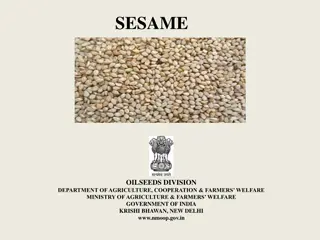

Investing in Sesame Seeds Hulling and Export in Ethiopia: A Lucrative Opportunity

Ethiopia, the world's 3rd largest sesame exporter, presents a compelling investment case for establishing a sesame hulling plant. With a high-quality product and a projected IRR of 40%, this venture offers substantial revenue potential in the lucrative bakery and confectionary markets. Political stability, strategic location, and growing economy further enhance the appeal of this investment opportunity.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. Download presentation by click this link. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

E N D

Presentation Transcript

The Business Case for Investing in the Hulling and Export of Sesame Seeds in Ethiopia Investor Presentation May 2012

Hulling and Export of Sesame Seeds Introduction This investment case has been prepared by the Monitor Group as part of Ethiopia s presentation at the Grow Africa Forum. The intended audience are Regional and International investors who are looking for strategic or financial investments in Sub-Saharan Africa. Objective of this Document The investment opportunity identified is the establishment of a sesame hulling plant with an annual output capacity of 10,000 MT through a joint venture agreement with a local partner in Ethiopia. The high quality hulled sesame seed produced would be packaged and exported to international purchasers for use in bakery and confectionary applications. An initial investment of $7.0 million is projected to return an IRR of 40% without leverage after five years. Opportunity Definition Note: This investment case was prepared by Monitor Group, an independent, global management consultancy firm. Funding for the investment case analysis was provided by the U.S. Agency for International Development as technical assistance to the Ethiopian Agricultural Transformation Agency Its findings are based on public and proprietary information, as well as information gathered by Monitor Group through field investigation and qualitative interviews with industry experts and other key stakeholders. Monitor Group does not make any representation or warranty, express or implied, as to the accuracy, completeness, or correctness of the information contained herein, nor does it accept any liability for any loss or damage, howsoever caused, arising from any errors, omissions, or reliance on any information or views contained in this document. Monitor Group is not a financial advisor; therefore, this document does not represent financial advice. Monitor Group Proprietary 2

Hulling and Export of Sesame Seeds Summary 1 Market Opportunity Ethiopia is the world s 3rd largest sesame exporter, sourcing 14% of the global market for raw seeds. These seeds are then processed abroad Sesame is one of Ethiopia s highest value crops, earning $1,330 / MT raw. Hulling sesame domestically would add revenue of $180-200 / MT Current domestic processing capacity is limited, presenting a significant opportunity to establish a high quality value addition hulling facility 2 Competitive Advantages Ethiopia is one of the fastest growing economies in Africa Political stability and ongoing government infrastructure investments Large domestic market, and good access to regional and international export markets Investors benefit from good agro-climatic conditions and generous investment incentives 3 Investment Highlights High quality hulled sesame sold to international purchasers can result in revenue of $21.8M USD by 2018 Opportunity to invest $7.0M into the hulling of sesame seeds, resulting in forecasted project IRR of 40%1, with net income of $2.1M by 2018 1 IRR of 40% represents IRR without any leverage Monitor Group Proprietary 3

Hulling and Export of Sesame Seeds Market Opportunity 1 Market Opportunity Ethiopia is the world s 3rd largest sesame exporter, sourcing 14% of the global market for raw seeds. These seeds are then processed abroad Sesame is one of Ethiopia s highest value crops, earning $1,330 / MT raw. Hulling sesame domestically would add revenue of $180-200 / MT Current domestic processing capacity is limited, presenting a significant opportunity to establish a high quality value addition hulling facility 2 Competitive Advantages Ethiopia is one of the fastest growing economies in Africa Political stability and ongoing government infrastructure investments Large domestic market, and good access to regional and international export markets Investors benefit from good agro-climatic conditions and generous investment incentives 3 Investment Highlights High quality hulled sesame sold to international purchasers can result in revenue of $21.8M USD by 2018 Opportunity to invest $7.0M into the hulling of sesame seeds, resulting in forecasted project IRR of 40%1, with net income of $2.1M by 2018 Monitor Group Proprietary 4

Hulled Sesame Market Opportunity Global Sesame Exports Ethiopia is a major supplier in a growing global sesame export market, accounting for 14% of all raw sesame exports in 2010 Global Sesame Exports Global Sesame Exports, USD (2006-2010) Value of global sesame market is growing at 28% and quantity is growing at 10% 3,750 3,000 28% USD ( 000) 2,167 2,250 1,593 1,600 1,500 1,082 797 Ethiopia is the 3rd largest global sesame exporter 750 0 2006 2007 2008 2009 2010 Nigeria is the largest exporter, and India is 2nd Global Sesame Exports, MT (2006-2010) 2,500 Ethiopian exports in MT grew at a 10% CAGR 06- 10, and $ value grew at 25% in the same time Metric Tons ( 000) 2,000 10% 1,360 1,500 1,185 1,117 1,057 946 1,000 500 Ethiopian sesame is known within the industry for its high quality 0 2006 2007 2008 2009 2010 Export Year Source: International Trade Centre Monitor Group Proprietary 5

