First-Time Homebuyer Assistance Program for New Construction by Utah Housing Corporation

Explore the First-Time Homebuyer Assistance Program offered by Utah Housing Corporation for new construction properties in Utah. This program features FAQs, definitions, qualifying criteria, and information on applying through approved participating lenders.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. Download presentation by click this link. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

E N D

Presentation Transcript

First-time Homebuyer Assistance Program (New Construction) UTAH HOUSING CORPORATION JULY 2023 www.utahhousingcorp.org 1

Frequently Asked Questions We have added the First-time Homebuyer Assistance Program FAQ to our homepage 2 www.utahhousingcorp.org

Frequently Asked Questions We encourage you to read through the First-time Homebuyer Assistance Program FAQ it will answer many of your questions. Definitions Application Terms Repayment 3 www.utahhousingcorp.org

First-time Homebuyer Definition First-time homebuyer - 42 U.S. Code 12852 defines a first-time homebuyer as an individual who (and whose spouse). 1) has had no ownership in a principal residence during the 3-year period ending on the date of purchase of the property. 2) is a displaced homemaker, who except for owning a home with his or her spouse or residing in a home owned by the spouse, meets the requirements of #1. 3) is a single parent who except for owning a home with his or her spouse or residing in a home while married, meets the requirements of #1. A Recipient must have been a resident of Utah for at least 12 months before closing the loan. 4 www.utahhousingcorp.org

Qualifying Mortgage Loan Definition A qualifying mortgage loan means a loan that is purchased and serviced by Utah Housing and secured by a recorded Deed of Trust in the county where the home is located. This can be any eligible first mortgage loan available through Utah Housing and its Participating Lenders. The Assistance Program loan is a 0% interest, no-monthly-payment loan secured by a recorded Deed of Trust and evidenced by a Subordinated Note. 5 www.utahhousingcorp.org

Qualifying Residential Unit Definition A qualifying residential unit is defined as: A residential unit that is: located in Utah; new construction or newly constructed but not yet inhabited; financed by a qualifying mortgage loan; owner-occupied upon purchase; and purchased for an amount that does not exceed $450,000 A single-family home, condominium, townhome, manufactured, or modular home on a permanent foundation. 6 www.utahhousingcorp.org

How do I Apply? First-Time Homebuyer (FTHB): will contact a Utah Housing Corporation Approved Participating Lender to credit qualify for the First-time Homebuyer Program (New Construction program). Utah Housing Participating Lender: The lender credit-qualifies the FTHB for a Utah Housing First Mortgage and the Assistance Program Reservation Request. The lender will follow the corresponding Utah Housing loan program to determine income limits. 7 www.utahhousingcorp.org

How do I Apply? The lender obtains the signed First-time Homebuyer Assistance Program Application Disclosure and the First Time Homebuyer Assistance Program Homebuyer Request to Reserve Funds from the Homebuyer. The lender completes and signs the First-time Homebuyer Assistance Program Lender Reservation Request and Lender Credit Qualified Certification. The Lender enters the Reservation Request Information into Utah Housing s PowerLender system and obtains a Utah Housing loan number. Utah Housing reviews the documents and if approved a Reservation is issued. The Reservation is valid for 90 days. 8 www.utahhousingcorp.org

How do I Apply? All documents provided to Utah Housing should be sent securely. Either through the PowerLender Portal By clicking the paperclip and adding documents. OR secure email to grantprograms@uthc.org. 9 www.utahhousingcorp.org

Transfer of Reservation A builder may have a preferred lender they work with. Because of this, the Reservation may need to be transferred to another lender. The FTHB or the lender may be required to pay a $250 transfer fee to Utah Housing. 10 www.utahhousingcorp.org

Transfer of Reservation To transfer a Reservation to a new lender, Utah Housing will require: 1) A written letter from the FTHB requesting the Reservation be transferred, including an explanation. 2) Authorization from the lender whose name is on the original Reservation. 3) The new lender will enter their data in the PowerLender System and obtain a new Utah Housing loan number. 4) The new lender provides a credit underwriting approval and submits a new Reservation Request. 11 www.utahhousingcorp.org

Transfer of Reservation With a transfer, the Reservation and expiration dates will remain the same as the original Reservation. 12 www.utahhousingcorp.org

Time Line The Reservation is valid for 90 days. At the end of 90 days, the lender contacts Utah Housing to extend or cancel the Reservation, based on the following conditions. The Lender completes and signs the First-time Homebuyer Lender Credit Qualified Certification The Lender obtains from the FTHB an executed Real Estate/Construction Purchase Agreement (REPC) and FTHB identifies a property Utah Housing reviews the documents and if conditions are met the Reservation is extended 120 days Extension #1 13 www.utahhousingcorp.org

Timeline At the end of the 90 days, if the conditions are not met the Reservation is canceled. The FTHB may reapply after obtaining a signed Real Estate Purchase Contract (if Assistance Program funds are still available). 14 www.utahhousingcorp.org

