Financial Management and Objectives

Financial management involves focusing on ratios, equities, debts, and various financial strategies to maximize shareholder value. It also encompasses aspects like capital raising, hedging, and dividend policies. The objectives of financial management include profit maximization, wealth maximization, ensuring company survival, maintaining cash flow, minimizing capital costs, and more. It also includes estimating fund requirements, determining capital structure, and effective investment planning to achieve business goals.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

You are allowed to download the files provided on this website for personal or commercial use, subject to the condition that they are used lawfully. All files are the property of their respective owners.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.

E N D

Presentation Transcript

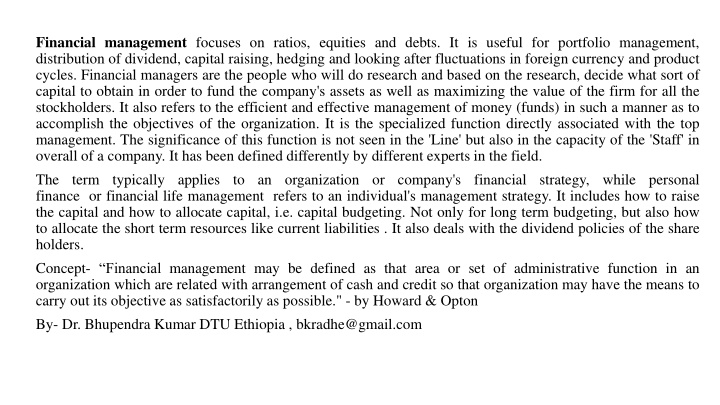

Financial management focuses on ratios, equities and debts. It is useful for portfolio management, distribution of dividend, capital raising, hedging and looking after fluctuations in foreign currency and product cycles. Financial managers are the people who will do research and based on the research, decide what sort of capital to obtain in order to fund the company's assets as well as maximizing the value of the firm for all the stockholders. It also refers to the efficient and effective management of money (funds) in such a manner as to accomplish the objectives of the organization. It is the specialized function directly associated with the top management. The significance of this function is not seen in the 'Line' but also in the capacity of the 'Staff' in overall of a company. It has been defined differently by different experts in the field. The term typically applies to an organization or company's financial strategy, while personal finance or financial life management refers to an individual's management strategy. It includes how to raise the capital and how to allocate capital, i.e. capital budgeting. Not only for long term budgeting, but also how to allocate the short term resources like current liabilities . It also deals with the dividend policies of the share holders. Concept- Financial management may be defined as that area or set of administrative function in an organization which are related with arrangement of cash and credit so that organization may have the means to carry out its objective as satisfactorily as possible." - by Howard & Opton By- Dr. Bhupendra Kumar DTU Ethiopia , bkradhe@gmail.com

Objectives of Financial Management 1. Profit maximization happens when marginal cost is equal to marginal revenue . This is the main objective of Financial Management. 2. Wealth maximization means maximization of shareholders' wealth. It is an advanced goal compared to profit maximization. 3. Survival of company is an important consideration when the financial manager makes any financial decisions. One incorrect decision may lead company to be bankrupt. 4. Maintaining proper cash flow is a short run objective of financial management. It is necessary for operations to pay the day-to-day expenses e.g. raw material, electricity bills, wages, rent etc. A good cash flow ensures the survival of company. 5. Minimization on capital cost in financial management can help operations gain more profit. 6. It is vague :- There are several types of profits before interest, depreciation and taxes, profit before taxes, profit after taxes, cash profit etc.

Scope of Financial Management 1. Estimating the Requirement of Funds: Businesses make forecast on funds needed in both short run and long run, hence, they can improve the efficiency of funding . The estimation is based on the budget e.g. sales budget , production budget . 2. Determining the Capital Structure : Capital structure is how a firm finances its overall operations and growth by using different sources of funds. Once the requirement of funds has estimated, the financial manager should decide the mix of debt and equity and also types of debt. 3. Investment Fund : A good investment plan can bring businesses huge returns. 4. To ascertain maximum profit as well as maintain the core value of the organization

Financing Meaning and Sources of Business Finance Meaning of Business Finance Business Finance is that business activity which is concerned with the acquisition and conservation of capital funds in meeting financial needs and overall objectives of business enterprises. Sources of finance are ways in which a business can get additional funds in order to finance various things. These include start-up, for example raw materials, machinery and buildings; expansion, for example buying more equipment and larger buildings; and to help with cash flow problems, for example in periods when the business is short of cash. The business will have two main categories to choose from. These are internal sources of finance and external sources of finance. Internal Finance = money that comes from inside the business itself. External finance = money which comes from outside the business

