Internal auditors throughout the world rate themselves highly in professional ethics but far lower in technical skills

Auditing ethics - CBOK 2015 Global Practitioner Survey But despite auditors' overall high ranking in professional ethics, the survey revealed a need for improvement in certain areas. For example, the survey report notes that 73 percent and 72 percent of respondents rate themselves as advanced or expert in ethics' competencies of maintaining confidentiality and objectivity. But in incorporating ethics and fraud into audit engagements, professionals confident in performing advanced and complex tasks dropped to 64 percent and 60 percent, respectively. And slightly more than 10 percent indicated they need supervision for routine tasks in those two skills.

Auditing ethics legal requirement The International Standards for the Professional Practice of Internal Auditing (The Standards) issued by the Institute of Internal Auditor (IIA) state that (Standard 2110.A1): The internal audit activity must evaluate the design, implementation, and effectiveness of the organization s ethics- related objectives, programs, and activities.

Auditing ethics the role of Internal Auditors Assessing the state of the organization s ethical climate and the effectiveness of its strategies, tactics, communications, and other processes in achieving the desired level of legal and ethical compliance Evaluating the design, implementation, and effectiveness of the organization s ethics-related objectives, programs, and activities. Providing assurance that ethics programs achieve stated objectives, key risks are effectively managed, and controls continue to operate effectively

Auditing ethics the role of Internal Auditors Providing consulting services to help the organization establish a robust ethics program and improve its effectiveness to the desired performance level. Serving as a role model and ethics advocate. Internal audit has a high level of trust, integrity, and competence to advocate appropriate conduct to comply with the organization s legal, ethical, and societal responsibilities and promote appropriate ethics and values.

Auditing ethics the role of Internal Auditors Serving as a subject matter expert on ethics-related issues and as a member of the organization s ethics council (or equivalent). Acting as a catalyst for change, promoting and recommending enhancements for the organization s governance structure and practices.

Auditing ethics understanding organizational culture Reviewing the organization s mission, vision, strategic plan, code of conduct, allegation reporting system, related regulatory and privacy requirements, etc. Confirming internal audit s understanding with management and employees. Reflecting on insights from past business issues and audit findings. Reviewing applicable legislation and guidelines.

Auditing ethics Key Considerations Realistic audit objectives need to be set, which are likely to include such things as whether: There is compliance with laws, regulations and policies. The organization has a documented ethics program and adequate means of measuring its effectiveness. There has been effective implementation of the ethics program.

Auditing ethics Key Considerations Breaches of the ethics program have been properly investigated and adequate sanctions imposed on offenders. Lapses in ethical behavior have an impact on the efficiency, effectiveness and economy of business operations and, if so, what is the impact on the organization. Assets are properly safeguarded from unethical conduct. Opportunity for fraud and corruption is minimized.

Auditing ethics - Key considerations The audit committee should identify specific ethics-related issues on which to focus. In some settings, the committee may decide to conduct a comprehensive ethics audit. In other organizations, the committee may focus on specific ethical issues that are especially important in those settings. An audit of ethics needs to be risk-based and based on a risk assessment. The internal auditor must establish the key risks to the organization s ethics program which will help to focus the audit objectives.

Auditing ethics - Scope of the Audit An audit of ethics should at least cover the following: Tone at the top commitment of the board and top management to ethics. Ethical principles how well these are adhered to by all levels of the organization, including stakeholders and suppliers. Risk management recognition of the need for risk management and effective implementation of risk management throughout the organization.

Auditing ethics - Scope of the Audit Information availability of information relating to ethical conduct such as a documented ethical program, awareness activities, and breaches of ethical guidelines. Sharing active sharing of information relating to the ethical program and its results. Alignment risk management alignment with the organization s ethical culture.

Auditing ethics Reporting and monitoring Report the audit results without fear or favor to the audit committee and senior management. Monitor and follow-up to ensure recommendations are effectively implemented and meaningful change occurs in a timely way.

Auditing Ethics Benefits To improve ethical performance and to give assurance that the organizations has an effective ethics program. The auditing process can highlight trends, improve organizational learning, and facilitate communication and working relationships. Improved relationships with stakeholders who desire greater transparency.

Way forward Internal auditors should take an active role in support of the organization s ethical culture. They should be trusted within the organization and possess a high level of integrity and the skills to be effective advocates of ethical conduct. They should have the competence and capacity to appeal to the organizations s leaders, managers, and other employees to comply with the legal, ethical, and societal responsibilities of the organization

Way forward The IIA s Code of Ethics helps ensure that internal auditors practice what they preach. The CAE should ensure that all audit work is performed in full compliance with, and meets the intent of, the Code. The CAE may assume proactive roles such as becoming a nonvoting member of an internal ethics council or conducting ethics training sessions.

Way forward The internal audit activity may also play roles that relate to both promoting and assessing ethics, such as hosting the organization s whistleblowing hotline or conducting fraud investigations. Before accepting such roles the CAE should consider how they would affect the perception of internal audit within the organization.

Maintaining dignity of the profession and internal auditors The supervising and governing institution of internal auditing profession to hold training courses, workshops and conferences on the standards of Internal auditing and professional work in general including the ethical principles and rules conduct of auditing in particular. The Role of the Audit Committees to be strengthened to support of the independence and neutrality of the internal auditors, as well as verifying the efficiency and professional level performance. The development and establishment of an incentive means that contribute in making the auditors committed to ethics of their profession

Auditing ethics conclusion Conducting an ethics audit requires a team effort as well as a clear definition of ethical behavior. Auditing ethics is not only required by the IIA s Standards but it is essential for the overall health of the organization. Even though there is no one size fits all approach to auditing ethics, the internal audit department should still take steps to audit the ethics program. Just because it is a difficult audit to do is no reason to ignore it especially when the risk of not carrying out an ethics audit can be severe.