Inventory Management and Control in Business

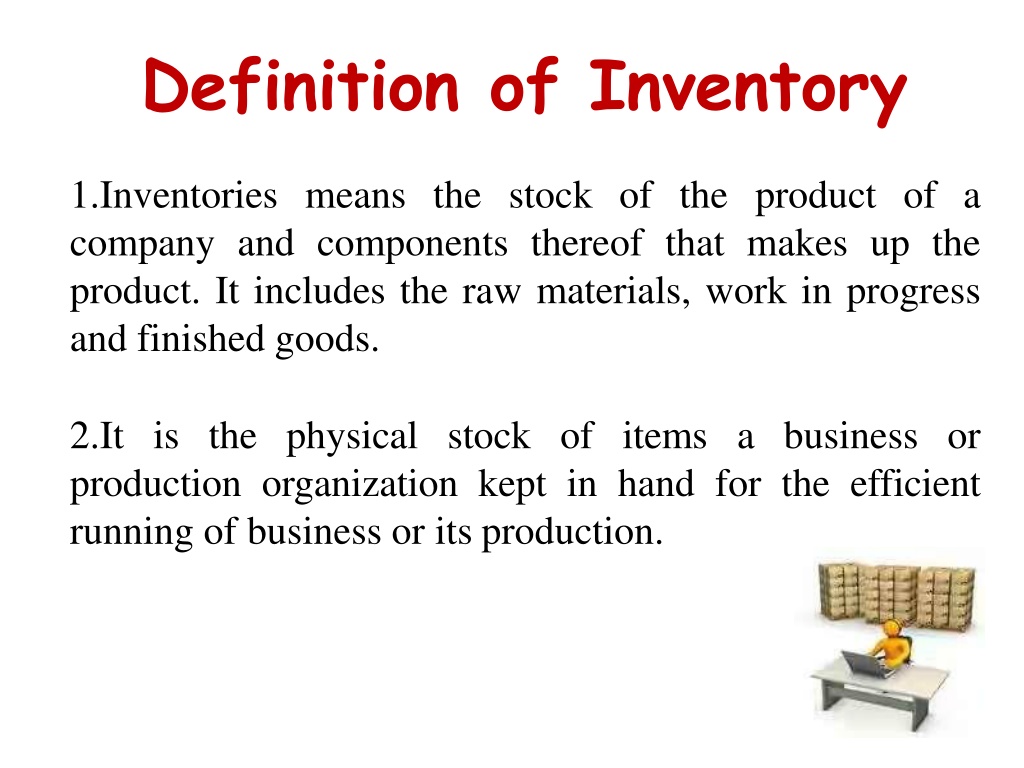

Definition of

Inventory

1.

Inventories means

the stock of the

product

of

a

company and components thereof that makes

up the

product. It includes the raw materials, work in progress

and

finished

goods.

2.

It is

the

physical stock

of

items

a

business or

production

organization

kept in hand for

the

efficient

running of business or

its

production.

Inventories

are

:-

1.

Items in

stock.

2.

Usable but

idle

resources.

Inventory

control

P

r

o

c

e

ss

o

f

m

aintai

n

i

ng

opti

m

u

m

nee

d

ed

qu

an

t

ity

of

inventories

for the

smooth operation

of

organization.

Classification of

inventories

Inventory

Indirect

i

n

v

e

n

t

o

r

y

In

process

inventory

Raw

material

inventory

Objectives

of

inventory

control

The basic managerial objectives are 2

fold:-

1.

Avoid

over/under investment in

inventories.

2.

To

provide right

quantity and quality goods

at

right

time

at

proper value.

Objecti

v

es

of

inventory

control

Operating

objecti

v

es

Financial

objecti

v

es

Operating

objectives

1.

Availability

of

Materials

: All type

of

material available

at

all

time

so that production

may

not be

held

up for

want

of

supply

of

materials.

2.

Minimizing the wastage

: permit only uncontrollable

wastage.

Avoid

wastage

by

leakage theft,

embezzlement,

spoilage( rust, dust

,

dirt)

3

.

P

r

o

m

o

t

i

o

n

o

f

m

a

n

u

facturing

e

f

fici

e

nc

y

:

Wh

e

n

ri

g

ht

type

of raw material is available

at

the

right

time.

4.

Better service to

the

customers

: Maintain proper

production

flow

to produce

sufficient

finished goods

to

meet

the

demand

of of the

customers

5.

Control

of

production

level

:

To

increase

or

decrease

the

production

as

per

the

demand as well

as

to maintain proper

buffer

stock

to

meet

any eventuality in

difficult

times.

6.

Optimal level

of

inventories

: It is done in view

as

per

the

operational requirements.it

also

avoids the

out of stock

danger.

Financial

objectives

1.

Economy in purchasing:

management

makes every

attempt to purchase the raw materials in

bulk

quantity

and to take advantage

of

favorable market

condition.

2.

