Understanding Recent Judgments and Rulings on GST Issues

Dive into the latest judgments and rulings regarding GST issues, focusing on topics such as Input Tax Credit discrepancies, supplier obligations, and High Court verdicts. Explore real-life cases like Suncraft Energy Ltd. in Calcutta High Court, analyzing repercussions and legal perspectives. Gain insights from expert CA Indranil Das on GST Pleading and Practice, with a deep dive into relevant sections of the CGST Act. Stay informed on the evolving landscape of GST regulations and compliance.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. Download presentation by click this link. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

E N D

Presentation Transcript

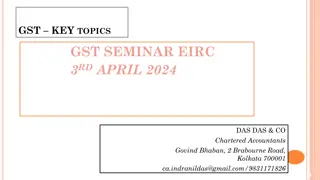

GST KEY TOPICS GST SEMINAR EIRC 3RDAPRIL 2024 DAS DAS & CO Chartered Accountants Govind Bhaban, 2 Brabourne Road, Kolkata 700001 ca.indranildas@gmail.com/9831171826 DAS DAS & Co Chartered Accountants

ABOUTTHESPEAKERS CA Indranil Das, FCA, DISA. Certificate in GST Pleading and Practice ( ICAI) CA Indranil Das is a practicing Chartered Accountant in practice for the past 12 years. He attained fellowship in the year 2016 from ICAI. He is extensively practicing in Direct and Indirect Taxation. A member of Direct Tax Professional Association Kolkata and Accountants Library Kolkata. He has attained Diploma in Information Systems Audit from ICAI. Specializes in GST Pleading and Practice and represents clients before Advance Ruling Authority, Adjudicating Authority. Has provided corporate trainings to large corporates like BSNL, HPCL,SBI to name a few. . DAS DAS & Co Chartered Accountants

TOPICS FOR DISCUSSION ITC LATEST JUDGEMENTS

SUNCRAFT ENERGY LTD ( CAL HC) ISSUE: Some of the Invoices of the said supplier was not reflected in GSTR 2A which was claimed by the Appellant for the Financial Year 2017-18. ( 3B Vs 2A Mismatch) RELEVANT SECTIONS: Section 16(2) of the CGST Act 2017. VERDICT: The Calcutta High Court had held that the company cannot be denied ITC by citing the ground that the supplier has not remitted the tax unless there are situations where the GST department cannot collect tax from the supplier.The High Court ruled that before directing the company to reverse ITC, GST authorities ought to have taken action against the supplier. Sec 16(2) Being a Non- Obstane Clause- a) Possession of Tax Invoice, Reciept of Goods or Services, the tax charged has been actually paid to the Government, either in cash or through utilisation of ITC admissible in respect of such supply and he has furnished the return u/s 39. The Petitioner satisfied all points and paid tax to the supplier Relying on SC Judgement on Bharti Airtel Ltd Vs Union of India. Press Release-18.10.2018 and 4.05.2018 Reliance was made on Arise India Ltd Vs Commissioner of Trade and taxes Delhi HC- For default committed by the seller, the purchasing dealer cannot be denied the ITC and asks questions whether it is a violation of Art 14 of the Constitution.

SUNCRAFT ENERGY LTD ( CAL HC) Press Release-18.10.2018 and 4.05.2018 The Press Release on 18.10.2018 states that it is just a Facilitation of viewing 2A and since not 2B coming into the picture, relying on 2A is not as per law The Press Release on 04.05.2018 states that- No Automatic Reversal on Non Payment of Tax by the seller In case of default of tax by the seller, recovery shall be made from the seller first. The option of Reversal is also available only in case of Missing Dealer, Closure of Business, Supplier not having enough assets. If there is collusion between buyer and seller, then the dept may proceed as per law. The Order of the State Tax was set aside and was asked to first take action against the erring dealer .

GUNJAN BINDAL VS COM OF CGST-DELHI HC- NOV 17-2023/(JAGDISHBANSALVSUOI) ISSUE: Can the Department seize cash u/s 67 of the CGST Act, 2017 RELEVANT SECTIONS: Section 67 of the CGST Act, 2017. VERDICT: a) The Delhi High Court had held that amount of cash seized be remitted along with interest thereby holding that, the Revenue Department has no power to seize cash under Section 67 of the Central Goods and Services Tax Act,2017. (b) It is important to note that even cash must be secreted to qualify for the seizure but, more importantly, cash is not goods liable to confiscation under section 130(1) but are things which are considered useful or relevant by the Authorized Officer to carrying out any further proceedings . What, therefore, can be the use or relevance of cash to be seized? (c ) Cash seizure does not directly point to proceeds from unaccounted sales. That would have been easy but the Legislative wisdom is that (i) Evasion of tax is a must for proceedings under section 67 to be with the jurisdiction and lawful and (ii) No presumption flows in favor of the Revenue, especially, when cash may be treated to be things and not consideration from supply . After all, things seized can only be if they are useful or relevant for that Authorized Officer in carrying out any further proceedings .