Timeline End of First 120 day extension 1) The Lender completes and signs the First-time Homebuyer Lender Credit Qualified Certification 2) The lender provides satisfactory evidence of construction progress (i.e. photos, inspections, etc.) 3) Utah Housing reviews the documents and if conditions are met the Reservation is extended 120 days Extension #2 OR The Reservation is canceled if conditions are not met the 15 www.utahhousingcorp.org

Timeline End of extension #2 1) The lender provides satisfactory evidence of construction progress (i.e. construction schedule, anticipated completion and certificate of occupancy date, etc.). 2) The lender certifies FTHB continues to be credit-qualified and meet Program guidelines. 3) The lender provides expected closing date. 4) The third and final extension is approved for 120 days. Extension #3 OR The Reservation is canceled if conditions are not met 16 www.utahhousingcorp.org

Timeline End of extension #3 The loan should close before the expiration of the third extension. If the loan has not closed and the Assistance Program funds wired to the Title Company the lender will contact Utah Housing with the closing date. Other documentation may be required. The Title Company provides the request for Program funds to Utah Housing at least 3 days prior to the closing date. Additional extensions may be granted per Utah Housing approval. 17 www.utahhousingcorp.org

Timeline Before Utah Housing wires funds, the lender will be required to provide verification the FTHB meets the requirements listed in the Program. 18 www.utahhousingcorp.org

Funding the Assistance The Title Company completes and signs the FTHB Assistance Program Funding (Wire) Request and Certification. Ye Old Title Company The request must be made to Utah Housing at least three business days before closing. 19 www.utahhousingcorp.org

Funding the Assistance Utah Housing will prepare and send to the Title Company a First-time Homebuyer Assistance Program Note and Deed of Trust to be executed by the Recipient(s) at closing. The funds will be sent directly to the Title Company. The wired funds must be applied to the Recipients down payment and/or closing costs, disclosed on the First Mortgage Closing Disclosure, and recorded concurrently in the second or third position, after the Utah Housing Deed(s). 20 www.utahhousingcorp.org

Purchase of the Loan A Utah Housing Underwrite will review and verify the loan. 1) Closing Disclosure includes the Program amount (must match wire). 2) FTHB did not receive cash back. 3) The Deed was recorded in accurate order. 4) The original Note has been signed, at closing, and the original has been received by Utah Housing. 5) Meets the Requirements, qualifying mortgage loan. 21 www.utahhousingcorp.org

Purchase of the Loan Utah Housing will 1) Retain and secure the Original Note and a copy of the recorded Deed of Trust. 2) Record a release of lien. 3) Funds received from the payoff may be used to assist another eligible FTHB. 22 www.utahhousingcorp.org

Repayment of the Program If the Recipient completes a sale or refinance the Recipient shall repay an amount equal to the lesser of: The amount of Program funds the Recipient(s) received; or 50% of the home equity amount. "Home equity amount" means the difference between: In the case of a sale. The sales price for which the qualifying residential unit is sold by the recipient in a bona fide sale to a third party with no right to repurchase; or in the case of a refinance, the current appraised value of the qualifying residential unit; and the total payoff amount of any qualifying mortgage loan that was used to finance the purchase of the qualifying residential unit. 23 www.utahhousingcorp.org

Tax Matters FTHB should consult with a tax professional regarding the potential effect of repayment of the Program on the FTHB federal and state taxes. FTHB may receive an IRS Form 1099, if FTHB fails to satisfy the terms of the Program and fails to fulfill all repayment obligations. 24 www.utahhousingcorp.org

Repayment of the Assistance It is important for lenders to understand the timeline for a borrower. How the Assistance is used by the FTHB will depend on each homebuyer. Some may apply the $20,000 as Principal Reduction, immediately having the equity to repay, if they sell in a short period of time. Others may use the $20,000 to buy down the interest rate, pay closing costs, or apply the funds to the upfront mortgage insurance. There will be less home equity, but the reduction in the payment may help with qualifying the FTHB. OR they may choose a combination of all. 25 www.utahhousingcorp.org

Repayment of the Assistance The amount of Program funds the Recipient(s) received; or 50% of the home equity amount. Have equity of $41,000 would have to repay $20,000 Have equity of $40,000 would have to repay $20,000 Have equity of $20,000 would have to repay $10,000 26 www.utahhousingcorp.org

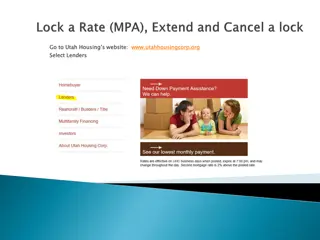

Calculating the Monthly Payment The Monthly Payment Calculator is a beneficial tool. 27 www.utahhousingcorp.org

Monthly Payment Calculator Enter the loan amount The rate for that day will be calculated. The rate and payment adjusts per the entered credit score. 28 www.utahhousingcorp.org

Interest Rates Rates are subject to change at any time, check the Utah Housing website for today s rates. Click to see daily Rate Adjustments & Buydown costs 29 www.utahhousingcorp.org

FHA/VA Mortgage Questions? Please feel free to email grantprograms@uthc.org or call 1-801-902-8200 30 www.utahhousingcorp.org