Optimum investment and

efficient

use

of

capital:

The

finance management should set

up

maximum and

minimum levels

of

stocks

to avoid deficiency

or

surplus

of

stock

position.

3.

Reasonable price

: Management should ensure supply

of

raw materials

at

a reasonable low price without

sacrificing

the

quality

of

it thereby helping the cost

of

production

and

quality

of

finished

goods.

Advantages

of

inventory

1.

Delivery in

time:

as inventory stored

aids

smooth production,

the

manufacturing company

can

earn reputation

as a

reliable

supply.

-

our finished goods can be raw

materials

for

buyers.

-

reputation

can get

more

customers

2.

Possibility of discount on bulk

purchase

3.

Efficiently

handle unforeseen circumstances

: harthal, bandh

or

other transportation

difficulties

do not hinder

production.

4.

No

idling of

workers

and

machineries

.

Disadvantages of

inventory

1.

W

ork

i

ng

c

a

p

i

tal

t

i

ed

up

:

c

ant

u

t

i

li

z

e

t

h

e

a

m

ount

for

o

t

her

purposes

nor

it yield any

interest.

2.

More space

required

: more inventories more

is

the

space

needed

and space accounts for

rent.

3.

Increase

i

n

sur

an

c

e

c

h

a

r

ge

s

:

Incr

e

ased

cost

of

handl

i

ng

and

manufacturing.

4.

Increased

o

ver

he

a

d

e

xpenses

:

S

e

curity

p

e

rs

o

nnel

requ

i

red

to

guard

inventory.

5.

Chances of

damage

:

Pilferage,

replacement,

etc

more.

6.

Increased chance

of

obsolesce

.

•

Inventories constitute a significant part

of the

working

capital.

•

I

n

ventory

con

t

rol

purchase

and

p

ro

du

c

t

i

o

n

u

n

i

t)

and

val

u

e

u

s

ed

i

n

u

n

i

t/physical

c

o

n

t

r

o

l(

c

o

n

trol

(Accounts

unit)

•

When

a

fi

r

m

f

e

e

l

s

h

o

r

tage

o

f

fi

n

ance

it

s

h

ould

t

ake

more

care

in its inventories rather than anything

else.

Ordering

cost or procurement

cost or purchasing

cost

•

The cost that

has

to be spent in

making

purchase

order.

•

Includes all the expenditure

associated

on placing an

order.

-

postal service

expense

-

expenditure on stationary and

consumables.

-

travelling

expense.

-

ti

m

e

spent

by

purc

h

ase

depar

t

m

ent

for

o

rd

e

r

and

its

equivalence in

terms

of

money.

-

expenses on

supplies.

-

rent for

premises

occupied by purchase

department

-

legal fee for lawyers in case such situations

arises.

Inventory

carrying

cost

Cost

of

blocking material

as

inventory

. This

includes:-

1.

Cost

of

interest

for the

value

of

items

stored

as

inventory.

2.

Salaries

o

f

per

s

onnel

m

anaging

v

a

ri

o

us

position

including security

personnel.

3.

Rent

for the

space occupied

by the

inventories.

4.

The potential scope

of

loss , pilferage, obsolescence,

etc.

5.

Cost

involved

in

the

insurance

of

inventories.

6.

Stationeries

and consumables used by the

store

people.

Under

stocking

or

shortages.

It is the

cost

of not having

an

item when it is

needed, thus

affecting

the

sales

of the

company.

This

may

lead to 2

situations:-

1.

Back

logging

2.

Cancellation

of orders.

Backlogging

:

work is

delayed beyond

its

schedule

and

eats

away

the schedule

time

of next order thereby delaying the next

order.

Cancellation

of

order

:

When

buyer is

not

in a position to wait

.

Both the above results

in:

1.

Penality cost

:

Purchase order

will have

an in

built provision

for

penality

eg, 20% payment

reduced

for

2 days

delay,

etc

2.

Emergency

replenishment:

In an

urgent

situation

if you

want

good

quality we

may

have to

spent extra amount

eg.

Emergency

transportation

cost,etc.

3.

loss

of good

will

Over stocking

cost

This results when stock is left on hand when the demand

for the

item has

ended.

The left over

inventory

may

be

-

Utilized

at

a later

stage.

-

Thrown

out

as

scrap.

1.

ABC

analysis

2.

VED

analysis

3.

SDE

analysis

4.

FSN

analysis

5.

HML

analysis

ABC

analysis

•

Process

of

classifying items

using

values

as

measure.

•

Process of excursing selective

control over

inventories.

Objectives

of the

analysis

1.

Frame

policy guidelines

regarding

control

of

items.

2.

This policy enables material managers to exercise

selective control when

he

is confronted with

large

number of

items.

3.

Expensive items are branded

as

A items(10%)

the

in

between

as

B(20%) and least

expensive

as

C(70%)

The

method.

1.

All

the

item that are used in

the industry

are

identified.

2.

Items are listed as per

the

value.

3.

The number of

high

valued

items

, medium valued and

low valued items are

counted.

4.

