Principles of Least Cost Combination in Economics

Least Cost

Combination

Dr. Pooja Singh

Assistant Professor,

Department of Economics,

School of Arts, Humanities And Social Sciences,

Chhatrapati Shahu Ji Maharaj University, Kanpur

Principle of Least Cost Combination

•

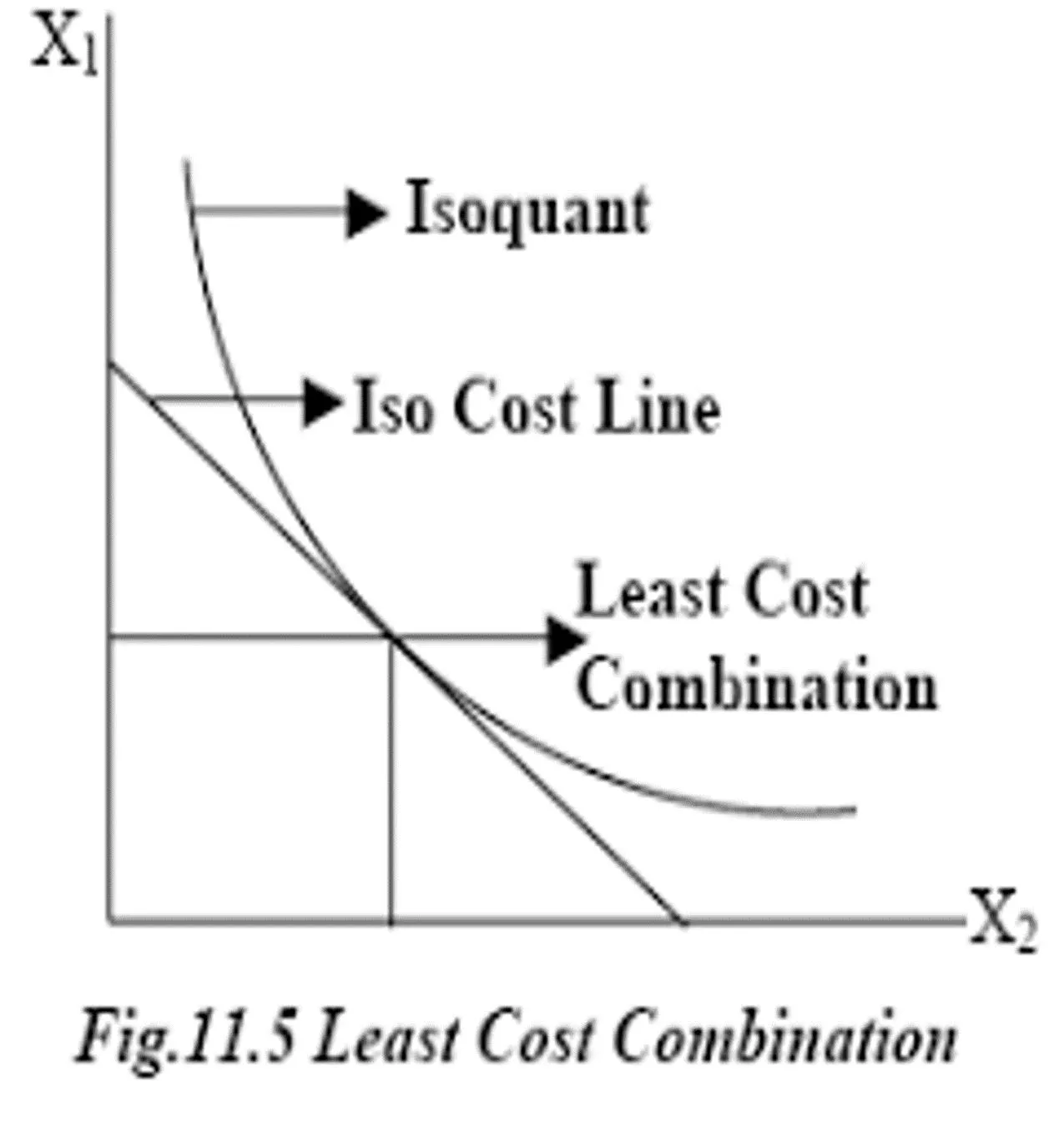

An isoquant curve is the combination of various factors of production that gives the same

level of output.On other hand , isocost line shows the combination prices that a firm incurs .

