Branch Accounting Overview and Entries

Prepared By

Dr. SHAHID IQBAL

Guest Faculty

Marwari College, Darbhanga,

Mobile No. and Whatsup No. : 7004160257

Email ID: shahidlnmu@gmail.com

1

WELCOME

WELCOME

Class: B.Com – Part-1

Class: B.Com – Part-1

Subject: Financial Accounting

Subject: Financial Accounting

TOPIC:

TOPIC:

Branch Accounts

Branch Accounts

– Part - 3

– Part - 3

2

(

B) Branch receiving goods from head office at cost price and

making both cash and credits sales :

If branch is authorised to sale goods cash as well as credit, the

following entries are also included in respect of credit sales in

addition to the above entries discussed earlier :

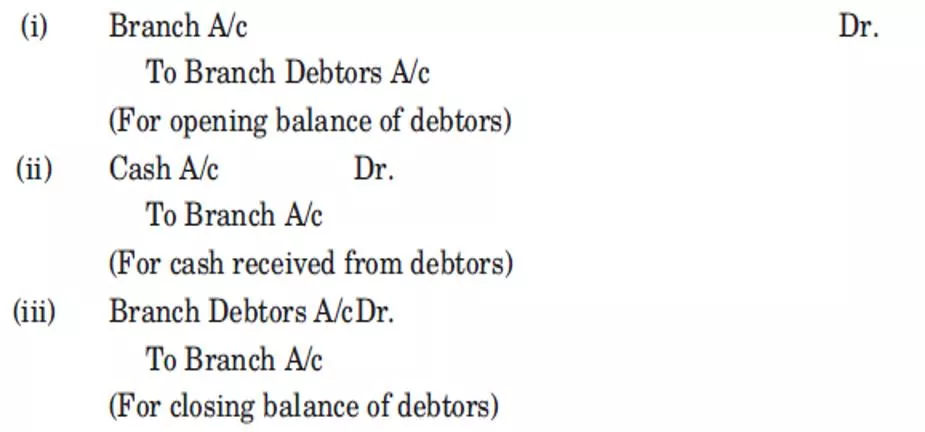

(i) Opening balance of debtors

(ii) Cash received from debtors

(iii) Closing balance of debtors

For the above items, the following journal entries are made by the

H.O.:

3

Posting in Branch Account :

The posting of above entries in branch account to be included is as

following:

The effect of posting of three items in branch account is that net

sale are automatically credited. In other words, sales returns,

discount and allowances allowed, bad debts have already been

deducted from sales. Hence no entry is required to be passed by

the head office in branch account in respect of the following :

(i) Goods sold on credit

(ii) Goods returned by debtors

(iii) Discount allowed to debtors

(iv) Bad debts written off

(v) Allowance allowed to debtors

4

(C) When goods are supplied to branch by head office at invoice or

selling price :

Sometimes goods are sent to branch by the head office at a price

higher than cost price. For example, if cost of goods is ` 8,000 and

goods are invoiced at a profit of 20% on cost, the perform invoice

will show the value of goods at ` 9,600. The following are the

advantages of invoicing goods at invoice price :

(i) It is possible to maintain secrecy about the actual cost and

profits, from branches personnel.

(ii) The branch can be directed to sell the goods at the invoice

price only or more.

(iii) control over stock with the branch becomes slightly easier.

When goods are invoiced at invoice price, question will be

attempted in the same manner as discussed under cost price

method but opening stock, goods supplied to branch, goods

returned by branch and closing stock are to be shown at invoice

price and not at cost price.

5

When goods are invoiced at invoice price, question will be attempted in

the same manner as discussed under cost price method but opening stock,

goods supplied to branch, goods returned by branch and closing stock are

to be shown at invoice price and not at cost price.

While calculating the branch profit or loss, adjustment entries are required

to be made in the branch Account for profit included in the above

mentioned items so the branch account shows true profit or loss. Hence,

the following adjustment entries are to be passed for inflated price,

i.e.,

difference between invoice price and cost price :

6

Thank You

Thank You

7

Branch accounting involves recording transactions between the head office and branches, including goods sent, sales, debtors, and profits. Entries for credit sales, invoice pricing, and adjustments are crucial for accurate branch accounts. The process ensures proper tracking of branch activities and financial performance.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

You are allowed to download the files provided on this website for personal or commercial use, subject to the condition that they are used lawfully. All files are the property of their respective owners.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.

E N D

Presentation Transcript

WELCOME Class: B.Com Part-1 Subject: Financial Accounting TOPIC: Branch Accounts Part - 3 Prepared By Dr. SHAHID IQBAL Guest Faculty Marwari College, Darbhanga, Mobile No. and Whatsup No. : 7004160257 Email ID: shahidlnmu@gmail.com 1

(B) Branch receiving goods from head office at cost price and making both cash and credits sales : If branch is authorised to sale goods cash as well as credit, the following entries are also included in respect of credit sales in addition to the above entries discussed earlier : (i) Opening balance of debtors (ii) Cash received from debtors (iii) Closing balance of debtors For the above items, the following journal entries are made by the H.O.: 2

Posting in Branch Account : The posting of above entries in branch account to be included is as following: The effect of posting of three items in branch account is that net sale are automatically credited. In other words, sales returns, discount and allowances allowed, bad debts have already been deducted from sales. Hence no entry is required to be passed by the head office in branch account in respect of the following : (i) Goods sold on credit (ii) Goods returned by debtors (iii) Discount allowed to debtors (iv) Bad debts written off (v) Allowance allowed to debtors 3

(C) When goods are supplied to branch by head office at invoice or selling price : Sometimes goods are sent to branch by the head office at a price higher than cost price. For example, if cost of goods is ` 8,000 and goods are invoiced at a profit of 20% on cost, the perform invoice will show the value of goods at ` 9,600. The following are the advantages of invoicing goods at invoice price : (i) It is possible to maintain secrecy about the actual cost and profits, from branches personnel. (ii) The branch can be directed to sell the goods at the invoice price only or more. (iii) control over stock with the branch becomes slightly easier. When goods are invoiced at invoice price, question will be attempted in the same manner as discussed under cost price method but opening stock, goods supplied to branch, goods returned by branch and closing stock are to be shown at invoice price and not at cost price. 4

When goods are invoiced at invoice price, question will be attempted in the same manner as discussed under cost price method but opening stock, goods supplied to branch, goods returned by branch and closing stock are to be shown at invoice price and not at cost price. While calculating the branch profit or loss, adjustment entries are required to be made in the branch Account for profit included in the above mentioned items so the branch account shows true profit or loss. Hence, the following adjustment entries are to be passed for inflated price, i.e., difference between invoice price and cost price : 5

Branch receiving goods from head office at cost price")

When goods are supplied to branch by head office at")