Hulled Sesame Market Opportunity Global Price Comparisons Despite Ethiopia s prominence in the export market, it earns less per ton than the global average in key end-markets, due to insufficiently supplying higher earning hulled sesame Global Price Comparison Sesame Import Price / Ton by Country (2008) Ethiopian sesame commands a price premium in China and Turkey, where it is processed and re-exported Price Difference Importer Ethiopia Global China $1,453 $1,164 $289 In key markets like the US, the Netherlands, and Israel, which look to purchase processed goods for end- market use, Ethiopian sesame is losing potential revenue by only exporting it in a raw form Israel $1,789 $1,849 ($60) Turkey $1,621 $1,529 $92 $1,769 $1,643 $126 Mexico Investing in a hulling facility will help close the gap and tap into these new, high value markets USA $1,858 $2,363 ($505) Netherlands $1,886 $2,072 ($186) Source: International Trade Centre, 2009 Oilseeds Business Opportunities, Monitor Analysis Monitor Group Proprietary 6

Hulled Sesame Market Opportunity Price Benefit of Hulling Sesame To close the gap between current and potential revenue from sesame exports, Ethiopia must build processing capacity to add more value through the establishment of more hulling facilities Potential Export Value of 2010 Production ($USD) by % Sesame Hulled1 350 316 312 308 306 34 303 15 300 Export Value (USD M) Export value with 4% hulling 51 86 120 250 200 150 288 271 256 226 100 196 Hulled 50 Raw 0 4% 10% 15% 25% 35% % Sesame Hulled Prior to Export 1 MT hulled sesame earns between $180-200 USD more than 1 MT raw sesame Current estimates have hulling facilities in Ethiopia processing just 4% of the total sesame exported from the country If 35% of 2010 exports had been hulled, rather than 4%, export revenue would have been greater by ~$13M USD Hulling additional 31% of sesame to reach 35% hulled exports would have an associated cost of $130 / MT, a total of $10.7M 1Assumes raw seeds earn $1,322 USD / ton and hulled seeds earn $1,502 USD / ton. Using the 2010 production volume, each column estimates potential sesame market export value at increasing intervals of processed sesame seeds Monitor Group Proprietary Source: International Trade Centre, 2009 Oilseeds Business Opportunities, Selet Hulling Report, Monitor Analysis 7

Hulled Sesame Market Opportunity Market Distribution Strategy Purchase markets for raw and hulled sesame are quite different; Ethiopia can target more upscale end-markets and earn a price premium for high quality processing 96% Exports, $1,330 / MT Value add of $180-200 / MT Processor Companies in India, China, Israel, and Turkey purchase raw seeds for hulling and other processing Producer End-Market Ethiopia exports the vast majority of its sesame raw to be produced in end markets Purchasers in the US, Japan, Mexico, and European Union demand high quality hulled sesame for use in bakery and confectionary applications 4% Exports, $1,530 / MT Potential to increase value by supplying directly to end-markets Ethiopia is losing out on the opportunity to increase sesame revenues by only exporting seeds raw. Developing hulling facilities will position the country to grow its sesame market and better establish its international market position. Source: International Trade Centre, Investor Interviews, Monitor Analysis Monitor Group Proprietary 8

Hulled Sesame Market Opportunity Competitive Landscape Domestic capacity for sesame hulling is limited, and significant competition will come from established international processing centers such as India and China Domestic International There are relatively few operational hulling facilities in Ethiopia Selet Hulling PLC Agro-Prom International A few other processing facilities are said to be in development, including a tahini factory by Sheba Ltd. Domestic farming and processing methods have room forimproved operational efficiency, which will be necessary to compete against international market prices Competition is likely to come primarily from international processing hubs like India and China India and China both have well- established hulling and other processing facilities that operate at high efficiency The high efficiency and economies of scale allow for lower prices Israel, Jordan, and other Middle Eastern countries are also competitive in sesame processing, producing end-products like tahini and sesame oil Source: Investor and Stakeholder Interviews, Monitor Analysis Monitor Group Proprietary 9

Hulling and Export of Sesame Seeds Competitive Advantages 1 Market Opportunity Ethiopia is the world s 3rd largest sesame exporter, sourcing 14% of the global market for raw seeds. These seeds are then processed abroad Sesame is one of Ethiopia s highest value crops, earning $1,330 / MT raw. Hulling sesame domestically would add revenue of $180-200 / MT Current domestic processing capacity is limited, presenting a significant opportunity to establish a high quality value addition hulling facility 2 Competitive Advantages Ethiopia is one of the fastest growing economies in Africa Political stability and ongoing government infrastructure investments Large domestic market, and good access to regional and international export markets Investors benefit from good agro-climatic conditions and generous investment incentives 3 Investment Highlights High quality hulled sesame sold to international purchasers can result in revenue of $21.8M USD by 2018 Opportunity to invest $7.0M into the hulling of sesame seeds, resulting in forecasted project IRR of 40%1, with net income of $2.1M by 2018 Monitor Group Proprietary 10

Ethiopias Competitive Advantage Economy and Business Environment Ethiopia enjoys strong economic growth and political stability, as well as strong government emphasis on attracting private sector investment GDP Growth Rates, 2005-2010 Attractive Performance and Governance 11% annual GDP growth rate since 2005 11% 11% Ranked as 3rd fastest growing economy in the world for the next four years by The Economist, behind China and India 9% Political stability which fosters a peaceful and secure working environment 7% Percentage Simple taxation structure and tax breaks for sesame investors 4% 4% 4% Robust policy framework in the Growth and Transformation Plan which also focuses on private sector investment promoting growth Zero tolerance to corruption and fraud South Africa Russia Brazil Nigeria India Ethiopia China Source: World DataBank; Monitor Analysis; The Economist; UN; ICC, Ministry of Finance and Economic Development Monitor Group Proprietary 11

