Managing Personal Finances: Understanding Income and Expenses

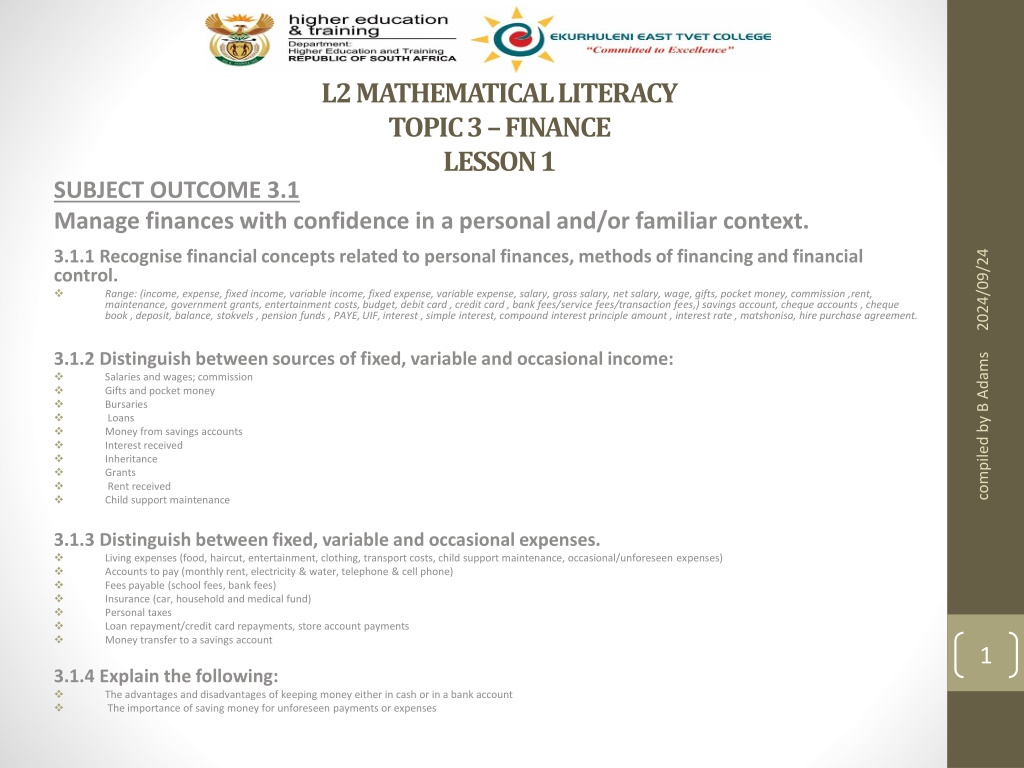

L2 MATHEMATICAL LITERACY

TOPIC 3 – FINANCE

LESSON 1

SUBJECT OUTCOME 3.1

Manage finances with confidence in a personal and/or familiar context.

3.1.1

Recognise financial concepts related to personal finances, methods of financing and financial

control.

Range: (income, expense, fixed income, variable income, fixed expense, variable expense, salary, gross salary, net salary, wage, gifts, pocket money, commission ,rent,

maintenance, government grants, entertainment costs, budget, debit card , credit card , bank fees/service fees/transaction fees,) savings account, cheque accounts , cheque

book , deposit, balance, stokvels , pension funds , PAYE, UIF, interest , simple interest, compound interest principle amount , interest rate , matshonisa, hire purchase agreement.

3.1.2

Distinguish between sources of fixed, variable and occasional income:

Salaries and wages; commission

Gifts and pocket money

Bursaries

Loans

Money from savings accounts

Interest received

Inheritance

Grants

Rent received

Child support maintenance

3.1.3

Distinguish between fixed, variable and occasional expenses.

Living expenses (food, haircut, entertainment, clothing, transport costs, child support maintenance, occasional/unforeseen expenses)

Accounts to pay (monthly rent, electricity & water, telephone & cell phone)

Fees payable (school fees, bank fees)

Insurance (car, household and medical fund)

Personal taxes

Loan repayment/credit card repayments, store account payments

Money transfer to a savings account

3.1.4

Explain the following:

The advantages and disadvantages of keeping money either in cash or in a bank account

The importance of saving money for unforeseen payments or expenses

2024/09/24

1

compiled by B Adams

2024/09/24

2

compiled by B Adams

3.1.1

Recognise financial concepts related to personal finances, methods of financing and financial control.

3.1.2

Distinguish between sources of fixed, variable and occasional income:

2024/09/24

compiled by B Adams

3

3.1.3

Distinguish between fixed, variable and occasional expenses.

