Financial Figures and Analysis

undefined

undefined

Joseph L. Petrelli, ACAS, MAAA

President & Co-Founder, Demotech, Inc.

Buckeye Actuarial Continuing Education

Inaugural Meeting, April 26, 2011

2

3

4

5

6

7

8

9

10

11

12

13

14

Title insurance rates vary by state. The premium is typically

determined based upon a rate per thousand dollars of

exposure. The one-time premium covers the parties as long

as they have an insurable interest in the real property. A

limited number of states have Title insurance rating bureaus.

The majority of states do not.

15

Escrow and settlement services are defined as part of the

Title insurance process in some states and specifically

excluded from Title insurance in others. Typically, premiums

are regulated by the states but fees and work charges are not

regulated.

16

The basic Title insurance products are an Owner’s policy or a

Loan policy. Although there are approximately thirty

endorsements available to expand coverage, in some states

there is a premium associated with the endorsements and in

other states the endorsements can be requested at no charge.

17

Policies, forms and endorsements are promulgated but not

filed by the American Land Title Association. Each state has a

land title association that represents the interests of the local

agents and domestic Title underwriters. Licensing

requirements including continuing education requirements

vary by state.

18

The overwhelming majority of the items that can adversely

impact the marketability of Title to real property are

discovered, addressed and resolved prior to policy issuance.

As Title insurance coverage is retrospective and not

prospective, it is my opinion that the financial reporting

practices in place today cannot measure the value proposition

of Title insurance. From a property and casualty insurance

perspective, a Title insurance policy is more like a closed

claim file than it is a P&C policy.

19

In 1994, the Federal National Mortgage Association issued

Bulletin 94-13. This bulletin simplified the process for

identifying acceptable title insurance companies and to

minimize the potential for losses related to the type of

coverage or the financial strength of the title insurer. Other

participants in the secondary mortgage marketplace imposed

similar requirements.

20

While Title insurance coverage looks backward from a

certain date, P&C insurance coverage looks forward,

utilizing a finite future period, to evaluate liability. The

timeframe of coverage and cost containment activities are

a fundamental difference between Title and P&C

coverages.

This distinction for Title underwriters has not been

properly reflected in financial reporting requirements nor

statistical reporting requirements.

21

Subject to the exclusions from coverage, the exceptions

from coverage contained in Schedule B and the conditions

and stipulations, the Title insurance company,

as of the

Date of Policy

shown in Schedule A, against loss or

damage…

Coverage is Retrospective.

22

In Consideration of the Provisions and Stipulations herein,

the Property and Casualty Insurance Company, for the

term of

this date

at 12:01 a.m. to

one year later

at 12:01

a.m. at the location of the property involved, does insure…

Coverage is Prospective.

23

Title is Retrospective

Incident must have occurred

prior to policy date to be

considered covered

P & C is Prospective

Incident must occur within

policy period to be

considered covered

D

a

t

e

o

f

P

o

l

i

c

y

D

a

t

e

o

f

P

o

l

i

c

y

24

Loss adjustment expenses include allocated loss adjustment expenses

and unallocated loss adjustment expenses.

Allocated loss adjustment expenses are those expenses, such as

attorneys’ fees and other legal costs, that are incurred in connection

with and assigned to specific claims.

Unallocated loss adjustment expenses are all other claim adjustment

expenses and include salaries, utilities and rent apportioned to

support the claim adjustment function although not readily assignable

to any specific claim.

25

Access Denied

Access Denied

This motel was landlocked after a neighbor’s foreclosure.

This motel was landlocked after a neighbor’s foreclosure.

Bumped and Stumped

Bumped and Stumped

Was it too much to ask that the mortgage be recorded?

Was it too much to ask that the mortgage be recorded?

Partnership Pie

Partnership Pie

The managing partner knew to manage for himself.

The managing partner knew to manage for himself.

26

Located on Interstate 40 (old Route 66), at midpoint of the long haul between Oklahoma City

and Amarillo, is the Highway 8 Motel at Elk City.

For many years business flourished. When the owner was tired of turning away travelers, he

bought more land behind the motel and built an addition. Construction was paid for by a

new loan secured by a deed of trust against the rear lot.

27

The motel’s success did not go unnoticed. Others bought land across the interstate, and soon

a new Holiday Inn appeared, then an Econo-Lodge.

Business fell off at the old Highway 8. When the owner fell behind in payments, his lenders

foreclosed.