Ethiopias Competitive Advantage Investment Incentives Sesame investors in Ethiopia benefit from a generous range of investment incentives, including affordable land rental rates, tax holidays and import/export incentives Availability of Resources Tax Environment Import/Export Incentives More than 80 Mn Ha of arable land is available Industrial land available at $6-7 per ha per year in Oromia for a lease period of 80 years In Addis Ababa, industrial land for hulling facility can be leased for $12-22 per sq meter Income tax holiday for ~2-7 years for manufacturing, agricultural and agro-industrial investment Companies earning over 50% of their revenue from exports, like the planned sesame hulling facility,receive a tax holiday of 5 years; all others receive a 2 year tax holiday Losses during the tax holiday are carried forward for half the exemption period 100% customs import duty exemption Agricultural and industrial machinery / equipment imported for investment purposes Raw materials for production of export goods Spare parts worth 15% of total investment capital goods Heavy investment planned by government in developing roads, electricity, water ($70B over 5 years) Export duty exemptions for products and services developed domestically Young, disciplined and trainable labor is available at relatively low cost Salaries are $50 90 per month for graduates Good standards of spoken and written English Simplified tax structures, e.g. universal corporate income tax rate of 30% Export sector benefits include Export Credit Scheme, Duty Drawback Scheme, Foreign Exchange Retention Scheme, Foreign Credit and Loan Schemes Access to 70% of capital investment financing at reasonable rates Source: Ethiopian Investment Agency Monitor Group Proprietary 12

Ethiopias Competitive Advantage Market Access Investors in a sesame processing facility in Ethiopia will also benefit from access to large domestic, regional, and international markets COMESA Trading Block and Regional Map Access to Adjacent Markets Ethiopia s population of 82.9M is the second largest in Sub-Saharan Africa 44% of the population is under age 15 and 73% is under 30 Ethiopia is geographically well-positioned to serve several export markets Its location in the Horn of Africa places it at the crossroads between Africa, the Middle East and Asia Membership in Common Market for Eastern and Southern Africa (COMESA) enhances access to 23 member countries and their population of more than 420 million Ethiopia also enjoys Duty Free and Quota Free (DFQF) privilege extended by international markets of USA, European Union, China and India 82.9 0.9 71.7 Djibouti 8.1 33.4 Ethiopia South Sudan 40.5 10.6 Uganda Kenya Rwanda Democratic Republic of the Congo 44.8 8.4 Tanzania Tanzania Burundi 10.0 Population (Millions) COMESA Members Other Trade Countries Source: World Bank, Doing Business , 2012; Monitor Analysis Monitor Group Proprietary 13

Ethiopias Competitive Advantage Sesame Supply Dynamics Sesame is one of Ethiopia s top performing export crops and shows potential for rapid increase in cash value and production quantities Major Exports by Crop, Ethiopia 2011 Strong Supply of Sesame Seeds Sesame seeds are Ethiopia s 2nd largest cash export crop behind coffee, and largest in terms of MT MT 365,689 USD ( 000) 331,047 Current yields of 0.7 MT / ha have potential to increase significantly with use of modern farming practices 255,783 247,149 166,934 385,000 ha under cultivation for sesame, largely in northwestern and western Ethiopia, involving 764,000 smallholder farmers 129,833 77,682 60,246 44,655 42,293 Near-organic production practices enhance Ethiopia s global reputation for producing high quality sesame Sesame Fresh Vegetables Coffee Dry Beans Oilseeds, NES Source: International Trade Centre, Monitor Analysis Monitor Group Proprietary 14

Ethiopias Competitive Advantage Agro-Climatic Conditions and Land Availability Ethiopia possesses favorable agro-climatic conditions for sesame production, as well as abundant land for agricultural activities Attractive Agri-Climatic Conditions Land Availability and Climate Ethiopia is home to 18 major agro-ecological zones and 49 agro-ecological sub-zones The country has the soils and climate suitable for growing over ~150 types of crops, including high value commodities such as coffee, sesame and other oilseeds, cereals, spices, fruits and vegetables Sesame grows particularly well in the Northern and Western Ethiopia Ethiopia has two main harvest seasons, which are heavily reliant on annual rainfall The bulk of harvesting is completed from October to December following the Meher growing season Just 21% of arable land is currently under cultivation, leaving great potential for growth in the agriculture sector Key Land Statistics Land (ha): 111.5M Arable land (ha): 74.5M Cultivated land (ha): 15.4M Annual Rainfall (western region): 200 cm Primary Harvest Seasons Belg Meher Rainy Season February June June October Harvest Season Jul - Sept Oct - Dec % of Crop Production 5-10% 90-95% Source: USDA Foreign Agriculture Service; Oakland Institute: Understanding Land Investment Deals in Africa, Ethiopia Country Report Monitor Group Proprietary 15