Their percentage is

found out.

The

concept

It is practically not feasible to exercise tight control

over

all items

in

a

large

or in medium sized

organization.

Hence

we

resort to classify

the

items

according to their

importance.

VED

analysis

•

Based

on

the critical values

and

shortage cost

of the

item.

Thus helps focus

on

vital

items.

•

Based

on

criticality

the

item

can

be

classified into 3

categories viz;

Vital,

Essential and

Desirable.

•

Vital

items are critically

needed

in a manufacturing unit.

The items with lower criticality included in E and lowest

in D.

•

The status

of

each

item will

be

discussed with

justification

by the

material manager in consultation with

other

departments of the manufacturing

unit.

SDE

analysis

Classification based on lead time/

availability

•

S(

Scarce)

those

item

which are imported

or

which need

a lead

time

more than 6

months.

•

D(Difficult): The

items

which require

less

than 6 months

but

more than a fort

night.

•

E

(

e

a

si

l

y

availa

b

le

)

:

It

e

m

s

which

are

a

v

ailable

e

a

sily

in

less than a fort

night.

•

Helps

bring down

lead time and out of

stock

cost.

FSN

analysis

Classification based

on

frequency

of

issue

or

use.

•

F

=

Fast

m

o

v

i

n

g

it

em

s

t

h

at

a

r

e

f

r

equen

t

ly

i

s

s

ued

in

a

manufacturing

unit.

•

S =

Slow

moving items in a manufacturing

unit.

•

N = Non moving

item

This classification helps

in

establishing most suitable

layout

by

locating all fast moving items near

the

dispensing

window to reduce

the

handling

efforts.

HML

analysis

Classification based on

unit

value.

H = high cost

M=

medium

cost

L= Low

cost

This type

of

analysis helps in exercising control

at

the

use

point

.

Proper

authorization should be there for replacing

a high value

item

Definition

of

EOQ

It

is

t

h

e

p

a

rt

i

cular

quantity

a

t

wh

i

ch

t

h

e

s

u

m

o

f

c

o

st

of

both

the ordering

and

inventory

carrying cost is

minimum.

Total

cost

= carrying cost + procurement cost

Consumption

rate

It is

the

rate

at

which

the

raw materials are

consumed.

If

we

plot a graph

between

time and level

of

inventory

the

slope of the

graph gives

the

consumption

rate

Constant consumption

rate.

If

the

raw material is consumed at same rate over

the

same

period

of

time.

Actual / irregular

consumption

rate

There will

be

variation in

the

production which leads to

different

consumption rates

at different time

intervals.

Also influenced

by

factors like power

failure.

Replenishment.

The process of

refilling

the material

as

and when it is

consumed so

that

the

inventory level

is

maintained within a

range

.

Types:-

1.

Instantaneous

replenishment

2.

Replenishment at constant

rate

3.

Replenishment at irregular

rate.

1.

Instantaneous replenishment

: refilling

is

done

at

one

time,

at

one

instant

for the one

full

lot

size.

2.

Replenishment

at

constant rate

: If

we

replenish the

used inventory

at

a constant rate . Usually practiced

in

industries especially

the

ones which manufacture its

own raw

material.

3.

Replacement

at

irregular interval:

The inventory is not

refilled

at

regular interval

of

time.

Lead

time

Lead

time

is the time gap

between

starting

or

initiating

the

process

of

ordering

and

receiving the ordered

quantity

in

stores.

This is estimated

by the

past experience.

Lead

time

includes

the

following:-

1.

Time

taken to prepare purchase requisition and placing

the

order.

2.

Time

taken to

deliver

purchase

order

to

vendor.

3.

Time

taken

for the

vendor to

manufacture.

4.

T

i

m

e

tak

e

n

f

o

r

transp

o

rt

a

tion

f

r

om

ven

d

o

r

s

pl

a

ce

to

the

stores.

Reorder

point

This is

the point

which indicate that it is

high

time

we place

the

order

failing which the

stokes

may

get

exhausted.

Reorder

point

=

lead time

– predicted

point

of

exhaustion.

Eg.

If

we order once in every

10

days and

the

lead

time

is 3

days then

ROP

= 10 – 3 = 7

days.

Lead

time

analysis.

Lead

time depends on

:-

1.

T

h

e

u

r

gency

o

r

i

m

p

o

r

tance

o

f

t

h

e

comp

o

nents

in

t

h

e

manufacturing

process.

2.

Reliability

of the

vendors.

Reserve stock(O-RS)/

Safety

stock/Buffer

stock

•

To

guard against disturbances

of

production process

either

due

to uncertainties in consumption rates

or

lead

time some extra

stock

is

maintained.

•

It serve the purpose

of

minimizing the

chances

of

running

out of

stock.

•

It should

not be

very less

or

excess.

Safety

stock

come

to play when there is

:-

1

.

A

n

e

x

c

e

ss

reje

c

ti

o

n

o

r

wastage

in

process than

normal.

production

2. Rejection

at

the time of receipt due

to

-Poor

production quality

by

vendor.