Internal Sources of finance Retained Profit = the profit left after all expenses have been paid (including dividends in a plc) Advantages: - It doesn t need to be paid back Disadvantages - The profits of a small business may be too low to be of use A new business won't have any retained profit Sale of Assets = this is when a company sells old assets which it no longer needs Advantages: - Saves space as old assets are no longer there - It makes better use of the business capital Disadvantages: - New businesses won t have any assets to sell - It s time consuming and the business might not find a buyer (especially if the assets are old)

Owners Savings = the owners of the business can use their savings as finance in the business. This is only available to sole traders and partnerships Advantages: - Quickly available - No interest will need to be paid Disadvantages - The owner might not have enough savings - It s very risky due to unlimited liability External Sources of finance Now let s look at external sources of finance. These include: A bank overdraft, a trade credit, a bank load, leasing, hire purchase, mortgages, the issue of shares, debentures, and factoring. Bank Overdraft- this allows the company to spend more money from their account than is actually in it. This is usually used to cover day to day expenses. Advantages: - It s easily arranged and flexible - Cheap as the company only has to pay interest on the amount overdrawn at any one time Disadvantages - The bank can ask for the overdraft to be repaid whenever they want to and with short notice - Cannot be used to finance long term assets - Interest need to be paid

Trade Credit- gives the business around 1-3 months to pay after purchasing supplies Advantages: - No interest - Useful as the company can sell its finished product and sell it before having to pay the suppliers Disadvantages - The supplier may refuse to give discounts or completely stop trade with the business if payments are not met. - Suppliers see smaller, new businesses as unreliable, therefore they might not allow them to pay on credit. Bank Loan - this is where a business borrows money from a bank for a period of 1-10 years. Usually used to buy fixed assets, e.g. machinery and buildings Advantages: - The business can easily plan ahead, as the interest rate is fixed - Large businesses can get lower interest rates as they are more reliable - Good for both long-term and short-term Disadvantages - Small companies will need to pay higher interest rates - Interest need to be paid - Collateral is needed, meaning that if the business fails to repay the loan, the bank will insist that it sells its property. In the case of a sole trader, the owner might lose his/her house or car.

Leasing- this is when a business borrows an asset and uses it in return for monthly payments. This means the company will not have to buy the asset. Advantages: - The company will not have to spend a lot of money on buying the asset - The firm will be able to easily update their equipment - The leasing company will take care of maintenance and replace damaged assets Disadvantages - In the long term, leasing will be more expensive than actually purchasing the equipment Hire Purchase - Allows a firm to pay for an item over a long period of time in the form of monthly payments Advantages: - The business will not have to find a lot of money to buy the item Disadvantages - Interest rates are very high. It may be better to take out a bank loan - A cash deposit needs to be paid at the start Mortgages - long term loans, usually used to buy land or buildings. Payments are made over a period of 25 years. Advantages: - Very long term. Gives the business a long time to repay the money Disadvantages: - If payments are not made the bank will take ownership of the building or land - Interest needs to be paid

Issue of Shares - only available to limited companies. Private limited companies (Ltds) can sell shares to friends and family. Public limited companies (Plc s) can sell shares to the general public. Generally used for expansion and to finance long term assets. Advantages: - Does not have to be repaid - Plc s can rtaise a lot of money this way - No interest - Status and reputation of a company can be raised - Having shareholders increases the financial security of the business, so it will be easier to get bank loans Disadvantages; - Dividends need to be paid to shareholders - Issuing shares takes time and requires lots of paperwork - The company is watched by the public and changes in performance are quickly noticed - Ownership of the company will be complicated and there is the danger of takeovers Debentures - debenture holders lend the company money which will need to be repaid over a long period of time Used to finance long term expansion. Advantages: - Very long term. Up to 25 years Disadvantages - Interest must be paid

Factoring -this is when a company uses another company (debt factor) to collect money which is owed to them by their customers Advantages: - It is immediately available - The risk of collecting the debt is passed onto the debt factor Disadvantages - A percentage of the debt collected will be paid to the debt factor Sources of Long Term Financing: Following are the various sources of long term finance are as follows Shares: These are issued to the general public. The holders of shares are the owners of the business. These may be of two types: Equity shares and Preference shares. Debentures: These are also issued to the general public. The holders of debentures are the creditors of the company. Public Deposits: General public also likes to deposit their savings with a popular and well established company which can pay interest periodically and pay-back the deposit when due. Retained Earnings: The company may not distribute the whole of its profits among its shareholders. It may retain a part of the profits and utilize it as capital.