Ethiopias Competitive Advantage Planned Government Enabling Environment Investments The Growth and Transformation Plan represents an ambitious set of national investments that will significantly upgrade both hard and soft infrastructure and facilitate sesame processing Growth and Transformation Plan Projected Spending ($B USD) Key Highlights of Growth and Transformation Plan Building 71,000 km of new roads, including all-weather roads to virtually all kebele administrations and an expressway linking Addis Ababa to Adama (a key route to facilitate export and import trade) Constructing 2,395 km of new railways linking Addis Ababa with Djibouti, linking selected domestic cities, and within Addis Ababa itself Laying 132,000 km of new electricity distribution lines and expanding electricity coverage to 75% of the country Expanding the water supply infrastructure to cover 99% of the population and the drilling of some 3,000 water wells per year Increasing irrigation coverage from 3% to 16% of total farm land Increasing (net) primary enrollment to 100%; raising the number of students at government universities to near half a million students (from 185,000 at present) 16 16 15 15 11 2010/11 2011/12 2012/13 2013/14 2014/15 Source: Access Capital Macroeconomic Handbook 2011/12 Monitor Group Proprietary 16

Ethiopias Competitive Advantage Support of the Agricultural Transformation Agency The Agricultural Transformation Agency (ATA) represents a high performance change agent, tasked with solving the key problems faced by the Ethiopian agricultural sector Origins of ATA ATA s Approach Established Q4 2010 on the recommendation of a set of Gates Foundation diagnostics submitted directly to the Prime Minister ATA s key activities include: Leading problem solving efforts to identify solutions to systemic bottlenecks Created as an independent organization modeled after Taiwan and Korean acceleration units Supporting implementation by providing project management, capability building etc. ATA s overall objective is to support achievement of the Growth and Transformation Plan agri-related targets Enhancing linkages and coordination among agri-stakeholders Enabling Factors for ATA s Success Example ATA Initiatives Reporting line directly to the Prime Minister Attracting and facilitating the entry of agri-investors Private-sector orientation, but with strong linkages to public entities e.g. Ministry of Agriculture Note: Project Management Unit to support agri- investors currently being developed, to be housed within ATA Hybrid staffing model - long-term goal is for ATA to be fully staffed by Ethiopian civil service, but for initial give years, a hybrid model of international staff, local analysts and seconded public sector fellows Developing systemic interventions for key bottlenecks like financing, input supply and extension services, as well as multi-stakeholder roadmaps for specific crops, like oilseeds Monitor Group Proprietary 17

Hulling and Export of Sesame Seeds Investment Highlights 1 Market Opportunity Ethiopia is the world s 3rd largest sesame exporter, sourcing 14% of the global market for raw seeds. These seeds are then processed abroad Sesame is one of Ethiopia s highest value crops, earning $1,330 / MT raw. Hulling sesame domestically would add revenue of $180-200 / MT Current domestic processing capacity is limited, presenting a significant opportunity to establish a high quality value addition hulling facility 2 Competitive Advantages Ethiopia is one of the fastest growing economies in Africa Political stability and ongoing government infrastructure investments Large domestic market, and good access to regional and international export markets Investors benefit from good agro-climatic conditions and generous investment incentives 3 Investment Highlights High quality hulled sesame sold to international purchasers can result in revenue of $21.8M USD by 2018 Opportunity to invest $7.0M into the hulling of sesame seeds, resulting in forecasted project IRR of 40%1, with net income of $2.1M by 2018 Monitor Group Proprietary 18

Hulled Sesame Investment Highlights Operational Highlights Investment in a sesame hulling facility, supported by a nucleus farm and corresponding out- grower scheme to ensure quality supply, will open up access to higher paying end-markets Hulled seeds will be sold primarily to US, Japanese, Mexican, and European markets, which demand high quality hulled seeds Target Customers Hulled and branded sesame seeds packaged in 100 kg bags and sold in 1 MT units Potential expansion to tahini and / or sesame oil product lines Product Proposed mark-up of 15% over cost-to-produce, starting at $2,000 / ton in 2014 (year 1 of operations) As a commodity, price will fluctuate annually based on global market Price Majority of sales to wholesalers and distributors Direct sales to key end-users (major restaurant chains or food processors), depending on market relationships Channel Sesame hulling plant with capacity to produce 10,000 MT annually (year 5 capacity utilization target of 90%) Proposed location in Oromia, outside of Addis Ababa to be close to infrastructure (e.g. electricity, water) Processing Facility Nucleus farm (or contractual arrangement or cooperative equity partnership with supply quality assurance) of 300 hectares Supply supported by arrangements with 4,400 out-growers Sourcing Model Source: Monitor Analysis Monitor Group Proprietary 19

Hulled Sesame Investment Highlights Channel Cost Structure Cost assumptions suggest that 1 MT hulled sesame will sell at a margin of 10% to international purchasers; procurement will remain the primary cost driver Channel Cost Structure for 1 MT Hulled Sesame (Year Five) 10% 100% 3% 8% 2% 0% 6% 70% Percentage of Unit Price Procurement Cultivation/Outgrower Expenses Labor Packaging Transportation Overhead (SG&A) Margin Channel Price Source: Monitor Analysis Monitor Group Proprietary 20

Hulled Sesame Investment Highlights Financial Performance Summary The 2018 EBITDA margin of 10.1% compares favorably to listed comparatives, and revenues have been conservatively forecast to ramp up over the first five years Revenue (Million USD) & EBITDA Margin (%), 2014-2018 100 EBITDA % 21.8 Revenue 19.8 17.9 75 16.1 Million USD Percentage 12.4 50 25 9.9% 10.1% 10.1% 10.1% 10.1% 0 2014 2015 2016 2017 2018 Source: Monitor Analysis Monitor Group Proprietary 21