-

Damage

to raw

material.

Factor of

uncertainty

Uncertainty is

the

main

reason

for

having safety

stock.

It

may

be due

to:-

1.

Uncertainty of demand

2.

Uncertainty

of

delivery.

3.

Uncertainty

of

quantity.

•

Uncertainty

of

demand:

there will

be

a

difference

between

the

expected demand and

the

actual

demand

which is known

as

the

forecast

error.

It is mainly

dependent on the

buyers

side.

•

Uncertainty

of

delivery:

depends

on

how long the

lead

time

is going to be. If something goes wrong with

the

suppliers production

the lead time

may

prolong.

•

Uncertainty

of quantity:

this

depends on how

many

scrap or imperfect items the

ordered

quantity

is

going

to

contain.

Determination

of

safety

stock

The

level

of

safety

stock

to

be

maintained

depends

on

various factors

like:-

-Cost of item in

question

-Uncertainties in

demand

-Negative fall

out of stock of

this

item

-Spoilage

due

to

long

storage ,

etc

Optimum safety stock = maximum lead

time

in

amount-

normal lead

time

in

amount.

Max.

lead

occurred.

ti

m

e

=

t

h

e

wor

s

t

possible

scenario

Foun

d

ou

t

in

co

n

sul

t

a

tion

with

t

h

e

purchase department or past

records.

Normal lead

time

= most expected lead

time

or the

average lead

time.

e.g.. If

the

maximum

lead

time

is

13

days and the

average lead

time

is

11.5

days then

13-11.5=

1.5, a

stock

that last

for

1.5 days is

the

optimum safety

stock.

Disposal of obsolete and

surplus

material

.

Obsolete material:

Those materials

or

equipments which

are

not

damaged

and

which have economic work

but

are

no

longer useful

for the

company’s

operation

due

to

change in

production

line.

The

term

can

be

associated with equipments, materials,

stocks, techniques,

etc.

It is very

difficult

to predict when

the

technology will

change leading to obsolescence. The company should

have sharp eye on the competition so that it

can

have

more

Causes

for

Obsolescence

1.

Adoption of

standardization

:

lead to

elimination

of non standard

varieties.

2.

Adoption of

new

technology.

3.

Changes in production

design

4.

Cannibalization

:

when a

machine breaks

down, it

is, sometimes

rectified

by using

components

of an

identical machine

which

is

already not

functional.

5.

Faulty purchases

:

it the purchases

are

made

in bulk

so

that

they

can last for a very long

time.

Can be controlled by

FSN

analysis

Surplus

material

Equipments which have

no

immediate use

but

had

accumulated

due

to faulty planning , forecasting and

purchasing.

They have usage value in

future.

•

They are merely excess

of

what is in

need.

•

Easy to control compared to

obsolete.

•

Both

s

u

rplus

and

o

b

solete

m

aterials

condition.

are

in

good

Common causes

for

surplus

and

obsolete

materials

1.

Over

ordering

2.

Faulty

planning,

purchasing and

forecasting.

3.

Reduced

production.

4.

Drastic reduction in

wastage.

5.

Modification of

processes.

6.

Faults in

store

keeping

and

record

keeping.

They

need to be disposed

?

1.

Keeping them is a costly

affair.

2.

They need space.

3.

More

security

personnel

4.

Separate

store for

maintaining

them.

5.

More chances

of

pilferage, damage

etc.

Stages

of

disposal

of

obsolete and

surplus.

1.

Finding:

Periodic study must

be

carried

out of

all

items stocked

or

staying

as

inventory.

2.

R

e

cri

m

i

n

a

t

io

n

:

Alternati

v

e

ways

o

f

using

t

h

e

se

items must

be

explored within

the

industry.

3.

If they cannot be used any where then disposal

act

is carried

out.

Priorities

in the

process

of

disposal.

1.

Explore

possibility of sending in

bulk.

2.

Dispose to

original

supplier if they show

interest.

3.

P

r

eference

m

ay

b

e

g

i

ven

to

b

u

yers

o

r

ven

d

o

r

s

who

have long term relation with

the

company.

4.

Then

t

h

ink

o

f

others

who

m

ay

bu

y

a

t

best

poss

i

b

l

e

price.

5.

If it cannot

be pushed

off

at

best

possible price, sell

at

scrap

value.

6.

If

it

is

not

p

o

ssible

d

i

s

p

ose

t

hem

o

f

f

f

ree

o

f

co

s

t

to

someone who

can

use

them.

( sometimes when distribute to employers it

may

lead to

a

negative

si

d

e

e

f

fe

c

t

–

ethic

a

l

iss

u

e,

p

u

r

p

os

e

f

u

l

Process

of

disposal

of

obsolete

and surplus

material.

•

B

y

nego

t

i

ation

by

which

b

u

y

e

rs

appr

o

a

c

hes

for

the

purchase

of

such

materials.

•

Auction.

•

Tenders.

