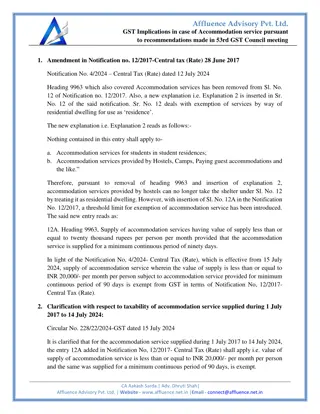

Understanding GST Implications for Investors and Traders

Presentation by Anandh Sundar discusses the impact of GST on sectors like food, changes in rates, luxury cess, fiscal revenue, and more. It delves into how GST affects pricing, margins, and consumer behavior within various industries. The presentation highlights key considerations for investors and traders when navigating the GST landscape.

Uploaded on Oct 05, 2024 | 0 Views

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. Download presentation by click this link. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

E N D

Presentation Transcript

GST For Investors and Traders Anandh Sundar Presented at EIN Meetup, CCI(Mumbai)-3 Feb 2018 Disclaimer: This presentation reflects my individual views on general market conditions/fiscal policy and is not investment advice. Please act at your own risk . While copy-left permission to share freely applies, the contents may not be published in any media source without prior consent.

Agenda GST imposed on a sector-good or bad (Eg Renewable Energy) GST Rate increase/decrease on Sector(eg Restaurents-18% to 5%) Imposition/Change of Luxury cess (eg Auto, Cigarretes) Fiscal Revenue/Tax Collection Numbers Overall Numbers vs Centre/State Split Contingent Liabilities/Transition Credit SMEs Consumers Unorganized Sectors Others In Conclusion

GST imposed on a sector-good or bad-Food In scenario of labour intensive industry or where inputs less taxed than outputs, GST results in consumer price inflation GST Composition Vendor(1%) Material Labour Depreciation SG&A Total Markup @25% Customer pricing(Pre Tax) Pre GST GST(Non Credit) Total Remark 20 30 10 30 90 3.6 23.6 30.0 11.8 35.4 100.8 25.2 126.0 1.8 5.4 10.8 Assume 1% GST passed on Customer pricing(With 1% GST) 127.3 Post GST Material Labour Depreciation SG&A Total Pre GST GST(Non Credit) Total Remark 20 30 10 30 90 0 0 0 0 0 20.0 30.0 10.0 30.0 90.0 Profit preserved in absolute terms Markup @25% Customer pricing(Pre Tax) Retail Consumer pricing(post tax) 25.2 115.2 135.94 With 18% GST charged Consumer price inflation 7%

GST Rate increase/decrease on Sector(eg Restaurents-18% to 5%) GST at 18% with full input credit Pre GST GST(Non Credit) Total Remark Material 25 25.0 Labour 20 20.4 Depreciation 6 5.5 SG&A 39 39.3 Total 90 90.2 Markup @10% 9.0 Customer pricing(Pre Tax) 99.2 Company will achieve 6.3% growth in sales without improving its margins, just to offset lost input tax credit Assume 18% GST passed on Company J reported double digit SSG growth on back of tepid earlier growth. Some bit of this is due to GST, and is not highlighted by company Customer pricing(With 18% GST) 117.0 GST at 5% without input credit Material Labour Depreciation SG&A Total Pre GST GST(Non Credit) Total Remark Assume 18% on 50% None as on-roll Assume 18% on 50% Assume 18% on 50% 25 20 6 39 90 2.25 - 0.50 3.53 - 27.2 20.4 6.0 42.8 96.5 Profit preserved in absolute terms versus earlier Markup @10% Customer pricing(Pre Tax) Retail Consumer pricing(post tax) 110.74 9.0 105.5 With 5% GST charged Consumer price change Reported Revenue change -5.4% Due to tax rate change 6.3% GST neutral price hike

GST Cess The cess goes to a fund meant to compensate states for revenue losses in the first five years of the GST regime. Sin Goods such as aerated drinks, coal, tobacco, automobiles and the ambiguous category of other supplies Jul 2017-Increase Cess on cigarettes to pre-GST rates Sep-2017- The goods and services tax (GST) Council on Saturday raised the cess on mid-sized to large cars and SUVs in the range of 2-7 percentage points but kept the tax burden lower than pre-GST levels Dec 2017- The Lok Sabha has approved a bill to hike Cess on luxury vehicles from 15 per cent to 25 per cent.

Fiscal Revenue Cross Matching with all statutory data(IEM/PAN/IEC) & Aadhar Linkage with customs data(Shipping bill); E-Way Bill & acceptance clause-Game changer for evasion Potential Linkages for employee data, electricity, direct tax data Initial Revenue boost lower so compliance focus. Also, impact of transition credit not fully done

SMEs Positives 6 month period for customer to pay or risk losing input credit Composition Scheme Reliable Record for lending-Erode NBFC moat for SMEs Negatives Practically large customers/transporters insist on GST to avoid additional work of reverse charge or generating E-way bill. So threshold less meaning Returns/Compliances-Need to upgrade accounting system as well

Consumers Able to complain about perceived profiteering Anti dumping duties now data backed so lesser chance of industries fudging data to protect their profit pools->Positive for consumer Under GST rules, the central government notified in June last year that any excess profit a manufacturer makes by charging a higher price should be credited to the Consumer Welfare Fund. But there is little clarity on how this transfer should happen and under what circumstances EXAMPLE: India s largest packaged consumer goods maker earmarked Rs119 crore in the December quarter to be paid to the government because it could not immediately lower prices after the goods and services tax (GST) on several products was reduced on 15 November.

Unorganized Sector Brought into the limelight due to reverse charge compliances especially during import of goods E Way Bill Introduced Wef 1 Feb 2018 will ensure EWB for movement of goods If above Rs 50,000 value For any purpose (Including repairs/jobwork) Between any premises(even if owned by same person) To be prepared by transporter if not done by supplier or customer Potential to compare EWB data with GST filings and detect lapses However, composition scheme is a bonus for first time tax payers

Other points GST Input Credit restriction (eg Restaurents/Energy/BFSI) Procedural Relaxation/Issues Composition Scheme, WayBill, Returns Boost to Digital India Easier Lending- Digital Transaction trail of Gross Profit (Ex Employee Costs/Utilities) E-Payment/E-Ledger/E-Filing-Make people conversant with it Cloud based working of professional firms

Conclusion Second Order effects relevant Eg Imports value chain Cascading effect still relevant due to impact of other duties/cess Anti Dumping duties included in taxable value of imported goods Earnings volatility due to anti profiteering(Eg HUL) Ease of doing business not yet fully visible unless visibility on Transition Credit(Pre GST Credit) Input Credit Matching Way Bill Tax Hikes/Cess changes