Loyalty Shares with Tenure Voting: Insights from the Loi Florange Experiment

Loyalty shares with tenure voting (LSTV) enhance voting rights based on holding periods, potentially impacting control mechanisms in various countries. The study examines the default rule's influence on the adoption and impact of LSTV, focusing on its availability, transparency, and implications for long-term shareholders. The research delves into the characteristics of LSTV, such as voting power dynamics, expiration upon sale, and its comparison to dual-class structures, shedding light on the French tradition and its implications for corporate governance.

Uploaded on Oct 02, 2024 | 0 Views

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

You are allowed to download the files provided on this website for personal or commercial use, subject to the condition that they are used lawfully. All files are the property of their respective owners.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.

E N D

Presentation Transcript

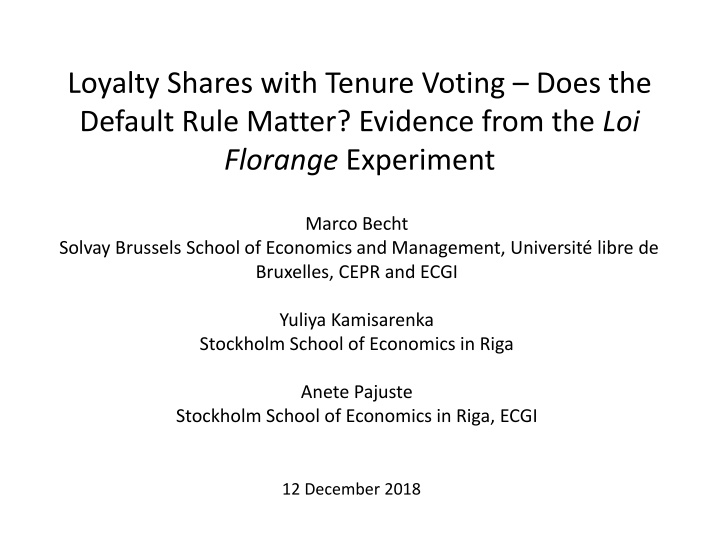

Loyalty Shares with Tenure Voting Does the Default Rule Matter? Evidence from the Loi Florange Experiment Marco Becht Solvay Brussels School of Economics and Management, Universit libre de Bruxelles, CEPR and ECGI Yuliya Kamisarenka Stockholm School of Economics in Riga Anete Pajuste Stockholm School of Economics in Riga, ECGI 12 December 2018

Loyalty Shares Loyalty shares provide long-term holders additional cash-flow and/or control rights (Bolton & Samama, 2013). L-Shares with tenure voting (LSTV) provide additional voting rights after a certain holding period (e.g. 2x or 4x after 24 or 48 months; 1/12 every month up to 120 months); Paper confined to loyalty shares with tenure voting (or time-phased voting ); control enhancing mechanism (CEM); LSTV available in Fr, NL, It (since 2014), the US, the UK; in Belgium 2019; under consideration in CH, ES 28/04/2018 Loyalty Shares with Tenure Voting 2

LSTV vs. Dual Class Single share class, potentially available to all shareholders; Extra votes not perpetual; expire upon sale; Single share price; Voting power depends on holding periods of other shareholders; Semi-manual registration in Europe; promise of automation from Long Term Stock Exchange (LTSE) project in the United States; Less transparent than dual class. 28/04/2018 Loyalty Shares with Tenure Voting 3

LSTV 2x Vote Wedge 28/04/2018 Loyalty Shares with Tenure Voting 4

Kering SA International luxury group based in Paris, France. It owns luxury goods brands, including Gucci, Yves Saint Laurent, Balenciaga, Alexander McQueen, Bottega Veneta, Boucheron and Brioni, Pomellato; controlled by Fran ois-Henri Pinault 28/04/2018 Loyalty Shares with Tenure Voting 5