Material

handling

Moving physical objects from

one

place

to another

as

parts, components, sub –assemblies,

raw

materials,

or

finished goods

ready

for

shipment.

Defined

as

the function dealing with

the

preparation,

placing and positioning

of

materials to facilitate their

movement

or

storage.

The moving of materials from

raw

material store to

through production to ultimate consumer with least

expenditure

of

time,

effort

so as to produce maximum

productive

efficiency

and lowest handling cost

Salient

principles of material

handling

1.

Principles related to

planning.

-

Planning

principle:

All

handling activities

must

be

properly

planned.

Eg,

use

of

same container throughout

a

handling

process.

-

System

principle:

Plan

a

system

integrating

as

many

handling

activities as

is

practical

and coordinate full scope of

operation.

-

Material flow principle

:

Plan an

operation sequence and

equipment arrangement optimizing material

flow.

e.g plan

related work areas

together.

-

Simplification principle:

Reduce

or

eliminate

unnecessary

movements.

-

Gravity

principle:

wherever practicable

utilize

gravity

to

move

material

-Space

utilization principle

:

Avoid

keeping

too

much

of

inventory at

temporary

store.

-Unit size

principle:

Increase

the

size

, weight,

quantity

of

the

load handled at a

time.

-Safety

principle:

provide

safe

handling method. Highlight

handling hazards or danger zones in a

manufacturing

unit.

-Equipment selection principle:

consider all the aspects

of of the

material

to be handled and the

method

to be

utilized

in

terms

of

the

lowest

overall cost.

Eg.

Select versatile

equipments.

-Standardization principle.

Standardize methods, as well as type

and size of handling

equipment.

-Motion

principle:

fix

minimum

period

for loading,

unloading

and

other

idleness.

-Idle

time

principle

: reduce

the

unproductive

time

of both

handling

of equipment

anf

manpower

-Maintenance principle:

Set up regular

maintanance

schedule

-Obsolescence principle:

Identify and replace obsolete

matrrials.

-Fle

x

ibi

l

ity

pr

i

n

cip

l

e

:

p

urc

ha

s

e

eq

u

ip

m

ents

that

c

an

p

e

rform

a

variety of

tasks.

Lig

h

t

wei

g

ht

prin

c

i

p

l

e

:

o

p

t

for

e

quip

m

ent

t

h

at

h

ave

less

dead

weight.

Principles related to

operations.

-

Control principle:

use martial handling principles

to

improve production and inventory control. Materials

may

be

moved

as

per

schedule.

-Capacity principle:

Production capacity should

be

fully

achieved.

-

Performance

efficiency

principle

: Determine

efficiency

of

handling performance in terms of expense per

unit

handled.

Kindly

refer

material

handling

and

modern

material

Store

keeping

Store

keeping: custody

of

all materials stocked in stores

for

which

store

keeper is

the

trustee.

St

o

res

ma

n

age

m

ent

res

p

o

n

sible

f

o

r

p

r

o

per

recei

p

t

,

custody and issue

of

materials.

Function of stores

department

1.

To

receive

materials

and check them

for

identification

2.

To

correctly

position all

materials

and supplies within

the

stores

3.

Maintain

stock safely

in good

condition.

4.

Is

s

u

e

m

a

t

er

i

al

on

l

y

on

r

e

q

u

is

i

tion

b

y

auth

o

r

i

z

ed

person.

5.

Maintain

up

to

date

record

6.

Ma

k

e

s

u

r

e

the

s

t

o

r

e

i

s

clean

a

n

d

i

n

g

oo

d

w

orking

condition.

7.

Optimum

utilization

of

store

space

8.

Initiate

process

of

purchasing

at

the

right

time.

9.

Coo

r

din

a

t

e

and

c

o

o

pe

r

a

t

e

wi

t

h

v

arious

departme

n

t

s

like

purchase,

production,

etc.

Location

of

store

- Minimize total handling costs and other costs related

store

operation.

-Location should

be

according

to

the

nature and value

of

materials to

be

stored.

-Raw materials are

stored

need to

the

first

operation.

-In process material close to

the

next

operation.

-Finished goods

near

the shipping

area

-All departments should have

easy

assess.

List of available store

space

1.

Platform

2.

Floor

space

3.

Rack

4.

Shelves

5.

Bins

6.

Trays

7.

Drums

8.

Barrels

they

can

be stored

as

a unit, a

tier,

a row

or

a

section

Stock

verification

1.

Annual physical

verification:

-

Verification

officer

individually

or

in team verifies

stocks

in

the

stores once

in

a year checking all

relevant documents

like

bin cards,

stores

ledger,

etc.

-

After verification a list consisting

of

shortages,

damages,

surplus

is given to

the

management.

-

During verification

the stores

wont

be

functioning.

2.

Perpetual

inventory

control

-Continuous check through

out the

year

in

such a way

that

each

item is checked

at

least

once

in a

year.