The lender on the rear lot was in for unpleasant news. There was no right of access

anywhere to connect it with a public road, and the lender on the frontage lot would no longer

allow it to be used to access the rear. Who, after all, needs competition?

Following litigation over the true amount of its damages, the insured lender received about

$83,000 from the title company.

28

Title insurance includes coverage for a right of access. This coverage is included in all owner,

loan and leasehold policies.

Any prospective insured wanting a specific right-of-way should be careful to make sure that

the same is expressly insured by the policy to be issued. Otherwise, the insured may be

surprised to learn that the desired right-of-way cannot be used, and instead, access is

allowed by some less desirable way.

29

After closing a $1.6 million construction loan on this apartment project in South Philly, the

closing agent made the most serious of mistakes: he forgot to record the mortgage.

By the time the mistake was discovered, the developer was in serious trouble, with 24 tax

and judgment liens filed against him totaling more than $800,000 in liabilities.

When the insured lender began foreclosure, they learned that because of the recording snafu

their priority was bumped from 1

st

to 25

th

!

30

It only got worse. Before the original mortgage could be located (it was in the agent’s file),

the developer filed bankruptcy.

Now the trustee in bankruptcy threatened to void the insured mortgage altogether using

section 544(a)(3) of the Bankruptcy Code. That section permits a trustee in bankruptcy (or a

debtor-in-possession) to avoid any interest in real property which is not perfected (in this

case, by recording) as of the date of commencement of bankruptcy.

However, because the mortgage was only partially funded, and thanks to contribution from

the agent’s errors and omissions insurance carrier, First American’s loss was limited to

$55,000.

31

Whenever an interest in real property is not perfected by recording, three things can wipe

out the interest:

1.

The grantor may sell or mortgage the property to another (bona fide

purchaser/encumbrancer) without disclosing the unperfected interest;

2.

Intervening liens or encumbrances may be recorded, gaining priority; or

3.

The grantor may go into bankruptcy, whereupon the trustee avoiding power (Bankruptcy

Code section 544 (a)(3)) may be invoked to avoid the interest as against the debtor’s real

property.

32

It seemed like a great opportunity, a limited partnership owning this luxury home on a bluff

overlooking the Pacific. This property had it all: 11,000 square feet of living space, a swimming

pool, tennis courts and panoramic view of Malibu’s beaches.

In all, 15 limited partnership shares were offered to investors throughout Los Angeles. After

renovation, the home would be put on the market for $6 million. Who cared if it didn’t sell?

Sooner or later the market would have to catch up.

So it was one evening as two of the partners watched “Lifestyles of the Rich and Famous” on

television. Something Robin Leach was saying, something about “Malibu” and “the man with the

Midas touch,” caught their attention.

There on screen was their managing partner. “The young multi-millionaire,” gushed Leache, “who

sees opportunities and seizes them.”

But wait! Now on screen was their house, their investment, “his magnificent mansion that serves

as international headquarters!” It was unmistakable. “It had all the wood From the old Vanderbilt

Mansion on Long Island,” bragged the general partner.

33

The partners investigated. Soon they learned that their general partner, using his broad

powers under their limited partnership agreement, had deeded the property to himself.

Then he borrowed $2.3 million from an unsuspecting bank, secured by a deed of trust

against the property. While some of this money was used to retire partnership debts, the rest

(about $900,000) disappeared in the general partner’s personal accounts.

Tricked out of their shoes, the partners got together and filed suit to get the property back

and avoid the deed of trust. Their attorneys would claim that the deed of trust was

unauthorized, not given for “partnership purpose.”

The deed of trust was insured by First American. The Company hired lawyers to represent

the lender’s interests. Dozens of depositions were taken. After a trial lasting several weeks,

the judge ruled in favor of the lender. He concluded the partners had given the general

partner such broad authority that the lender was justified in dealing with him solely.

After recouping court-awarded costs, First American paid legal expenses of $365,280.

34

In every real estate transaction, the title company must be satisfied that parties involved are

mentally competent or, where a business entity is involved, legally authorized to act.

Where partnerships are involved, the title examiner should review the partnership

agreement to see that the person with whom he or she is dealing has authority to contract on

behalf of the partnership, and that this authority is broad enough to include the transaction

at hand. Frequently, partnership agreements provide that there be no sale, lease or

mortgaging of partnership property without the vote or consent of a majority of partners.

This basic risk of incompetency, incapacity or lack of authority of parties is typically covered

by insurance.

35

Access ‘To Come’

Access ‘To Come’

Please, Mr. Postman – The lament of the landlocked.