LSTV 10x Vote Wedge 28/04/2018 Loyalty Shares with Tenure Voting 6

LSTV in France Long tradition of loyalty shares with tenure voting; used by more than half of French listed companies (Belot, 2005; Chene, 2008); One-share-one-vote IPO default rule; Double voting rights after two years or more; IPO with retroactive or zero tenure clock; Shareholders could change regime post-IPO via 66.66% majority vote (OSOV<->LSTV) 28/04/2018 Loyalty Shares with Tenure Voting 7

The Loi Florange Law to Reconquer the Real Economy Mainly about plant closure procedures, but also about voting rights in listed companies; On 3 April 2016 default rule changed from one-share- one-vote to loyalty shares with tenure voting (LSTV); New default rule applies for IPOs; For stock: Transition period between 29 March 2014 and 3 April 2016; inaction results in L-Share adoption; interference with property rights Safe-harbor: mandatory bid requirement suspended for extra votes in OSOV->LSTV transitions Law perturbs pre-reform corporate control equilibrium. 28/04/2018 Loyalty Shares with Tenure Voting 8

Loi Florange Timeline 28/04/2018 Loyalty Shares with Tenure Voting 9

IPO Flow Default Rules Period OSOV LSTV OSOV default phase before 3 April 2016 Default Opt-in Default & Opt-in & opt-out of Article L. 225-123 after 2 April 2016 do not opt-out of Article L. 225-123 after 2 April 2016 Transition phase 29 Mar 2014 to 2 Apr 2016 Opt-in Default LSTV default phase 3 Apr 2016 onwards (Opt-out of Article L. 225-123) (Do not opt-out of Article L. 225-123) 28/04/2018 Loyalty Shares with Tenure Voting 10

LSTV IPO in 2015 Europcar SA ARTICLE 9 DOUBLE VOTING RIGHTS A double voting right is allocated to fully paid-up ordinary shares that have been continuously owned in registered form by the same shareholder for a minimum period of at least two (2) years. [ .] The power to derogate from the allocation of double voting rights, provided by Article L. 225-123 para. 3 of the French Commercial Code, is not used. 28/04/2018 Loyalty Shares with Tenure Voting 11

OSOV IPO in 2015 Amundi SA IPO Prospectus: 21.2.3 Rights, Privileges and Restrictions on Shares (Articles 7 to 9 of the Bylaws) Each share gives the right to one vote. The double voting right provided for by Article L. 225-123 of the French Commercial Code is expressly excluded. The Bylaws do not contain any provisions restricting the voting rights attached to the shares. 28/04/2018 Loyalty Shares with Tenure Voting 12

Default Rules and Freedom of Contracting Behavioural economics: default rules matter Coase: default rule should not matter Pre-IPO controller will choose structure that is most beneficial, if transaction costs are small Argument in favour of freedom of contracting; one-share-one vote will be used when beneficial; IPO default rule should not matter Will the stock revert? (Conflicted) parties without super-majority might have a blocking minority 28/04/2018 Loyalty Shares with Tenure Voting 13

IPO Flow: LSTV vs. OSOV Time Period One share- one vote Loyalty shares Total Fraction of IPO firms with Loyalty Shares (of Total) Before 28 March 2014 26 26 52 50.0% After 28 March 2014 27 43 70 61.4% Total 53 69 122 56.6% p-value of (two-sided) Mean equality test (Before vs. After) 0.211 Population of 122 IPOs on Euronext Paris, Euronext Growth and Alternext markets March 28, 2010 - March 28, 2018. 28/04/2018 Loyalty Shares with Tenure Voting 14

IPO Characteristics (1) (2) (3) Family Stake VC Stake Proportion Sold 0.257*** -0.098 -0.030 Loyalty share dummy (2.776) (-1.304) (-0.820) -0.006 -0.023 0.046 After reform dummy (-0.078) (-0.279) (1.467) Loyalty share x After reform (Diff-in-Diff) -0.068 0.062 0.026 (-0.549) (0.620) (0.536) 0.241*** 0.283*** 0.296*** Constant (3.904) (5.344) (13.323) Yes Yes Yes Industry effects 116 116 116 Observations 0.0939 0.0448 0.0478 Adjusted R-squared 28/04/2018 Loyalty Shares with Tenure Voting 15