Hulled Sesame Investment Highlights Capital Investment and Forecast Returns An initial investment of $7.0M is required to reach revenue forecasts; without leverage the investment will deliver an IRR of 40% after five years and be cash positive by 2015 Investment (Year 0) Return (Year 5) Internal Rate of Return (IRR) 40% Total Capital Investment ($M) 7.01 Plant, Property, and Equipment 1.72 NPV ($M) 4.3 Cultivation Investment 2.7 2018 Revenue ($M) 21.8 Working Capital & Other1 2.6 2018 Net Income ($M) 2.1 Capital investment assumed to take place in Year 0; processing begins in Year 1 (2014) No debt assumed IRR can be improved to 47% with the addition of 70% debt (on fixed assets) Net profit margin ends at 9.5% Forecast Free Cash Flows (Million USD) Initial 1.8 1.2 1.0 Investment1 0.5 -2.2 -7.0 2013 2014 2015 2016 2017 2018 1The assumption that all capital investment will take place in year zero is conservative, and investment can be staggered over the initial business setup phase; 2The model assumes that the hulling facility will not engage in significant cleaning activities, but a cleaning machine could be purchased for $600,000 USD. This cost covers a new, high quality cleaning machine that would meet European and Japanese quality standards Source: Monitor Analysis, Investor Interviews Monitor Group Proprietary 22

Hulled Sesame Investment Highlights Key Risks and Mitigation Options Several key risks have been identified and must be addressed to ensure the success of the sesame hulling facility Risk Parameter High Med Low Mitigation Options Leverage government investments in irrigation systems under the GTP Weather and crop insurance financed by cooperatives Forward agreements / contracts with sesame producers Incentivize quality and quantity of production Work with financial cooperatives to provide advance credit to out-growers Coordinate with ATA s Cooperatives Team to select advanced partner cooperatives Invest in training and extension services for farmers to implement modern practices Work with ATA s planned PMU to secure ECX exemption Participate in Public-Private forums to have a voice in policy discussions Facilitate government involvement and work closely with the ATA s planned PMU Partner with international traders who have existing global relationships Invest in marketing and advertising overseas Engage in forward contracts with sesame cooperatives, offering market price premium Purchase / store stock in advance to hedge risk Environmental Factors - Droughts or excessive rains, which may adversely affect sesame harvests Variable Commodity Prices - Breach of supply contracts when more lucrative prices can be found elsewhere Supply Chain Risks Inability to Distribute / Finance Inputs - Farmers unable to access necessary financing for inputs Low Capacity and Productivity of SHFs - Outdated agronomic practices and limited resources lead to reduced yields Uncertain Policy / Regulatory Environment - Unanticipated costs from sudden policy changes; getting exemption from ECX can be a challenge Regulator y Risks Bureaucracy/Lack of Coordination - Delays or blocks in processes such as land allocation Access to Export Markets - Slow uptake of Ethiopian hulled sesame among new international markets (including U.S., Japan) Market Risks High Inflation - Cost increase and competitiveness erosion from rising inflation Financial Risks Source: Monitor Analysis Monitor Group Proprietary 23

Hulled Sesame Investment Highlights Sensitivity Analysis Sales price, crop production yields, and cost of raw materials have been identified as having the greatest uncertainty and downside potential, and will necessitate targeted mitigation steps Internal Rate of Return (IRR) Downside Sensitivity Base Case IRR 39.6% Upside Sensitivity Input Lever Mitigation Steps Investment in cultivation and out-grower scheme to improve agronomic practices and resulting crop yields Yields improve at 0% Yields improve at 10% 13.3% 51.2% Crop Yields Investment in cultivation to improve yield / ha and careful negotiation with co-ops and farmers Costs inflate at 15% Costs inflate at 2% Cost of Raw Materials N/A1 71.4% Substantial marketing and advertising efforts to promote Ethiopian sesame as premium Improve operational efficiency to reduce COGS and price sensitivity 80% Price lower by 10% Price higher by 10% Sales Price N/A1 73.9% 0% 10% 20% 30% 40% 50% 60% 70% 1 N/A represents a negative Net Present Value for the scenario that was tested which means an IRR cannot be calculated Source: Monitor Analysis Monitor Group Proprietary 24

Hulled Sesame Investment Highlights Key Enabling Requirements To support the sesame hulling facility and lower investment risks, multiple interventions are being considered, and in some cases implemented, by public stakeholders and donors Public / Donor Initiatives to Satisfy Key Enabling Requirements SHF access to quality seed inputs, warehousing, and machinery SHF access to credit/insurance Training and education of SHFs in modern sesame farming practices Value chain approach to increasing capacity of sesame producers Simplified, transparent and time-bound land acquisition processes Simplified, transparent and time-bound business- registration/licensing processes Credit/financing availability for sesame processors Sufficient volume and quality of infrastructure (e.g. electricity, roads for transportation) Supply Market Linkage Processing End Market Sufficient volume and quality of infrastructure (e.g. roads) to support transport from sesame producing regions to processing facility Negotiation of long-term contracts Sufficient volume and quality of infrastructure to deliver hulled sesame to end market (e.g. ports) Note: Key public stakeholders and donors include: Ministry of Agriculture, Agricultural Transformation Agency, USAID, DFID, ACDI/VOCA and others Monitor Group Proprietary 25

