Understanding STD Revenue Clarifications for 340B Program

Explore how to utilize 340B revenue and savings within your program to benefit patients effectively. Learn about the regulations, best practices, and ways to reinvest back into your STD program for improving services and addressing disparities.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. Download presentation by click this link. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

E N D

Presentation Transcript

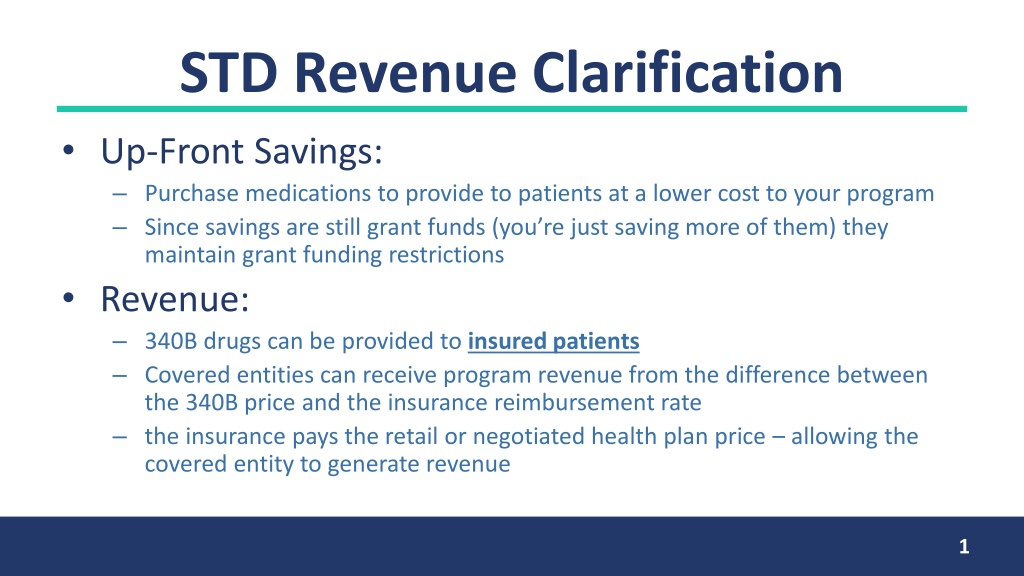

STD Revenue Clarification Up-Front Savings: Purchase medications to provide to patients at a lower cost to your program Since savings are still grant funds (you re just saving more of them) they maintain grant funding restrictions Revenue: 340B drugs can be provided to insured patients Covered entities can receive program revenue from the difference between the 340B price and the insurance reimbursement rate the insurance pays the retail or negotiated health plan price allowing the covered entity to generate revenue 1

STD Revenue Clarification Grantees, including sub-grantees, are required to use all 340B revenue and savings for activities that promote the purpose of their qualifying funding/federal grant There is no HRSA, CDC, or statutory regulation for program revenue 2

STD Revenue Clarification Ways STD 340B revenue can be reinvested back into an STD program: Expanding STD testing Additional staffing including outreach workers & DIS Providing supportive services Addressing health disparities Others, specific to your program operations & needs 3

STD Revenue Clarification Calculating 340B Net Financial Impact and Use of Savings, Apexus a. (pg. 1) Background:Although the 340B statute does not require covered entities to document what their 340B net financial impact is or how those savings are used, doing so is considered a best practice to demonstrate how the 340B Program expands access to underserved patient populations. b. (Middle of pg. 2) Although it is a best practice to align savings from the 340B Program directly to the cost of caring for the underserved, each covered entity may make its own determination as to which areas of benefit apply directly to its 340B Program. 4

STD Revenue Clarifiation GAO Report, United States Government Accountability Office Page 3: "Further, because the 340B program has no requirements on how 340B revenue can be used,10. FN10: According to HRSA, while there are no 340B-specifc requirements, all covered entities eligible for the program based on their grantee status may be required to use 340B revenue in accordance with their grant requirements. 5

STD Revenue Clarification Federal Register/Vol. 61, No. 207 Public Health Service Act There is no HRSA, CDC, or statutory regulation for program revenue It is because of this that programs can discern how to reinvest their revenue back into their STD program 6

Important Notes This is guidance and technical assistance is specific to the STD 340B Designation and is not applicable to other 340B covered entity types When implementing 340B programming, you should always use your own judgement and legal counsel to assist in ensuring compliance with 340B Program requirements as liability for compliance with 340B Program requirements resides solely with the covered entity. 7

Rebekah Horowitz rhorowitz@naccho.org (c) 215-964-7452 Stephanie S. Arnold Pang sarnold@ncsddc.org (c) 612-220-2446 Erin Fratto efratto@ncsddc.org (c) 801-450-7939