IPO Underpricing (4) (5) (6) 1 Day-Return 5 Day-Return 22 Day-Return Loyalty share dummy -0.030 -0.022 0.006 (-0.459) (-0.279) (0.088) After reform dummy -0.059* -0.013 0.084 (-1.840) (-0.234) (0.855) Loyalty share x After reform (Diff-in-Diff) 0.051 0.002 -0.107 (0.714) (0.026) (-0.916) Constant 0.049* 0.050* 0.015 (1.934) (1.817) (0.436) Industry effects Yes Yes Yes Observations 116 116 116 Adjusted R-squared -0.0136 -0.0236 -0.00724 28/04/2018 Loyalty Shares with Tenure Voting 16

IPO Size and Book to Market (7) (8) (9) Ln(Proceeds) Book to Market Ln(Market Cap) -0.698* Loyalty share dummy -0.833** 0.057 (-1.793) (-2.072) (1.157) 0.210 After reform dummy 0.368 0.014 (0.585) (0.968) (0.293) Loyalty share x After reform (Diff-in-Diff) 0.378 0.540 -0.027 (0.755) (1.007) (-0.401) 4.565*** Constant 3.261*** 0.328*** (15.645) (10.752) (9.832) Yes Industry effects Yes Yes 116 Observations 116 116 0.241 Adjusted R-squared 0.257 0.279 28/04/2018 Loyalty Shares with Tenure Voting 17

Pre-Reform Equity and Voting Stake of Largest Owner 28/04/2018 Loyalty Shares with Tenure Voting 18

Transition Matrix Total (after) OSOV (before) 45 (43%) L-Share (before) 59 (57%) 104 (100%) 28/04/2018 Loyalty Shares with Tenure Voting 19

Transition Matrix OSOV (after) L-Share (after) Total (after) OSOV (before) 31 45 (30%) (43%) L-Share (before) 58 59 (56%) (57%) Total (before) 104 (100%) 28/04/2018 Loyalty Shares with Tenure Voting 20

Transition Matrix OSOV (after) L-Share (after) Total (after) OSOV (before) 31 14 45 (30%) (13%) (43%) L-Share (before) 1 58 59 (1%) (56%) (57%) Total (before) 32 72 104 (100%) (31%) (69%) 28/04/2018 Loyalty Shares with Tenure Voting 21

OSOV to Post-Reform L2x switchers: Pre-Reform 28/04/2018 22 Loyalty Shares with Tenure Voting

Shareholder Resolution Orange: Motivation Double voting rights do not allow for exact proportionality between the capital invested by a shareholder and the voting rights available to him; in addition, obtaining double voting rights requires registration of shares, which involves an administrative burden that is too high or impossible to manage for a foreign investor or UCITS mutual fund, and consequently leads to an imbalance in shareholder rights. Contrary to the intent of the law, which is to promote long- term investment - a goal many shareholders have in common with us - , we have concluded that the system of double voting rights, as created by the Florange Law, does not in any way facilitate the long-term holding of shares. Resolution submitted by PhiTrust Active Investors, supported by a group of investors, jointly representing 1,0882% of the Company s capital., not approved by the Board of Directors. 28/04/2018 Loyalty Shares with Tenure Voting 23

Failed Revert to OSOV Resolutions Votes Present State (% capital 31/12/2014) Ticker Company Sponsor For Mgmt ISS Air France- KLM Alstom SA AF M 58.6 56.6 For For 18.0% ALO M 61.5 52.0 For For 20.0% ENGI Engie SA M 65.9 40.0 For For 32.8% ORA Orange SA S 67.2 43.3 Against For 23.0% RNO Renault SA M 72.5 60.5 For For 19.7% VIE M 56.2 51.2 Against For 4.6% Veolia E SA VIV Vivendi SA S 59.0 50.1 Against For (3.4%) The French State is the dominant force in 6/7 cases. 28/04/2018 Loyalty Shares with Tenure Voting 24

28/04/2018 25 Loyalty Shares with Tenure Voting - a Coasian Bargain?

28/04/2018 26 Loyalty Shares with Tenure Voting - a Coasian Bargain?