3.1.3 Advantages and disadvantages of keeping money either in cash or in a bank account

- The importance of saving money for unforeseen payments or expenses

2024/09/24

compiled by B Adams

4

Develop confidence in managing personal finances by recognizing financial concepts related to income, expenses, and financial control. Learn to distinguish between sources of fixed, variable, and occasional income, as well as fixed, variable, and occasional expenses. Understand the advantages of keeping money in a bank account and the importance of saving for unforeseen expenses.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. Download presentation by click this link. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

E N D

Presentation Transcript

L2 MATHEMATICAL LITERACY TOPIC 3 FINANCE LESSON 1 SUBJECT OUTCOME 3.1 Manage finances with confidence in a personal and/or familiar context. 3.1.1 Recognise financial concepts related to personal finances, methods of financing and financial control. Range: (income, expense, fixed income, variable income, fixed expense, variable expense, salary, gross salary, net salary, wage, gifts, pocket money, commission ,rent, maintenance, government grants, entertainment costs, budget, debit card , credit card , bank fees/service fees/transaction fees,) savings account, cheque accounts , cheque book , deposit, balance, stokvels , pension funds , PAYE, UIF, interest , simple interest, compound interest principle amount , interest rate , matshonisa, hire purchase agreement. 2024/09/24 3.1.2 Distinguish between sources of fixed, variable and occasional income: Salaries and wages; commission Gifts and pocket money Bursaries Loans Money from savings accounts Interest received Inheritance Grants Rent received Child support maintenance compiled by B Adams 3.1.3 Distinguish between fixed, variable and occasional expenses. Living expenses (food, haircut, entertainment, clothing, transport costs, child support maintenance, occasional/unforeseen expenses) Accounts to pay (monthly rent, electricity & water, telephone & cell phone) Fees payable (school fees, bank fees) Insurance (car, household and medical fund) Personal taxes Loan repayment/credit card repayments, store account payments Money transfer to a savings account 1 3.1.4 Explain the following: The advantages and disadvantages of keeping money either in cash or in a bank account The importance of saving money for unforeseen payments or expenses

3.1.1 Recognise financial concepts related to personal finances, methods of financing and financial control. 3.1.2 Distinguish between sources of fixed, variable and occasional income: TYPES OF INCOME DESCRIPTION An amount of money received that stays the same from month to month E.g. salary, wages, rental income, government grants, child support maintenance. FIXED INCOME 2024/09/24 An amount of money received that differs from month to month E.g. commission , gratuities, profit from a business, interest earned on an investment VARIABLE INCOME Occasional money received. E.g. birthday money, inheritance, selling your phone. It is also a Variable income (loans, bursaries, gifts, inheritance, UIF) OCCASIONAL INCOME compiled by B Adams Monthly payment a person receives if he/she is employed. It is a fixed income paid directly into the employee s bank account. Sometimes additional benefits such as housing and car allowances is added. SALARY Cost to company is more than the amount that the employee gets at the end of the month. All benefits such as medical aid, UIF, pension fund, etc., as well as PAYE(tax known as Pay-As-You-Earn) must still be deducted. The gross salary is the salary before deductions. GROSS SALARY The amount paid directly into the bank account of employee. The take-home salary . GROSS SALARY DEDUCTIONS = NET SALARY NET SALARY Weekly payment that a person receives who is employed. Usually paid in cash. Wage amount differs slightly from week to week, calculated on a rate system (takes hours worked in consideration) WAGE 2 Salespeople often receive commission on sales and services. If a person receives commission as an income, his income can vary from month to month. Commission is a variable income. COMMISSION Tips earned by waitrons and other service providers. It is a variable income, as it will not always be the same. GRATUITIES

3.1.3 Distinguish between fixed, variable and occasional expenses. EXPENSES DESCRIPTION FIXED EXPENSE An amount paid that stays the same from month to month. E.g. rent, insurance, cellphone contract VARIABLE EXPENSE An amount that changes from month to month e.g. groceries, entertainment, prepaid cellphone OCCASIONAL EXPENSE Money spends occasionally, like buying a birthday present, paying for a car, home repairs or funeral costs. 2024/09/24 compiled by B Adams 3

3.1.3 Advantages and disadvantages of keeping money either in cash or in a bank account - The importance of saving money for unforeseen payments or expenses Why should we save? Advantage and disadvantage of keeping money in either cash or bank account Cheaper to buy an item cash than by paying it off for months and years. 2024/09/24 Good to save for difficult times. You may loose your job or serious illness. Save for unforeseen events and emergencies. compiled by B Adams Good to make provision for your retirement early in life. The sooner you start saving for retirement, the better your retirement years will be. Give you a sense of security and achievement if you manage your live within your means and that you made provision for a rainy day. 4