Hulling and Export of Sesame Seeds Who Should Invest? The sesame hulling investment opportunity will be attractive to operational firms looking to build scale and sourcing reach, and financial firms driven by high scalability and social impact Opportunity Attraction Investor Profiles Operational Investors Increased Product Traceability Local traders looking to backward integrate into processing to add value to export productsand / or build sourcing base in the region Expanded Sourcing Network International investors looking to gain supply security by working more closely with producers and introduce traceability to sesame export supply Attractive Returns Financial Investors Financial investors looking for projects with high scalability and return potential Social / SHF Impact Financial investors looking to drive social impact to SHFs Monitor Group Proprietary 26

Hulling and Export of Sesame Seeds Way Forward This investment case is intended to foster interest/awareness; in order to successfully execute, prospective investors will need to take further steps to realize the attractive opportunity Build relationships with ATA, MoA, MoTI, and USAID, amongst others, to ensure support for land acquisition and setting up operations Initiate Public / Donor Dialogue Perform, or outsource, an independent due diligence process, to identify operational and capital cost structures, and identify consumers willingness to pay Perform Own Due Diligence Enter into contractual relationships with cooperatives and out-growers, to ensure raw material supply Identify Procurement Arrangements Identify and contract key procurement sources, including packaging and transport Build Consumer Market Platform Design and implement sustained advertising and marketing strategy, to build educate consumers and convert consumer interest to action Khalid Bomba, CEO, ATA (khalid.bomba@ata.gov.et) Contact Details Mirafe Marcos, Special Programs Officer, ATA (mirafe.marcos@ata.gov.et) Monitor Group Proprietary 27

Hulling and Export of Sesame Seeds Appendix Monitor Group Proprietary 28

Appendix Abbreviations and Acronyms Gross Domestic Product Government of Ethiopia Growth and Transformation Plan Hectare Hectoliters International Criminal Court International Finance Corporation Internal Rate of Return Kilogram Ministry of Agriculture Ministry of Trade & Industry - Ethiopia Metric Ton Non Governmental Organization Net Present Value Private Equity Project Management Unit Selling, General, and Administrative Costs Smallholder Farmer Technical Assistance United Nations United States Agency for International Development US Department of Agriculture World Economic Forum World Food Program GDP GOE GTP HA HL ICC IFC IRR KG MoA MoTI MT NGO NPV PE PMU SG&A SHF TA UN Agricultural Cooperative Development International / Volunteers in Overseas Cooperative Assistance ACDI/VOCA African Development Bank Agricultural Transformation Agency Build-Operate-Transfer Compound Annual Growth Rate Cost of Goods Sold Consumer Packaged Goods ADB ATA BOT CAGR COGS CPG Common Market for Eastern and Southern Africa COMESA Central Statistical Agency of Ethiopia CSA Ethiopia Development Bank of Ethiopia DBE Department for International Development DFID Duty Free and Quota Free DFQF Earnings Before Interest, Taxes, Depreciation, and Amortization EBITDA Ethiopian Investment Agency EIA Ethiopian Pulses, Oilseeds , and Spices Producers and Exporters Association USAID EPOSPEA USDA WEF WFP Food and Agriculture Organization FAO Fast Moving Consumer Packaged Goods FMCPG Monitor Group Proprietary 29

Appendix Potential Investors / Partners for Sesame Hulling Plant Potential investors and partners span the value chain from input supply to end-market off- takers Input Supply and Research Production Processing End-Market Bayer John Deere Syngenta Yara Midroc Cooperatives International traders/processors e.g. Olam Trading Local traders/processors e.g. Mullege EPOPSEA (Exporters Association) Traders e.g. Hakan Agro Access Capital Schulze Global Investments Development Bank of Ethiopia Zemen Bank Financial Investors Farm Africa USAID Technoserve ACDI/VOCA Gates IFC ADB Donors/NGOs List of noted investors / partners was developed from initial interest conversations with no formal or verbal commitments attached Note: List of interested investors and partners is preliminary and not exhaustive; identification does not imply any form of obligation or concrete commitment on the part of listed investors and partners Monitor Group Proprietary 30

Appendix Key Financial Assumptions (1/2) The key financial assumptions for the investment case include capital expenditure, cost of the out-grower program, working capital requirements, inflation and tax treatments Capital Expenditure ($ M) Cost of Out-grower Program ($M USD) Total Cost to Company (2013) $2.7 Total Capital Investment ($M) 7.0 Harvest cost / ha (nucleus) $1,000 Building Costs 0.7 Total harvest cost (nucleus) $300,000 Equipment Costs 1.0 Harvest cost / ha (out-growers) $350.00 Cultivation 2.7 Total harvest cost (out-growers) $2,737,445 Working Capital and Other 2.6 Working Capital Requirements Tax Treatments & Inflation Corporate Tax Rate Straight Line Depreciation for Plant (years) Straight Line Depreciation for Equipment and Infrastructure(years) Carry for Tax Losses (years) Tax Holiday for Export Companies (years) Inflation Rate 30% Percent of Sales 21% 20 Working Capital Considerations: Inventory Days 180 10 5 5 12% Source: Team Discussions, Monitor Analysis 31

