Legal Provisions Regarding Affidavits and Liabilities in Financial Matters

The ARAA 2003 mandates that all plights must be supported by affidavits and payment of court fees. Affidavits are considered substantive evidence in court proceedings, allowing for judgment without witness deposition. Financial liabilities for mortgagees and guarantors are joint and several, with a specific order of repayment. Financial institutions are required to sell pledged properties before filing Artha Rin Mamla cases, following specific legal procedures. Failure to adhere to these regulations may result in legal action.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. Download presentation by click this link. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

E N D

Presentation Transcript

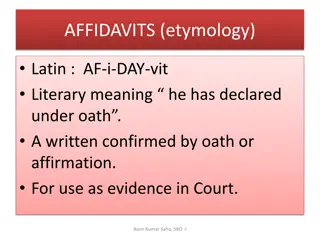

AFFIDAVIT AS SUBSTANTIVE EVIDENCE: (SECTION 6) ARAA 2003 says that the plaint should be supported by Affidavit and Ad Valorem court fees has to be paid with the plaint (section 6(2) of ARAA). Every plaint and written statements has to be attached with an affidavit and this affidavit shall be treated as substantive evidence so that the trial court may make instant order or pass judgment only upon perusing the concerned plaint or written statement together with other documentary evidence without deposition of any witness. This plaint supported by affidavit will be counted as substantial evidence and the court, in case of default or summary judgment, can give order or judgment by solely relying on the plaint without examining any witness (section 6(4) of ARAA)

LIABILITY OF MORTGAGOR AND GUARANTOR (SECTION 6): Generally the principal debtor, third party mortgagor and third party guarantor are jointly and severally liable for making repayment of the outstanding liability to the Financial Institution. Nevertheless when the dues are realized through execution, the principal debtor, third party mortgagor and third party guarantor are liable to pay the decreetal amount consecutively. That is, at first the principal debtor, then third party mortgagor and at last third party guarantor shall be liable to pay the decreetal amount.

PRIOR CONDITION TO FILE ARTHA RIN MAMLA: (SECTION 12) No financial institution is entitled to file an Artha Rin Mamla before the Adalat without adjusting the liability by selling the property (movable or immovable) under lien, pledge, hypothecation or registered mortgage of which the financial institution is lawfully authorized to sell by dint of irrevocable notarized power of attorney in case of movable property and registered power of attorney in case of immovable property.

If any property is given in mortgage or pledge or lien then before filing the plaint the financial institution has to sell the property and adjust the loan or has to fail after trying to sell the property. Please note that the financial institution has to have the lawful right or been given the right to sell the property [section 12 (1) and (3) of ARAA]. If the plaint has already been filed without the property being sold, then the plaintiff has to sell the property and adjust the loan and inform the court in written form [12(2) of ARAA].

For selling the above-mentioned property, the financial institutions shall follow the procedure of auction sale provided in Section 33 of the Ain so far as it is possible. After selling the property in question, if the financial institution fails to make delivery of possession to the purchaser, it can take recourse to the District Magistrate and the District Magistrate or his nominated Magistrate of the First Class upon satisfaction of mortgage against debt, shall take necessary step to transfer the possession of the property to the concerned purchaser on behalf of the Financial Institution.

NO SET OFF OR COUNTER CLAIM (SECTION 18) The borrower-defendant is not entitled to claim set off or counter claim by filing written statement in a Mamla filed against him by the Financial Institution.

NO ANALOGOUS HEARING (SECTION 18) If a borrower files a suit against any Financial Institutions before the general court and the Financial Institution again files another Mamla before the Artha Rin Adalat, then the two suits shall not be heard analogously in any of the said court in spite of the fact that the suits have been arisen out of the same cause of action.

NO DISMISSAL OF MAMLA (SECTION 19) No pending Mamla before the Artha Rin Adalat shall be dismissed on account of non-appearance of the plaintiff or any kind of failure on the part of the plaintiff. In this case the Adalat shall adjudicate the Mamla upon verification of the documentary evidence.

If the defendant is absent on any date of final hearing the court can ex parte dispose of the case by giving ex parte decree [section 19(1) of ARAA]. If the plaintiff is absent on any date or fails for any reason, the court cannot strike out the plaint. In this case the court has to scrutinise the papers and dispose of the matter accordingly [19(6) of ARAA] In this case, the defendant can vacate the ex parte decree by applying within 30 days of the date of passing of the decree or the date of his getting notified about the decree by depositing 10% of the decreed amount in the court or in the financial institution [section 19(2) and (3) of ARAA].

EX PARTE DECREE: (SECTION 19) The Adalat shall hear the suit ex parte and pass a decree against the defendant if the defendant does not appear before the court on the day fixed for hearing or when the Mamla is taken for hearing but the defendant is not available at that very time.

SET ASIDE EX PARTE DECREE: (SECTION 19) The defendant may file an application for setting aside the ex parte decree within 30 days from the day passing of the ex parte decree or from the day when the defendant come to know about the ex parte decree. In order to setting aside the ex parte decree, the defendant is required deposit 10% of the decreetal amount within 15 days from day of filing the application-

by cash payment to the concerned Financial Institution as recognition of claim made by the plaintiff, or by Bank Draft, Pay Order or any kind of Negotiable Instrument to the Court as security. Upon payment of the said 10% decreetal amount, the ex parte decree shall be set aside and the Mamla will be immediately restored in the original number and file; failing which the Adalat shall straightly dismiss the application for setting aside the ex parte decree.

PLAINT--------PLAINTIFF--------CREDITOR---FINANANCILA INSTITUTION----BANK WRITTEN STATEMENT--------DEFENDANT-DEBTOR- BORROWER- PERSON, COMPANY- THIRD PARTY-

")

:")

")

")

")

")

")

")