Term Loans from Banks: Many industrial development banks, cooperative banks and commercial banks grant medium term loans for a period of 3-5 years. Loan from Financial Institutions: There are many specialized financial institutions established by the Central and State governments which give long term loans at reasonable rates of interest. Long Term Financing Products: The following products are provided as part of long term financing services: 1. Debentures 2. Interest Rate Swaps 3. Secured Notes 4. Unsecured Notes 5. Forward Rate Agreements (FRA s) 6. Interest Only Futures 7. Convertible Notes 8. Option on Future Contracts 9. Fixed Deposit Loans 10. Subordinated Debt 11. Mortgages 12. Preference Shares 13. Euro-issues

The money market instruments are amongst the safest forms of investment in the United States because the principals of these forms of investment are assured. The money market instruments are normally provided in the minimum denomination of $1 million. The term periods of the money market instruments could vary from a single day to a year itself. However the most commonly observed term periods are three months or less. The money market instruments are often sold in active secondary markets before they mature. Banker s Acceptance The Banker s Acceptance is a form of money market instrument. It is basically a draft provided by a bank that could be used as a form of payment just like a cashier s check for example. Certificate of Deposit These are time deposits, in banks, that have a fixed date of maturity. The certificates of deposit that have comparatively bigger denominations are eligible to be sold off prior to maturity. Repurchase Agreements The Repurchase Agreements are primarily subscribed by government securities and are essentially short-term notes. These have term periods not exceeding two weeks. Quite often the holder of securities sells them to investors after which they agree on either a specified rate or date at which the securities may be bought back. Forward Rate Agreement is a version of over-the counter derivatives that are designed to meet certain requirements. It is a kind of agreement where two parties are involved and through this agreement these parties fix a forward interest rate. This forward interest rate is applicable to a pre-decided speculative amount of money, which may be a loan or any kind of deposit amount. The time limit in this type of contract is always pre-decided. A combination of Forward Rate Agreements is called swap. Forward Rate Agreement is mainly used by the banking institutions for different purposes. At the same time, financial activities that are related to high risk also use the Forward Rate Agreement to reduce the risk factors. Convertible bonds are essentially corporate bonds that could be converted by the bondholder into common stock or shares of the issuing company. These bonds give the bond holder the option to exchange the bond for a predetermined and mutually agreed amount of equity stock of the issuing company.

Investment decisions Investment decisions are made by investors and investment managers. Investors commonly perform investment analysis by making use of fundamental analysis, technical analysis and gut feel. Investment decisions are often supported by decision tools. The portfolio theory is often applied to help the investor achieve a satisfactory return compared to the risk taken. Capital budgeting, and investment appraisal, is the planning process used to determine whether an organization's long term investments such as new machinery, replacement of machinery, new plants, new products, and research development projects are worth the funding of cash through the firm's capitalization structure (debt, equity or retained earnings). It is the process of allocating resources for major capital , or investment, expenditures. One of the primary goals of capital budgeting investments is to increase the value of the firm to the shareholders. Many formal methods are used in capital budgeting, including the techniques such as 1. Accounting rate of return 2. Average accounting return 3. Payback period 4. Net present value 5. Profitability index 6. Internal rate of return 7. Modified internal rate of return 8. XIRR 9. Real options valuation

Net Present value (NPV)- Cash flows are discounted at the cost of capital to give the net present value (NPV) added to the firm. Unless capital is constrained, or there are dependencies between projects, in order to maximize the value added to the firm, the firm would accept all projects with positive NPV. This method accounts for the time value of money . For the mechanics of the valuation here, see Valuation using discounted cash flows . Mutually exclusive projects are a set of projects from which at most one will be accepted, for example, a set of projects which accomplish the same task. Thus when choosing between mutually exclusive projects, more than one of the projects may satisfy the capital budgeting criterion, but only one project can be accepted. The internal rate of return (IRR) is the discount rate that gives a net present value (NPV) of zero. It is a widely used measure of investment efficiency. To maximize return, sort projects in order of IRR. Many projects have a simple cash flow structure, with a negative cash flow at the start, and subsequent cash flows are positive. In such a case, if the IRR is greater than the cost of capital, the NPV is positive, so for non-mutually exclusive projects in an unconstrained environment, applying this criterion will result in the same decision as the NPV method. An example of a project with cash flows which do not conform to this pattern is a loan, consisting of a positive cash flow at the beginning, followed by negative cash flows later. The greater the IRR of the loan, the higher the rate the borrower must pay, so clearly, a lower IRR is preferable in this case. Any such loan with IRR less than the cost of capital has a positive NPV. Excluding such cases, for investment projects, where the pattern of cash flows is such that the higher the IRR, the higher the NPV, for mutually exclusive projects, the decision rule of taking the project with the highest IRR will maximize the return, but it may select a project with a lower NPV. Real options analysis has become important since the 1970s as option pricing models have gotten more sophisticated. The discounted cash flow methods essentially value projects as if they were risky bonds, with the promised cash flows known. But managers will have many choices of how to increase future cash inflows, or to decrease future cash outflows. In other words, managers get to manage the projects - not simply accept or reject them. Real options analysis tries to value the choices - the option value - that the managers will have in the future and adds these values to the NPV .