Appendix Key Financial Assumptions (2/2) Key assumptions for revenue and investment returns include capacity utilization and costs of goods sold Projected Hulled Sesame Investment Revenues 2014 2015 2016 2017 2018 Maximum Capacity (MT) 10,000 10,000 10,000 10,000 10,000 Utilization Rate (%) 60% 75% 80% 85% 90% Unit Sales (MT) 6,000 7,500 8,000 8,500 9,000 Operating Revenue ($M) $12.4 $16.1 $17.9 $19.8 $21.8 General and Admin Costs in 2014 ($) Cost of Goods Sold in 2014 ($ / MT) Raw Material Indirect Labor $46,519 $1,378 Cultivation / Out-grower Costs Utilities $77,833 $170 Labor Costs Maintenance $28,600 $7 Marketing $32,113 Packaging $36 Transportation (Farm to Plant) Selling Costs (at 2%) $247,693 $53 Transportation (Plant to Port) SG&A Total $433,172 $151 Total $1,795 Source: Team Discussions, Monitor Analysis 32

Appendix Financial Statements Under 100% Equity (1/2) Forecast Income Statement Assuming a 100% Equity Funded Investment ($M) 2014 $12.38 $12.38 $8.27 $1.02 $0.32 $0.22 $0.91 $10.73 $1.66 $0.43 $0.05 $0.08 $0.03 $0.03 $0.25 $1.22 9.9% $0.14 $0.00 $1.09 $0.00 $1.09 2015 $16.14 $16.14 $10.94 $1.20 $0.40 $0.30 $1.13 $13.98 $2.16 $0.53 $0.05 $0.09 $0.03 $0.04 $0.32 $1.63 10.1% $0.14 $0.00 $1.50 $0.00 $1.50 2016 $17.88 $17.88 $12.27 $1.22 $0.42 $0.36 $1.21 $15.48 $2.40 $0.59 $0.06 $0.10 $0.04 $0.04 $0.36 $1.81 10.1% $0.14 $0.00 $1.67 $0.00 $1.67 2017 $19.76 $19.76 $13.70 $1.24 $0.45 $0.43 $1.29 $17.10 $2.66 $0.66 $0.07 $0.11 $0.04 $0.05 $0.40 $2.00 10.1% $0.14 $0.00 $1.87 $0.00 $1.87 2018 $21.77 $21.77 $15.24 $1.26 $0.47 $0.51 $1.36 $18.84 $2.93 $0.73 $0.07 $0.12 $0.05 $0.05 $0.44 $2.21 10.1% $0.14 $0.00 $2.07 $0.00 $2.07 Revenue Total Revenues COGS - Raw Materials COGS - Cultivation / Out-grower Expenses COGS - Transportation (Farm to Plant) COGS - Packaging COGS - Transportation (Plant to Port) Total COGS Gross Profit SG&A Total Indirect Labor Utilities Maintenance Marketing Selling Costs EBITDA EBITDA % Depreciation Interest Earnings Before Taxes Taxes Net Income / NOPAT Note: The base case assumed a 100% Equity and 0% Debt model, given that excess demand for debt in Ethiopia, and the current lack of capacity in the nation s banks to process debt applications, has led to difficulty accessing debt; also modeled for 70% debt, which is the maximum Ethiopian banks are willing to cover for agricultural investors Source: Team Discussions, Monitor Analysis 33

Appendix Financial Statements Under 100% Equity (2/2) Forecast Balance Sheet Assuming a 100% Equity Funded Investment ($M) 2013 $1.70 $0.00 $0.00 $1.70 $0.00 $0.00 2014 $1.57 $0.00 $2.60 $4.17 $0.00 $0.00 2015 $1.43 $0.00 $3.39 $4.82 $0.00 $0.00 2016 $1.30 $0.00 $3.76 $5.05 $0.00 $0.00 2017 $1.16 $0.00 $4.15 $5.31 $0.00 $0.00 2018 $1.03 $0.00 $4.57 $5.60 $0.00 $0.00 PPE Net, Other Assets Working Capital Total Assets Long Term Debt Total Liabilities Shareholders Equity $1.70 $4.17 $4.82 $5.05 $5.31 $5.60 Forecast Cash Flow Statement Assuming a 100% Equity Funded Investment ($M) 2013 2014 2015 2016 2017 2018 Cash Flow from Operations Earnings from P&L Depreciation Net Interest (after tax) (Change in net working capital) Total Cash Flow from Operations $0.00 $0.00 $0.00 $0.00 $0.00 $1.09 $0.14 $0.00 -$2.60 -$1.38 $1.50 $0.14 $0.00 -$0.79 $0.84 $1.67 $0.14 $0.00 -$0.37 $1.44 $1.87 $0.14 $0.00 -$0.39 $1.61 $2.07 $0.14 $0.00 -$0.42 $1.78 Investment (Capex) Terminal Value Free Cash Flows Cumulative Cash Flows -$4.44 $0.00 $0.00 $0.00 $0.00 $0.00 $19.63 -$4.44 -$1.38 $0.84 $1.44 $1.61 $21.41 Note: The base case assumed a 100% Equity and 0% Debt model, given that excess demand for debt in Ethiopia, and the current lack of capacity in the nation s banks to process debt applications, has led to difficulty accessing debt; also modeled for 70% debt, which is the maximum Ethiopian banks are willing to cover for agricultural investors Source: Team Discussions, Monitor Analysis 34

