Understanding Various Aspects of Insurance in the Financial Sector

Insurance serves as a vital tool for managing financial risks and protecting against uncertainties. This article delves into types of insurance, advantages, regulatory issues, and the role of credit rating agencies. It covers life insurance, property insurance, and marine insurance among others, highlighting their significance in safeguarding against loss. Expert insights from Dr. N. Isvarya shed light on key concepts in the field of insurance.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. Download presentation by click this link. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

E N D

Presentation Transcript

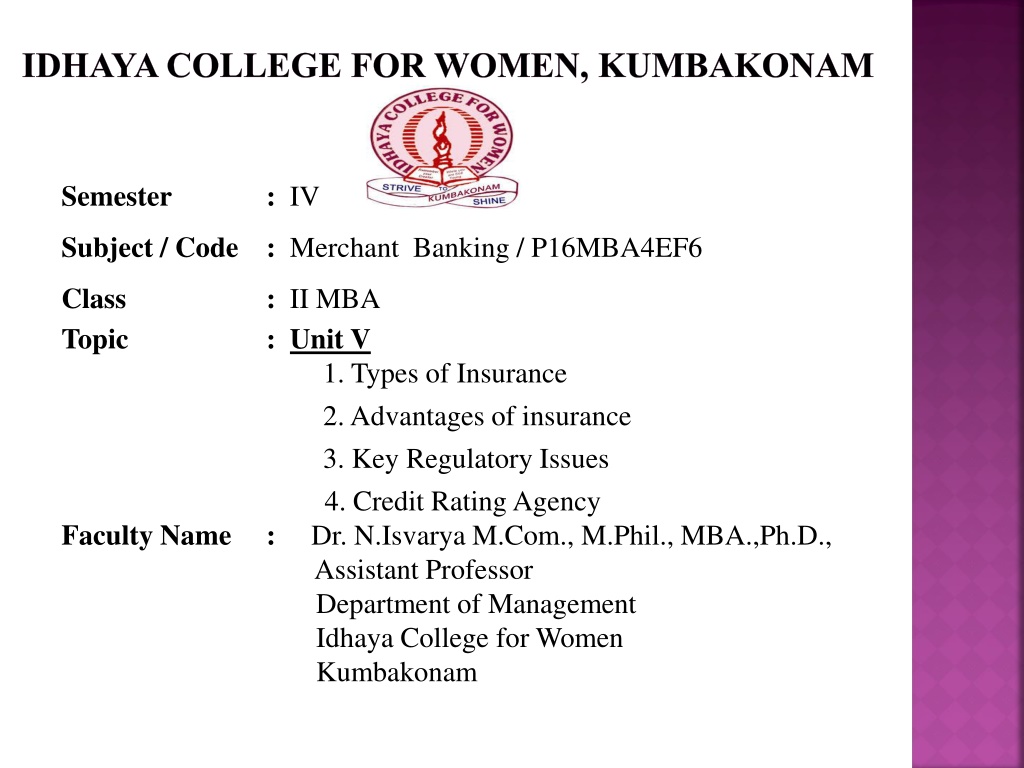

IDHAYA COLLEGE FOR WOMEN, KUMBAKONAM Semester : IV Subject / Code : Merchant Banking / P16MBA4EF6 Class Topic : II MBA : Unit V 1. Types of Insurance 2.Advantages of insurance 3. Key Regulatory Issues 4. Credit RatingAgency : Dr. N.Isvarya M.Com., M.Phil., MBA.,Ph.D., Assistant Professor Department of Management Idhaya College for Women Kumbakonam Faculty Name

INSURANCE Insurance is a means of protection from financial loss. It is a form of risk management, primarily used to hedge against the risk of a contingent or uncertain loss. An entity which provides insurance is known as an insurer. Insurance company , insurance carrier or underwriter.

MAIN OBJECTIVES OF INSURANCE It is a financial guard against unpredictable life occurrences in short, when you buy an insurance policy, you make monthly payment, called premiums, to purchase protection from monetary repercussions related to things like accident, illness or even death.

TYPES OF INSURANCE Life insurance or personal insurance Property insurance Marine insurance Fire insurance Liability insurance Guarantee insurance Social insurance

LIFE INSURANCE Insurance that pay out a sum of money either on the death of the insured person or after a set period It is a form of insurance in which a person makes regular payment to an insurance company, in return for sum of money to be paid to them after a period of time, or to their family if they die. I have also taken out a life insurance policy on him just in case.

PROPERTY INSURANCE It provides insurance against most risk to property. Such as fire, theft and some weather damage. This includes specialized form of insurance such as fire insurance. Flood insurance, earthquake insurance, home insurance, or boiler insurance.