Please, Mr. Postman – The lament of the landlocked.

First Name First

First Name First

ABC’s of searching records.

ABC’s of searching records.

NSF

NSF

Some bad advice, a bad check and two former partners.

Some bad advice, a bad check and two former partners.

36

Plans called for this retirement and convalescent facility to have two driveways.

Set back from March Lane, a busy thoroughfare, the facility was to have access both to March

Lane and to a nearby side street. The neighbor who owned the surrounding property

agreed; it was a done deal.

The developer was anxious to get started, but the escrow officer had yet to receive easement

deeds from the holder of the neighbor’s mortgage, a savings and loan association.

Yielding to the developer’s wishes, escrow was closed with easement deeds to be received

and recorded later.

The deeds failed to arrive and were eventually forgotten about… Details.

37

Meanwhile, the neighbor lost his land through foreclosure, and it was acquired by the

foreclosing S&L. Then the foreclosing S&L failed and was taken over by FSLIC.

FSLIC inspected the land and told the developer to forget about getting any easements, even

though one concrete driveway was already in place. FSLIC threatened to tear it up.

First American hired a lawyer to represent the insured owner and lender, and peace was

made with FSLIC.

The Company paid $35,000 for confirmation of an easement where the concrete driveway is

located, and in the process incurred legal expenses of $10,000.

38

Real estate transactions are frequently closed with needed documents promised, but not in

hand. This is most often the case with releases or ‘satisfactions’ of paid-off mortgages or

liens.

This practice is approved by title companies, and they are willing to insure against paid-off

items. When this practice is followed, the escrow or closing officer should have written

evidence of the paid-off party’s agreement to provide a written release by return mail.

On the other hand, where a promised document directly affects immediate rights of use and

possession, such as a deed or easement deed, it is too important to go without. Any death,

displacement, disability or bankruptcy of the party giving a verbal promise can render the

promise useless.

39

This tale begins with foreclosure of this retail store space to satisfy an unpaid mortgage.

Four years later, John was served with a lawsuit filed by Joyce, whom John had never heard

of, seeking to foreclose a ten year-old mortgage, which also John had never heard of. The

unpaid balance of the mortgage was said to be more than $100,000.

The successful bidder was John, who after the foreclosure wisely obtained an owner’s policy

of title insurance from an agent of First American. This policy insured the property free and

clear of any mortgages or liens. John called the title agent … here’s what we learned.

The property was formerly owned by a corporation named “Anita Lee Gift Shop, Inc.” This

corporation was owned by William and Joyce, who were husband and wife. When the couple

split, William took over the gift shop and promised to pay Joyce $120,000, in monthly

installments of $1,000 for ten years. This promise was secured by the aforementioned

mortgage, in favor of Joyce, which was duly recorded in Camden County land records.

40

Later, William gave a second mortgage to a financial institution, which was the same

mortgage that was later foreclosed resulting in the ownership of our insured, John.

In searching the records prior to issuing our policy to John, the searcher checked the

recorder’s alphabetical index for “Lee, Anita” rather than “Anita Lee,” and so missed the

mortgage in favor of Joyce.

More bad news … William had made almost none of his mortgage payments, so the balance

now due Joyce was equal to the value of the property. This was a total ‘failure of title.’

First American paid $116,875 to satisfy the missed mortgage.

41

The protocol for posting, indexing and searching proper names of individuals is “last name

first, first name last.” This rule doesn’t apply to corporations, whose names should be listed

under the first letter of the name as registered with the state of incorporation.

This rule is sometimes misunderstood by county employees who do indexing or “posting,”

and is also misunderstood by title searchers. Experienced searchers know to check every

conceivable variation of a name under search.

42

The uptown shopping center was owned by the partnership of John and Ron. The managing

partner was John.

One January 31

st

the partnership sent a check for $385,616 to the county tax assessor for

second installment property taxes. This check was drawn on the account of Riverfront Plaza

Property Management, a company owned solely by John.

When they received the check, the office of the tax assessor made a record that the taxes had

been paid – but then the check bounced (“NSF – Refer to Maker”).

Meanwhile, John decided to sell his interest in the partnership. A First American agent was

asked to handle the transfer of ownership to a new partnership. The closing officer checked

for property taxes and received from the Cook County Clerk a “Certificate of Payment,” dated

April 1, showing second installment taxes as paid. The transfer of ownership closed a few

days later, and a First American owner’s policy was issued with no exception for past-due

taxes.