-‘A method

of recording

stores balances after every

receipt and issue to facilitate regular checking

and

to

obviate closing down

for

stock

taking”

-Priority

given to A items then B and least to

C.

-Incidentally help continuous

stock

taking.

Errors

in

stores

1.

Clerical

mistakes.

2.

Improper

storage e.g,

camphor

–

volatile.

3.

Pilferage

( steal items that are not that

valuable)

4.

Leakage.

5.

Careless

handling

6.

Handling

loss.

Store

layout

1.

Section

adjacent

to

store

should be

kept reserved

for

receipt

of

materials

and

for

its inspection

before

storage.

2.

Minimize

handling and transportation of

materials.

3.

Optimum utilization of floor

space and

height.

4.

Shelves,

racks

etc should be

situated

in

clearly

defined

leaves

so

that he

items

are

quickly stored

and

located

for

physical

counting and

issuing.

5.

Min lines

should be between

1.5 to 3 m wide

depending

on

the

type of

material

and

amount

of

traffic

involved.

6.

Storage space should

be

clearly marked to ensure

easy

and

quick

identification.

7.

Storage

space should

be

protected against waste

damages, pilferage,

etc.

8.

Place

for storing

material based

on

material

characteristics.

9.

Lay

out

should

be

such hat it

can

make use

of

modern

material handling equipments like fork lifts, trucks,

conveyors,

etc

10.

Store

keeper is

not

compelled to

put

newly arrived

material on the top of the

old.

11.

20

to

25% due

space in

each

portion

of the store for

further

expansion.

Records

Store

r

e

c

o

r

d

s

.

Store

ledger

BIN

card

Bin

card

•

The

d

o

cu

m

ent

t

h

at

recor

d

s

t

h

e

exa

c

t

qu

anti

t

y

of

material available in the

store

at

a

give

time.

•

For

each

material a separate

bin

card

is

maintained.

•

prepared by

store

keeper.

•

Record

of

quantity only

•

Entry

made

immediately after

each

transaction

•

Kept

inside

store.

Stores

ledger/

perpetual

inventory

cards

•

Identical

to

bin

card

but

here the money value is

also

shown.

•

Entries are

made

periodically.

•

Prepared

by

Accounts

department

•

Outside

store.

Advantages

of

record.

1.

Efficiency

of

economy.

2.

Settlements

of

disputes with credits, debits, insurance

etc.

3.

Check against under

stocking/

over

stocking.

Inventory refers to the stock of products, raw materials, and goods in various stages of production within a company. Effective inventory management is crucial for ensuring smooth operations, optimizing resources, and meeting customer demands. It involves categorizing inventories, setting objectives for control, and achieving operational and financial goals. Operating objectives focus on material availability, waste reduction, manufacturing efficiency, customer service, production control, and optimal inventory levels. Financial objectives aim at achieving economies in purchasing and maintaining healthy financial practices.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

You are allowed to download the files provided on this website for personal or commercial use, subject to the condition that they are used lawfully. All files are the property of their respective owners.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.

E N D

Presentation Transcript

Definition of Inventory 1.Inventories means the stock of the product of a company and components thereof that makes up the product. It includes the raw materials, work in progress and finished goods. 2.It is the physical stock of items a business or production organization kept in hand for the efficient running of business or its production.

Inventories are :- 1. Items in stock. 2. Usable but idle resources. Inventory control Process of maintaining optimum needed quantity of inventories for the smooth operation of organization.

Classification of inventories Rawmaterial inventory Inprocess inventory Inventory Indirect inventory

Objectives of inventory control The basic managerial objectives are 2 fold:- 1. Avoid over/under investment in inventories. 2. To provide right quantity and quality goods at right time at proper value.

Operating objectives Objectives of inventory control Financial objectives

Operating objectives 1. Availability of Materials: All type of material available at all time so that production may not be held up for want of supply of materials. 2. Minimizing the wastage : permit only uncontrollable wastage. Avoid wastage embezzlement, spoilage( rust, dust , dirt) by leakage theft,

3. Promotion of manufacturing efficiency: When right type of raw material is available at the right time. 4. Better service to the customers: Maintain proper production flow to produce sufficient finished goods to meet the demand of of the customers

5. Control of production level: To increase or decrease the production as per the demand as well as to maintain proper buffer stock to meet any eventuality in difficult times. 6. Optimal level of inventories: It is done in view as per the operational requirements.it also avoids the out of stock danger.

Financial objectives 1. Economy in purchasing: management makes every attempt to purchase the raw materials in bulk quantity and to take advantage of favorable market condition. 2. Optimum investment and efficient use of capital: The finance management should set up maximum and minimum levels of stocks to avoid deficiency or surplus of stock position.

3. Reasonable price: Management should ensure supply of raw materials at a reasonable low price without sacrificing the quality of it thereby helping the cost of production and quality of finished goods.

Advantages of inventory 1. Delivery in time: as inventory stored aids smooth production, the manufacturing company can earn reputation as a reliable supply. - our finished goods can be raw materials for buyers. - reputation can get more customers 2. Possibility of discount on bulk purchase 3. Efficiently handle unforeseen circumstances: harthal, bandh or other transportation difficulties do not hinderproduction. 4. No idling of workers and machineries.