Appendix Financial Statements Under 30% Equity (1/2) Forecast Income Statement Assuming a 70% Equity Funded Investment ($M) 2014 $12.38 $12.38 $8.27 $1.02 $0.32 $0.22 $0.91 $10.73 $1.66 $0.43 $0.05 $0.08 $0.03 $0.03 $0.25 $1.22 9.9% $0.14 $0.11 $0.97 $0.00 $0.97 2015 $16.14 $16.14 $10.94 $1.20 $0.40 $0.30 $1.13 $13.98 $2.16 $0.53 $0.05 $0.09 $0.03 $0.04 $0.32 $1.63 10.1% $0.14 $0.11 $1.39 $0.00 $1.39 2016 $17.88 $17.88 $12.27 $1.22 $0.42 $0.36 $1.21 $15.48 $2.40 $0.59 $0.06 $0.10 $0.04 $0.04 $0.36 $1.81 10.1% $0.14 $0.10 $1.58 $0.00 $1.58 2017 $19.76 $19.76 $13.70 $1.24 $0.45 $0.43 $1.29 $17.10 $2.66 $0.66 $0.07 $0.11 $0.04 $0.05 $0.40 $2.00 10.1% $0.14 $0.09 $1.78 $0.00 $1.78 2018 $21.77 $21.77 $15.24 $1.26 $0.47 $0.51 $1.36 $18.84 $2.93 $0.73 $0.07 $0.12 $0.05 $0.05 $0.44 $2.21 10.1% $0.14 $0.08 $1.99 $0.00 $1.99 Revenue Total Revenues COGS - Raw Materials COGS - Cultivation / Out-grower Expenses COGS - Transportation (Farm to Plant) COGS - Packaging COGS - Transportation (Plant to Port) Total COGS Gross Profit SG&A Total Indirect Labor Utilities Maintenance Marketing Selling Costs EBITDA EBITDA % Depreciation Interest Earnings Before Taxes Taxes Net Income / NOPAT Note: The base case assumed a 100% Equity and 0% Debt model, given that excess demand for debt in Ethiopia, and the current lack of capacity in the nation s banks to process debt applications, has led to difficulty accessing debt; also modeled for 70% debt, which is the maximum Ethiopian banks are willing to cover for agricultural investors Source: Team Discussions, Monitor Analysis 35

Appendix Financial Statements Under 30% Equity (2/2) Forecast Balance Sheet Assuming a 30% Equity Funded Investment ($M) 2013 $1.70 $0.00 $0.00 $1.70 $1.19 $1.19 2014 $1.57 $0.00 $2.60 $4.17 $1.11 $1.11 2015 $1.43 $0.00 $3.39 $4.82 $1.03 $1.03 2016 $1.30 $0.00 $3.76 $5.05 $0.94 $0.94 2017 $1.16 $0.00 $4.15 $5.31 $0.84 $0.84 2018 $1.03 $0.00 $4.57 $5.60 $0.73 $0.73 PPE Net, Other Assets Working Capital Total Assets Long Term Debt Total Liabilities Shareholders Equity $0.51 $3.05 $3.79 $4.11 $4.47 $4.87 Forecast Cash Flow Statement Assuming a 30% Equity Funded Investment ($M) 2013 2014 2015 2016 2017 2018 Cash Flow from Operations Earnings from P&L Depreciation Net Interest (after tax) (Change in net working capital) Total Cash Flow from Operations $0.00 $0.00 $0.00 $0.00 $0.00 $0.97 $0.14 $0.08 -$2.60 -$1.41 $1.39 $0.14 $0.07 -$0.79 $0.81 $1.58 $0.14 $0.07 -$0.37 $1.41 $1.78 $0.14 $0.06 -$0.39 $1.58 $1.99 $0.14 $0.06 -$0.42 $1.76 Investment (Capex) Terminal Value Free Cash Flows Cumulative Cash Flows -$4.44 $0.00 $0.00 $0.00 $0.00 $0.00 $19.36 -$4.44 -$1.41 $0.81 $1.41 $1.58 $21.12 Note: The base case assumed a 100% Equity and 0% Debt model, given that excess demand for debt in Ethiopia, and the current lack of capacity in the nation s banks to process debt applications, has led to difficulty accessing debt; also modeled for 70% debt, which is the maximum Ethiopian banks are willing to cover for agricultural investors Source: Team Discussions, Monitor Analysis 36

Appendix Development Benefits The hulling facility will have significant social returns, increasing annual farmer income by 17.4% and engaging more than 4,400 SHF over the course of the investment Number of Smallholder Farmers Affected by Out-grower Scheme Unit 2014 2015 2016 2017 2018 Yields Nucleus Yield SHF Yield Annual Production Required Nucleus Production SHF Production Required MT / ha MT / ha MT / ha MT / year MT / year 1.20 1.00 7324 360 6,964 1.25 1.05 9155 376 8,779 1.31 1.09 9766 393 9,372 1.37 1.14 10376 411 9,965 1.43 1.19 10986 430 10,557 Smallholder Farmers Involved # SHFs 3,482 4,200 4,290 4,364 4,424 Projected Income Improvements 2014 (Year 1) Total SHF Income from Crop (USD) Total Potential SHF Income from Crop (USD) Total Increase in Income (USD) $2,003 $2,351 $348 Increase in Income (%) 17.4% Note: Income improvements for growers account solely for wages from sesame production Source: Investor Interviews, Monitor Analysis 37