M/S A.S.E INDIA VS UNION OF INDIA- NOV 6 2023-TELEGANA HIGH COURT. ISSUE: Whether ITC can be blocked when no Assessment order is issued? RELEVANT SECTIONS: under Section 74 of the CGST Act or Rule 86A of the CGST Rules. 5 reasons of Rule 86A for which Pre Emptive and Emergency Power is used by the Commissioner VERDICT: a) The Honorable Telangana High Court noted that the Impugned notice issued pertains to the blocking of the electronic credit ledger of the Petitioner under Rule 86A of the CGST Rules. b) Also, nowhere it has been stated that the Impugned Notice is an intimation pertaining to proceedings initiated under Section 74 of the TNGST Act. Further, noted that the Impugned Notice issued is not an order of attachment of the ITC account of the Petitioner. Further, noted that the Impugned Notice issued is not an order of attachment of the ITC account of the Petitioner Moreover, this decision by the Commissioner or any other authorized officer is a nonappealable decision, although not specified u/s 121 of the Act.

M/S ADVENT INDIA PE ADVISORS VS UNION OF INDIA- BOMBAY HIGH COURT. ISSUE: Whether ITC can be blocked when no Assessment order is issued? RELEVANT SECTIONS: under Section 74 of the CGST Act or Rule 86A of the CGST Rules. 5 reasons of Rule 86A for which Pre Emptive and Emergency Power is used by the Commissioner VERDICT: a) Rule 86A in which AC has reasons to believe that ITC in Credit ledger is fraudulently availed or is ineligible, by reason of RP non existent, not conducting any business from the place where registration has been obtained or tax charged not paid to govt, or without any receipt of goods or services or both Such effect will cease after expirt of 1 year from the date of imposition of such restriction. Dept consistently asked for taxpayer for submission for due verification of the credit availed, it said after completion of verification if any demand is there, SCN will be issued and Unblocking will be done- Directed to lift blockage.

M/S CHUKKATH KRISHNAN PRAVEEN VS STATE OF KERALA- DEC 8, 2023- KERALA HIGH COURT ISSUE: Whether rectification in return be allowed when ITC in GSTR-3B is accounted as IGST credit instead of CGST and SGST credit erroneously? RELEVANT SECTIONS: Sec 38 of the CGST Act 2017, 39 also VERDICT: a) The Honorable High Court Allowed the Writ Petition and directed that the rectification in return should be allowed when Input Tax Credit ( ITC ) in GSTR-3B is accounted as the Integrated Goods and Services Tax ( IGST ) credit instead of the Central Goods and Services Tax ( CGST ) and the State Goods and Services Tax ( SGST ) credit erroneously. The Honorable Kerala High Court disposed of the writ petition and directed that the Representation filed by the Petitioner be treated as a Rectification application and pass the necessary order in accordance with law after granting a proper hearing to the Petitioner within a period of two months

M/S BBAINFRASTRUCTURELTDVSSENIORJCOFST- DEC 13-2023-CALCUTTAHIGHCOURT ISSUE: Whether ITC can be availed by Registered Person when returns are filed beyond statutory period stipulated u/s 16(4) of CGST Act? RELEVANT SECTIONS: Sec 16(4) of the CGST Act 2017, 16(1) of the CGST. VERDICT: a) The Honorable High Court dismissed the Writ Petition and held that Sec 16(1) of the CGST Act is an enabling provision allowing ITC and Sec 16(4) of the CGST Act, 2017 imposing restriction on the filing belated returns for availing Credit is valid in nature. The Honorable High Court relies on the SC Judgement of ALD Automotive Pvt Ltd observed that the conditions under which the concessions and benefits are given are always to be strictly construed. And the time under which a return is to be filed for the purpose of assessment of tax cannot be dependent on the will of the dealer. TVS Motor Judgement is included- ITC is a form of concession provided under the CGST Act which cannot be availed as a matter of right but only as per the terms of the statute, therefore the conditions mentioned has to be fulfilled by the dealer.