Disadvantages of inventory 1. Working capital tied up: cant utilize the amount for other purposes nor it yield any interest. 2. More space required: more inventories more is the space needed and space accounts for rent. 3. Increase insurance charges: Increased cost of handling and manufacturing. 4. Increased over head expenses: Security personnel required to guard inventory. 5. Chances of damage: Pilferage, replacement, etc more. 6. Increased chance of obsolesce.

Inventories constitute a significant part of the working capital. Inventory purchase and production unit) and value (Accounts unit) control used in unit/physical control( control When a firm feel shortage of finance it should take more care in its inventories rather than anything else.

Ordering cost or procurement cost or purchasing cost The cost that has to be spent in making purchase order. Includes all the expenditure associated on placing an order. - postal service expense - expenditure on stationary and consumables. - travelling expense. -time spent by purchase department for order and its equivalence in terms of money. - expenses on supplies. - rent for premises occupied by purchase department - legal fee for lawyers in case such situationsarises.

Inventory carrying cost Cost of blocking material as inventory . This includes:- 1. Cost of interest for the value of items stored as inventory. 2. Salaries of personnel managing including security personnel. 3. Rent for the space occupied by the inventories. 4. The potential scope of loss , pilferage, obsolescence, etc. 5. Cost involved in the insurance of inventories. 6. Stationeries and consumables used by the store people. various position

Under stocking or shortages. It is the cost of not having an item when it is needed, thus affecting the sales of the company. This may lead to 2 situations:- 1. Back logging 2. Cancellation of orders.

Backlogging: work is delayed beyond its schedule and eats away the schedule time of next order thereby delaying the nextorder. Cancellation of order: When buyer is not in a position to wait. Both the above results in: 1. Penality cost: Purchase order will have an in built provision for penality eg, 20% payment reduced for 2 days delay, etc 2. Emergency replenishment: In an urgent situation if you want good quality we may have to spent extra amount eg. Emergency transportation cost,etc. 3. loss of good will

Over stocking cost This results when stock is left on hand when the demand for the item has ended. The left over inventory may be - Utilized at a later stage. - Thrown out as scrap.

1. ABC analysis 2. VED analysis 3. SDE analysis 4. FSN analysis 5. HMLanalysis

ABC analysis Process of classifying items using values as measure. Process of excursing selective control over inventories. Objectives of the analysis 1. Frame policy guidelines regarding control of items. 2. This policy enables material managers to exercise selective control when he is confronted with large number of items. 3. Expensive items are branded as A items(10%) the in between as B(20%) and least expensive as C(70%)

The method. 1. All the item that are used in the industry are identified. 2. Items are listed as per the value. 3. The number of high valued items , medium valued and low valued items are counted. 4. Their percentage is found out. The concept It is practically not feasible to exercise tight control over all items in a large or in medium sized organization. Hence we resort to classify the items according to their importance.

VED analysis Based on the critical values and shortage cost of the item. Thus helps focus on vital items. Based on criticality the item can be classified into 3 categories viz; Vital, Essential and Desirable. Vital items are critically needed in a manufacturing unit. The items with lower criticality included in E and lowest in D. The status of each justification by the material manager in consultation with other departments of the manufacturing unit. item will be discussed with

SDE analysis Classification based on lead time/ availability S( Scarce) those item which are imported or which need a lead time more than 6 months. D(Difficult): The items which require less than 6 months but more than a fort night. E( easily available): Items which are available easily in less than a fort night. Helps bring down lead time and out of stock cost.

FSN analysis Classification based on frequency of issue or use. F = Fast moving items that are frequently issued in a manufacturing unit. S = Slow moving items in a manufacturing unit. N = Non moving item This classification helps in establishing most suitable layout by locating all fast moving items near the dispensing window to reduce the handling efforts.

HML analysis Classification based on unit value. H = high cost M= medium cost L= Low cost This type of analysis helps in exercising control at the use point . Proper authorization should be there for replacing a high value item

Definition of EOQ It is the particular quantity at which the sum of cost of both the ordering and inventory carrying cost is minimum. Total cost = carrying cost + procurement cost

Consumption rate It is the rate at which the raw materials are consumed. If we plot a graph between time and level of inventory the slope of the graph gives the consumption rate Constant consumption rate. If the raw material is consumed at same rate over the same period of time. Actual / irregular consumption rate There will be variation in the production which leads to different consumption rates at different time intervals. Also influenced by factors like power failure.

Replenishment. The process of refilling the material as and when it is consumed so that the inventory level is maintained within a range . Types:- 1. Instantaneous replenishment 2. Replenishment at constant rate 3. Replenishment at irregular rate.

