GST Implications in case of Accommodation service in 53rd GST Council meeting

Notification No. 4/2024 amends the GST exemption rules for accommodation services effective 15 July 2024. Heading 9963 is removed from Notification 12/2017, and a new explanation excludes certain accommodations like hostels from exemptions. A new e

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

You are allowed to download the files provided on this website for personal or commercial use, subject to the condition that they are used lawfully. All files are the property of their respective owners.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.

E N D

Presentation Transcript

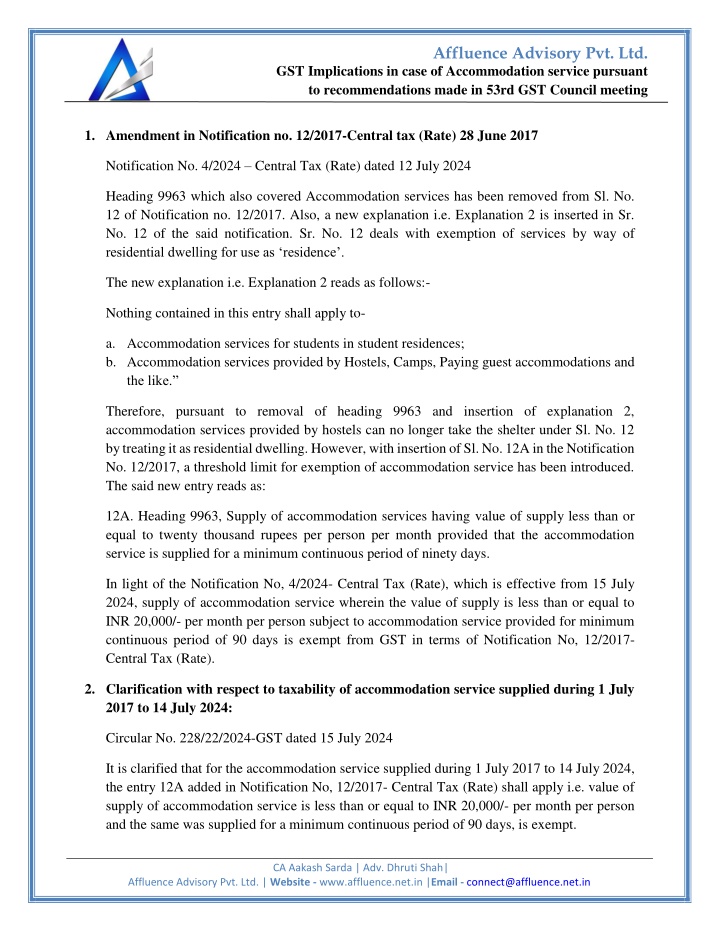

Affluence Advisory Pvt. Ltd. GST Implications in case of Accommodation service pursuant to recommendations made in 53rd GST Council meeting 1.Amendment in Notification no. 12/2017-Central tax (Rate) 28 June 2017 Notification No. 4/2024 Central Tax (Rate) dated 12 July 2024 Heading 9963 which also covered Accommodation services has been removed from Sl. No. 12 of Notification no. 12/2017. Also, a new explanation i.e. Explanation 2 is inserted in Sr. No. 12 of the said notification. Sr. No. 12 deals with exemption of services by way of residential dwelling for use as residence . The new explanation i.e. Explanation 2 reads as follows:- Nothing contained in this entry shall apply to- a.Accommodation services for students in student residences; b.Accommodation services provided by Hostels, Camps, Paying guest accommodations and the like. Therefore, pursuant to removal of heading 9963 and insertion of explanation 2, accommodation services provided by hostels can no longer take the shelter under Sl. No. 12 by treating it as residential dwelling. However, with insertion of Sl. No. 12A in the Notification No. 12/2017, a threshold limit for exemption of accommodation service has been introduced. The said new entry reads as: 12A. Heading 9963, Supply of accommodation services having value of supply less than or equal to twenty thousand rupees per person per month provided that the accommodation service is supplied for a minimum continuous period of ninety days. In light of the Notification No, 4/2024- Central Tax (Rate), which is effective from 15 July 2024, supply of accommodation service wherein the value of supply is less than or equal to INR 20,000/- per month per person subject to accommodation service provided for minimum continuous period of 90 days is exempt from GST in terms of Notification No, 12/2017- Central Tax (Rate). 2.Clarification with respect to taxability of accommodation service supplied during 1 July 2017 to 14 July 2024: Circular No. 228/22/2024-GST dated 15 July 2024 It is clarified that for the accommodation service supplied during 1 July 2017 to 14 July 2024, the entry 12A added in Notification No, 12/2017- Central Tax (Rate) shall apply i.e. value of supply of accommodation service is less than or equal to INR 20,000/- per month per person and the same was supplied for a minimum continuous period of 90 days, is exempt. CA Aakash Sarda | Adv. Dhruti Shah| Affluence Advisory Pvt. Ltd. | Website - www.affluence.net.in |Email - connect@affluence.net.in

Affluence Advisory Pvt. Ltd. GST Implications in case of Accommodation service pursuant to recommendations made in 53rd GST Council meeting Disclaimer:This article provides general information existing at the time of preparation and we take no responsibility to update it with the subsequent changes in the law. The article is intended as a news update and Affluence Advisory neither assumes nor accepts any responsibility for any loss arising to any person acting or refraining from acting as a result of any material contained in this article. It is recommended that professional advice be taken based on specific facts and circumstances. This article does not substitute the need to refer to the original pronouncement CA Aakash Sarda | Adv. Dhruti Shah| Affluence Advisory Pvt. Ltd. | Website - www.affluence.net.in |Email - connect@affluence.net.in