OSOV to L-Share2x by default State Ticker Company (% capital 31/12/2014) 50.5% ADP Aeroports de Paris BOL Bollor SA - CNP CNP Assurances 78.3% indirect via Airbus (10%) 84.9% AM Dassault Aviation SA EDF Electricit de France SA HAV Havas SA - The French State is the dominant force in 3/5 cases Note: Sopra Steria Group voted in June 2014 to adopt L-Shares, converting two years earlier than by default. The vote was opposed by ISS and the state was not involved. Loyalty Shares with Tenure Voting - a Coasian Bargain? 28/04/2018 27

OSOV to Post-Reform L2x switchers: Post-Reform 28/04/2018 Loyalty Shares with Tenure Voting 28

Pre-Reform Stock (SBF 120) Capital and Votes Loyalty Shares OSOV N Fraction Capital (%) Votes (%) N Fraction Capital/Votes (%) Family 28 0.47 35.7 45.8 7 0.16 50.6 Corporation 9 0.15 39.6 51.1 14 0.30 34.2 Financial 8 0.14 14.7 20.9 7 0.16 33.8 State 3 0.05 19.5 22.2 9 0.20 41.6 Dispersed 11 0.19 . . 8 0.18 . 59 1.00 31.9 41.2 45 1.00 39.1 Source: Annual reports; 104 French incorporated index constituents 28/04/2018 Loyalty Shares with Tenure Voting 29

Pre-Reform Stock (SBF 120) Capital and Votes Loyalty Shares OSOV N Frac Capital (%) Votes (%) N Frac Capital/Votes (%) Family 31 0.43 37.4 47.6 4 0.13 35.8 Corporation 8 0.11 38.2 50.3 10 0.31 38.2 Financial 9 0.13 13.9 18.0 7 0.22 25.5 State 11 0.15 35.4 42.2 2 0.06 31.1 Dispersed 13 0.18 . . 9 0.28 . 72 1.00 33.6 42.4 32 1.00 33.3 28/04/2018 Loyalty Shares with Tenure Voting 30

Post-Reform Equity and Voting Stake of Largest Owner 28/04/2018 Loyalty Shares with Tenure Voting 31

Value effect (Tobins Q) Tobin s Q unaffected by Loi Florange, even for switchers . 28/04/2018 Loyalty Shares with Tenure Voting 32

Change in Market to Book Values 2.5 2.14 2.06 2 1.65 1.62 1.5 1.46 1.41 1.11 1.11 1 0.5 0 2014 2016 LSTV-LSTV OSOV-OSOV LSTV-OSOV OSOV-LSTV 28/04/2018 Loyalty Shares with Tenure Voting 33

Tobin's Q by ownership type Tobin s Q consistently lower for state ownership, pre- and post reform. Inefficiency or stakeholder orientation? 28/04/2018 Loyalty Shares with Tenure Voting 34

Average holding period by the decision group The average holding periods of loyalty share firms and OSOV firms are not significantly different both before and after the Act 28/04/2018 Loyalty Shares with Tenure Voting 35

OSOV-L2x switchers become less loyal 28/04/2018 Loyalty Shares with Tenure Voting 36

Summary LSTV in Europe: CEM used by families IPO flow LSTV IPOs: high family ownership LSTV proportion in IPO flow: hardly affected by change in default rule IPO valuation; no difference LSTV-OSOV cross-section, before and after Stock Valuation of OSOV and LSTV (Q) high before reform Reversal to OSOV in absence of the French state (and Bollor group); Valuation of state controlled companies lower pre- and post reform; 28/04/2018 Loyalty Shares with Tenure Voting 37

Reference Becht, Marco and Kamisarenka, Yuliya and Pajuste, Anete, Loyalty Shares with Tenure Voting - a Coasian Bargain? Evidence from the Loi Florange Experiment (April 2018). European Corporate Governance Institute (ECGI) - Law Working Paper No. 398/2018. Available at SSRN: https://ssrn.com/abstract=3166494 28/04/2018 Loyalty Shares with Tenure Voting 38

")

")

")