A firm requires a maximum level of output at minimum cost.

This can be achieved at the

output where the isoquant touches the isocost line which shows the least cost combination

available for particular firm.

•

Equilibrium point is where isoquant is tangent to isocost line.

Dr. Pooja Singh, Assistant Professor, Department of Economics,

School of Arts, Humanities And Social Sciences,

Chhatrapati Shahu Ji Maharaj University, Kanpur

Least Cost Combination

Assumptions:

The assumptions on which this

analysis is based are:

1.

There are two factors. Capital and labor.

2.

All units of capital and labor are

homogeneous.

3.

The prices of factors of production are

given and constant.

4.

Money outlay at any time is also given

.

Dr. Pooja Singh, Assistant Professor, Department of Economics,

School of Arts, Humanities And Social Sciences,

Chhatrapati Shahu Ji Maharaj University, Kanpur

Least Cost Combination

References

•

Dwivedi D N, Managerial Economics, Vikas Publishing House Pvt.

Ltd, 2006

•

Samuelson, Paul A; Nordhaus, William D. (2014). Economics. Boston,

Mass: Irwin McGraw-Hill

Dr. Pooja Singh, Assistant Professor, Department of Economics,

School of Arts, Humanities And Social Sciences,

Chhatrapati Shahu Ji Maharaj University, Kanpur

Least Cost Combination

In economics, the principle of least cost combination involves determining the optimal combination of factors of production (such as capital and labor) that allows a firm to achieve maximum output at minimum cost. This is achieved by identifying the point where the isoquant curve intersects the isocost line, representing the least cost combination available. Assumptions include homogeneity of factors, constant factor prices, and fixed money outlay. References like Dwivedi D.N's Managerial Economics and Samuelson & Nordhaus's Economics provide further insight into this concept.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. Download presentation by click this link. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

E N D

Presentation Transcript

Least Cost Combination Dr. Pooja Singh Assistant Professor, Department of Economics, School of Arts, Humanities And Social Sciences, Chhatrapati Shahu Ji Maharaj University, Kanpur

Least Cost Combination Principle of Least Cost Combination An isoquant curve is the combination of various factors of production that gives the same level of output.On other hand , isocost line shows the combination prices that a firm incurs . A firm requires a maximum level of output at minimum cost.This can be achieved at the output where the isoquant touches the isocost line which shows the least cost combination available for particular firm. Equilibrium point is where isoquant is tangent to isocost line. Dr. Pooja Singh, Assistant Professor, Department of Economics, School of Arts, Humanities And Social Sciences, Chhatrapati Shahu Ji Maharaj University, Kanpur

Least Cost Combination Assumptions: The assumptions on which this analysis is based are: 1.There are two factors. Capital and labor. 2.All units of capital and labor are homogeneous. 3.The prices of factors of production are given and constant. 4.Money outlay at any time is also given. Dr. Pooja Singh, Assistant Professor, Department of Economics, School of Arts, Humanities And Social Sciences, Chhatrapati Shahu Ji Maharaj University, Kanpur

Least Cost Combination References Dwivedi D N, Managerial Economics, Vikas Publishing House Pvt. Ltd, 2006 Samuelson, Paul A; Nordhaus, William D. (2014). Economics. Boston, Mass: Irwin McGraw-Hill Dr. Pooja Singh, Assistant Professor, Department of Economics, School of Arts, Humanities And Social Sciences, Chhatrapati Shahu Ji Maharaj University, Kanpur