1. Instantaneous replenishment: refilling is done at one time, at one instant for the one full lot size. 2. Replenishment at constant rate: If we replenish the used inventory at a constant rate . Usually practiced in industries especially the ones which manufacture its own raw material. 3. Replacement at irregular interval: The inventory is not refilled at regular interval of time.

Lead time Lead time is the time gap between starting or initiating the process of ordering and receiving the ordered quantity in stores. This is estimated by the past experience. Lead time includes the following:- 1. Time taken to prepare purchase requisition and placing the order. 2. Time taken to deliver purchase order to vendor. 3. Time taken for the vendor to manufacture. 4. Time taken for transportation from vendors place to the stores.

Reorder point This is the point which indicate that it is high time we place the order failing which the stokes may get exhausted. Reorder point = lead time predicted point of exhaustion. Eg. If we order once in every 10 days and the lead time is 3 days then ROP = 10 3 = 7 days.

Lead time analysis. Lead time depends on :- 1. The urgency or importance of the components in the manufacturing process. 2. Reliability of the vendors.

Reserve stock(O-RS)/ Safety stock/Buffer stock To guard against disturbances of production process either due to uncertainties in consumption rates or lead time some extra stock is maintained. It serve the purpose of minimizing the chances of running out of stock. It should not be very less or excess.

Safety stock come to play when there is :- production 1. An excess rejection or wastage in process than normal. 2. Rejection at the time of receipt due to -Poor production quality by vendor. - Damage to raw material.

Factor of uncertainty Uncertainty is the main reason for having safety stock. It may be due to:- 1. Uncertainty of demand 2. Uncertainty of delivery. 3. Uncertainty of quantity.

Uncertainty of demand: there will be a difference between the expected demand and the actual demand which is known as the forecast error. It is mainly dependent on the buyers side. Uncertainty of delivery: depends on how long the lead time is going to be. If something goes wrong with the suppliers production the lead time may prolong. Uncertainty of quantity: this depends on how many scrap or imperfect items the ordered quantity is going to contain.

Determination of safety stock The level of safety stock to be maintained depends on various factors like:- -Cost of item in question -Uncertainties in demand -Negative fall out of stock of this item -Spoilage due to long storage , etc Optimum safety stock = maximum lead time in amount- normal lead time in amount.

Max. lead occurred. purchase department or past records. time = the worst possible scenario Found out in consultation with the Normal lead time = most expected lead time or the average lead time. e.g.. If the maximum lead time is 13 days and the average lead time is 11.5 days then 13-11.5= 1.5, a stock that last for 1.5 days is the optimum safety stock.

Disposal of obsolete and surplus material. Obsolete material: Those materials or equipments which are not damaged and which have economic work but are no longer useful for the company s operation due to change in production line. The term can be associated with equipments, materials, stocks, techniques, etc. It is very difficult to predict when the technology will change leading to obsolescence. The company should have sharp eye on the competition so that it can have more

Causes for Obsolescence 1. Adoption of standardization: lead to elimination of non standard varieties. 2. Adoption of new technology. 3. Changes in production design 4. Cannibalization: when a machine breaks down, it is, sometimes rectified by using components of an identical machine which is already not functional. 5. Faulty purchases : it the purchases are made in bulk so that they can last for a very long time. Can be controlled by FSN analysis

Surplus material Equipments which have no immediate use but had accumulated due to faulty planning , forecasting and purchasing. They have usage value in future. They are merely excess of what is in need. Easy to control compared to obsolete. are in good Both surplus and obsolete materials condition.

Common causes for surplus and obsolete materials 1. Over ordering 2. Faulty planning, purchasing and forecasting. 3. Reduced production. 4. Drastic reduction in wastage. 5. Modification of processes. 6. Faults in store keeping and record keeping.

They need to be disposed ? 1. Keeping them is a costly affair. 2. They need space. 3. More security personnel 4. Separate store for maintaining them. 5. More chances of pilferage, damage etc.

Stages of disposal of obsolete and surplus. 1. Finding: Periodic study must be carried out of all items stocked or staying as inventory. 2. Recrimination: Alternative ways of using these items must be explored within the industry. 3. If they cannot be used any where then disposal act is carried out.

Priorities in the process of disposal. 1. Explore possibility of sending in bulk. 2. Dispose to original supplier if they show interest. 3. Preference may be given to buyers or vendors who have long term relation with the company. 4. Then think of others who may buy at best possible price. 5. If it cannot be pushed off at best possible price, sell at scrap value. 6. If it is not possible dispose them off free of cost to someone who can use them. ( sometimes when distribute to employers it may lead to a negative side effect ethical issue, purposeful

Process of disposal of obsolete and surplus material. By negotiation by which buyers approaches for the purchase of such materials. Auction. Tenders.

Material handling Moving physical objects from one place to another as parts, components, sub assemblies, raw materials, or finished goods ready for shipment. Defined as the function dealing with the preparation, placing and positioning of materials to facilitate their movement or storage. The moving of materials from raw material store to through production to ultimate consumer with least expenditure of time, effort so as to produce maximum productive efficiency and lowest handling cost

/")