Dividend Decisions- A dividend is a payment made by a corporation of profits. When a corporation earns a profit or surplus, the corporation is able to re-invest the profit in the business (called retained earnings) and pay a proportion of the profit as a dividend to shareholders. Distribution to shareholders may be in cash (usually a deposit into a bank account) or, if the corporation has a dividend reinvestment plan , the amount can be paid by the issue of further shares or share repurchase . When dividends are paid, shareholders typically must pay income taxes, and the corporation does not receive a corporate income tax deduction for the dividend payments. to its shareholders , usually as a distribution A dividend is allocated as a fixed amount per share with shareholders receiving a dividend in proportion to their shareholding. Dividends can provide stable income and raise morale among shareholders. For the joint- stock company , paying dividends is not an expense ; rather, it is the division of after-tax profits among shareholders. Retained earnings (profits that have not been distributed as dividends) are shown in the shareholders' equity section on the company's balance sheet the same as its issued share capital. Public companies usually pay dividends on a fixed schedule, but may declare a dividend at any time, sometimes called a special dividend to distinguish it from the fixed schedule dividends. Cooperatives , on the other hand, allocate dividends according to members' activity, so their dividends are often considered to be a pre- tax expense. The word "dividend" comes from the Latin word "dividendum" ("thing to be divided")

Dividend Policies 1-Relevance of dividend policy I. Walter's model II. Gordon's Model III. Lintner's Model IV. Capital structure substitution theory & dividends 2- Irrelevance of dividend policy I. Residuals theory of dividends II. Modigliani-Miller theorem Relevance Dividend Model- Dividends paid by the firms are viewed positively both by the investors and the firms. The firms which do not pay dividends are rated in oppositely by investors thus affecting the share price. The people who support relevance of dividends clearly state that regular dividends reduce uncertainty of the shareholders i.e. the earnings of the firm is discounted at a lower rate, kethereby increasing the market value. However, its exactly opposite in the case of increased uncertainty due to non-payment of dividends. Irrelevance Dividend Model- The Modigliani and Miller school of thought believes that investors do not state any preference between current dividends and capital gains. They say that dividend policy is irrelevant and is not deterministic of the market value. Therefore, the shareholders are indifferent between the two types of dividends. All they want are high returns either in the form of dividends or in the form of re-investment of retained earnings by the firm. There are two conditions discussed in relation to this approach : decisions regarding financing and investments are made and do not change with respect to the amounts of dividends received. when an investor buys and sells shares without facing any transaction costs and firms issue shares without facing any floatation cost, it is termed as a perfect capital market. Two important theories discussed relating to the irrelevance approach, the residuals theory and the Modigliani and Miller approach.

Working Capital Decisions - Working capital (abbreviated WC) is a financial metric which represents operating liquidity available to a business, organisation or other entity, including governmental entities. Along with fixed assets such as plant and equipment, working capital is considered a part of operating capital. Gross working capital is equal to current assets. Working capital is calculated as current assets minus current liabilities . If current assets are less than current liabilities, an entity has a working capital deficiency, also called a working capital deficit. A company can be endowed with assets and profitability but may fall short of liquidity if its assets cannot be readily converted into cash. Positive working capital is required to ensure that a firm is able to continue its operations and that it has sufficient funds to satisfy both maturing short-term debt and upcoming operational expenses. The management of working capital involves managing inventories, accounts receivable and payable, and cash. NWC=CA-CL Current assets and current liabilities include four accounts which are of special importance. These accounts represent the areas of the business where managers have the most direct impact: 1. cash and cash equivalents (current asset) 2. accounts receivable (current asset) 3. Inventory (current asset), and 4. accounts payable (current liability) The current portion of debt (payable within 12 months) is critical because it represents a short-term claim to current assets and is often secured by long-term assets. Common types of short-term debt are bank loans and lines of credit. An increase in net working capital indicates that the business has either increased current assets (that it has increased its receivables or other current assets) or has decreased current liabilities for example has paid off some short-term creditors, or a combination of both.

- Cash flows are discounted at the")