M/S BBAINFRASTRUCTURELTDVSSENIORJCOFST- DEC 13-2023-CALCUTTAHIGHCOURT In the case of Tirumalakonda Plywoods v. Assistant Commissioner- State Tax [W.P. No. 24235 of 2022 dated July 18, 2023], the central issue was whether Section 16(2) of the CGST Act, being a non-obstante clause would prevail over Section 16(4) of the CGST Act. It was further noted that Section 16 which clearly stipulates that the grant of ITC is subject to the condition stated in the CGST Act. Further, it is stated that the provision under Section 16(4) is one of the conditions making the registered person eligible to avail of ITC and is not violative of Article 300 A of the Constitution of India. Similar stand by Patna High Court in case of Gobinda Construction Vs UOI. The Supreme Court has issued a Notice against the Judgement of Honble Patna High Court in case of Gobinda Construction- Jan 3 2024 Keep a Close look at Mritunjay Kumar Vs UOI listed at Apex Court.

SEC 16(4) OF THE CGST ACT- ISSUES STILL AMBIGUITY: IS Section 16(4) is violative of Article 14 and 19(1)(g) of the Constitution of India ? Article 14 of the Constitution of India reads as under: The State shall not deny to any person equality before the law or the equal protection of the laws within the territory of India. Article 19 ( 1) (g) of Constitution of India provides Right to practice any profession or to carry on any occupation, trade or business to all citizens subject to Art. Instances where 16(4) is not considered by Government. 1. The input tax credit is allowed under section 18(1)(d) to eligible taxpayers even though they have not claimed credit within the time limit in section 16(4) of the CGST Act. ( Exempt to Taxable) 2. The input tax credit is allowed to IRPs in respect of Corporate Debtors who are undergoing the CIRP process under the Insolvency and Bankruptcy Code vide notification 11/2020-Central Tax dated 21 Mar 2020;

SEC 16(4) OF THE CGST ACT- ISSUES-2 Retrospective amendment to section 7(1)(aa) of CGST Act notified from 1 Jan 2022 and have been allowed an input tax credit for fifty-four (54) months since the retrospective amendment- Clubs and Association. The input tax credit is allowed on the restoration of registration in appeal in cases where registration was canceled and login credentials blocked due to the action of Proper Officer which came to be overturned by Appellate Authority, and all outstanding returns were filed in one go. CASES in favour of Dealer-the Honorable Madras High Court in the case of Tvl. Kavin HP Gas GraminVitrak v. The Commissioner of Commercial Taxes & Ors [W.P.(MD). Nos.7173 and 7174 of 2023 dated November 24, 2023] allowed the filing of belated returns for availing ITC in cases where the taxpayer was unable to file GSTR-3B when the registered person is not able to pay taxes on outward supply due to financial hardship. Apply the law in different treatments under different circumstance is not as per Constitutional Rights.

TVL.KAVIN HP GAS GRAMIN VITRAK VSCOMM OFCOMMTAXES- MADRASHIGHCOURT ISSUE: Whether ITC can be claimed by submitting physical FORM GSTR- 3B returns when FORM GSTR-2 was not notified? VERDICT: Yes, the Hon'ble Court held that the respondents without giving any opportunity to file the returns cannot expect the taxable person to file returns. Hence, the Respondents ought to allow the dealers to file returns manually and the writ petitions were allowed without any cost. The Honorable Madras High Court observed that if the GSTN provided an option for filing GSTN without payment of tax or incomplete FORM GSTR- 3B, the dealer would be eligible for claiming ITC. The same was not provided in the GSTN network hence, the dealers are restricted from claiming ITC on the ground of non-filing of FORM GSTR-3B within the prescribed time If the option of filing incomplete filing of FORM GSTR-3B is provided in the GSTN network the dealers would avail the claim and determine self-assessed ITC online. The Petitioner had expressed real practical difficulty. by notifying the Form GSTR-2

TVL.KAVIN HP GAS GRAMIN VITRAK VSCOMM OFCOMMTAXES- MADRASHIGHCOURT Absense of enabling mechanism the assessee should not be denied from availing credit. The Honorable Court held that the Respondents shall permit the petitioner to file manual returns whenever the petitioner is claiming ITC on the outward supply/sales without paying taxes and directed the respondents to accept the belated returns and if the returns are otherwise in order and accordance with the law, the claim of ITC may be allowed. Hence, the Impugned Orders is quashed and the writ petition is allowed. The Honorable Court relied on the judgment passed by the Punjab and Haryana High Court in the case of Hans Raj Sons v. Union of India and others [CWP No. 36393 of 2019 dated December 16, 2019], and Adfert Technologies Private Limited v. Union of India and others [CWP No. 30949 of 2018 dated November 04, 2019],

")

")

OF THE CGST ACT- ISSUES")

OF THE CGST ACT- ISSUES-2")