MARINE INSURANCE It covers the loss or damage of ship, cargo, terminals, and any transport by which the property is transferred, acquired, or held between the point of origin and the final destination. Cargo insurance is the sub branch of marine insurance, through marine insurance also includes onshore and offshore exposed property, hull, marine casualty, and marine liability.

FIRE INSURANCE It is a property insurance that covers damage and losses caused by fire. The purchases of fire insurance in addition to homeowners or property insurance help to cover the cost of replacement, repair, or reconstruction of property, above the limit set by the property insurance policy

LIABILITY INSURANCE It provides the insured party with protection against claims resulting from injuries and damage to people or property. Liability insurance policy covers both legal cost and payouts for which the insured party would be responsible if found legally liable.

GUARANTEE INSURANCE Financial guarantee insurance. An insurance policy covering a lender from liability resulting from the failure of the borrower to repay the loan. It may also cover losses from a decrease in interest rates to the detriment of the lender. It is similar to surety or co-signed loan.

SOCIAL INSURANCE Protection of the individual against economic hazards such as unemployment, old age, or disability in which thee government participates or enforces the participation of employers and affected individual.

ADVANTAGES OF INSURANCE Provides economic protections Share risk Maintains standard of living Encourages saving Eliminates dependency Grants loan Create employment opportunity Promotes foreign trade Help to operate business smoothly Help to reduce inflation Help to develop economy

DISADVANTAGES OF INSURANCE It does not compensate all type of losses which caused biasness to insured by insurance company It takes more time to provide financial compensation because lengthy legal formalities Although insurance encourage savings, it does not provide the facility that are provided by bank In internally tries to compensate as less as possible to the sufferer with the aim of maximizing profit rather than maximizing well-being of the insured

It may lead to the crimes in the society as the beneficiaries of the policy may be tempted to commit crime to receive the insured amount. Sometimes , the total amount of premium might be higher than the policy amount receivable on maturity.

IMPORTANT OF INSURANCE Buying insurance is important as it ensure as it ensure that you are financially secure to face any types of problem in life, and this is why insurance is very important part of financial planning. A general insurance company offers insurance policies to secure health, travel, motor vehicle, and home.

INSURANCE INDUSTRY IN INDIA The insurance industry of India consist of 57 insurance companies of which 24 are in life insurance business and 33 are non-life insurers. Among the life insurance, corporation (LIC) is the sole public sector company. Apart from that, among the non-life insurers there are six public sector insurers. In addition to these, there is sole nation re-insurer, namely, general insurance corporation of India. Other stakeholders in Indian insurance market includes agents, brokers, surveyors and third-party administrators servicing health insurance claims. life insurance

OTHER FINANCIAL SERVICES Banking Advisory. Expert advisory services help both people and organization with a variety of tasks Wealth management Mutual funds

CREDIT CARD It is a payment card issued to users to enable the cardholders to pay a merchant for goods and services based on the cardholder s promise to the card issuer to pay them for the amount plus the other agrees charges.

CREDIT RATING A credit rating is a quantified assessment of the creditworthiness of a borrower in general term or with respect to a particular debt or financial obligation. A credit rating can be assigned to any entity that seeks to borrow money an individual, corporation, state or provincial authority, or sovereign government.

PROCESS OF CREDIT RATING Request from issuer an analysis Rating committee Communication to management and appeal Pronouncement of rating Monitoring of the assigned rating Rating watch Rating coverage Rating score

CREDIT RATING METHODOLOGY Business analysis Economic analysis Financial analysis Management evaluation Graphical analysis Fundamental analysis

REGULATORY FRAMEWORK FOR CREDIT RATING Credit rating is entirely a new concept in the history of India corporate sector and is intended for investors guidance and protection. It came into limelight only when securities exchange board of India (SEBI) made the credit rating compulsory for the Indian companies. The SEBI regulations, 1999 empower the SEBI to regulate credit rating under the SEBI.

KET REGULATORY ISSUES Appropriate level of external oversight Quality of the rating process Monitoring and updating of rating Conflicts of internet Disclosure issues Adequacy of organizational resources Over-reliance on credit rating by investors.

ROLE OF REGULATORY IN CREDIT RATING Conditions for setting up a credit rating agency Process of getting certificate of registration Obligations of credit rating agency towards SEBI Conditions to be followed while assigning rating Restriction on rating Liability in case of default Internal audit of credit rating agency Transparency and disclosure norms

CREDIT RATING AGENCY It a company that assign credit ratings, which rate a debtor s ability to pay back making timely principle and internet payments and the likelihood of default.

CREDIT RATING REGULATORY FRAMEWORK It is an important financial intermediary acts as a gatekeeper to the financial markets by financial markets by influencing the investor and regulating the issuer s access to the financial markets. In India, securities and exchange board of India (SEBI) brought rating agencies under its regulatory ambit in 1999.