43

After the closing, former partners John and Ron held a post-closing reconciliation meeting in

which they settled business matters between themselves and signed mutual releases.

More than a year later, First American was notified that the old “second installment” taxes

remained unpaid and now stood as a lien against the property in the amount of $499,552,

including penalties and interest.

When first contacted, neither of the former partners seemed interested in the problem. One

put us off for months saying through his lawyer that the taxes had been paid or, perhaps, an

account was established somewhere to cover them.

Lawsuits were filed and, after months of wrangling, the former partners settled with John

agreeing to pay the taxes. First American continues to pursue John to recover its legal

expenses, totaling more than $340,000.

44

Title insurance is your best protection against ineffective payoffs at the time of closing –

such as resulting from a bad check.

45

Breach of Trust

Breach of Trust

Money to pay off mortgages was missing.

Money to pay off mortgages was missing.

Masquerade

Masquerade

When he tried to take possession, the buyer got a surprise.

When he tried to take possession, the buyer got a surprise.

Power of Attorney

Power of Attorney

Title “stolen” through fake authority.

Title “stolen” through fake authority.

46

Thomas M. Dameron was a successful attorney with a hand in several companies offering

title and settlement services in Northern Virginia. One of these companies, Mid-Atlantic Title

& Escrow Services, was an authorized agent of First American.

Dameron got interested in developing a shopping center and waste treatment plat at Inwood,

West Virginia. Rather than borrowing money to finance these projects, he began diverting

funds provided to pay off mortgages in connection with property sales and refinancings

handled by his Virginia-based companies. (Defalcation)

To conceal these diversions Dameron continued monthly payments on mortgages which

should have been paid off, and he routinely issued title policies to new owners and lenders as

if the old mortgages were released.

Obviously, this sort of thing can get out of hand. Every month Dameron had to take more and

more money to keep things quiet.

But that wasn’t what stopped him.

47

Things started to unravel around January when lenders mailed IRS 1099 forms to Dameron’s

clients, showing their mortgage interest payments for the past year. Several clients were

surprised at the numbers on their 1099’s. They investigated and wrote letters to the State

Bar. Dameron was caught.

He was arrested and pleaded guilty to federal charges of bank years. His seven-month spree

saw misappropriations totaling about $4 million.

With Dameron in the pokey, mortgage payments stopped and lenders began to foreclose. In

all, 24 homeowners made claims under First American policies or commitments, and the

Company paid a total of $2,564,304 to clear up their titles. The Company also paid

accounting and legal expenses of $491,296.

48

First American offers title insurance through thousands of independent company and

attorney agents throughout the United States. The Company’s goal is to affiliate only with

the most competent and ethical agents in the business. And, First American has a large staff

of agency representatives trained to do field audits and spot problems and help agents avoid

trouble.

But occasionally an agent can go wrong. When it happens, the homeowner’s best protection

is an owner’s policy of title insurance.

49

When First American handled the sale of this property, insuring a new owner and lender,

there were clues that something was wrong.

First, the sale was for a bargain price and to be “confidential” so not to upset the tenants in

six rentals on the property.

Second, in checking public records, the examiner encountered an eleven year-old probate

opened for a decedent whose name was identical to the name of our seller, Anna “X.” Even

though the name was uncommon, the examiner disregarded the probate – and didn’t bother

to review the courthouse file – assuming it was a “coincidence.”

Third, when our seller appeared to sign the deed she had no identification in the name of

Anna X. Instead, her driver’s license bore the name “Patricia Anna McGinnis.” She explained

that since acquiring the property seventeen years earlier she went through a divorce and

changed her name. The escrow officer believer her, and notarized the deed signed by

Patricia as “Anna X.”

50

When the insured owner tried to take possession of the property, he was turned away by the angry

son of Anna X, who claimed to be the true owner under his mother’s will, which was still in

probate.

Then the escrow officer mailed her a check for sale proceeds of $90,448, payable to Dean Witter,

“Credit of: Patricia Anna McGinnis.”

It turned out the real Anna X had died twelve years earlier, leaving the property to her son.

However, Anna must have been concerned about the son’s management of his finances, for she

directed by her will that the property be held in trust, for his benefit, until he reached the age of 45,

at which time it would be transferred to his name. This is called a “Spendthrift Trust.” The son was

now 44.

So, the “seller” was an impostor. First American paid the loan policy amount of $150,000, which

was slightly greater than the purchase price, and hired a private investigator to find the impostor.

The investigator concluded that the impostor was the son’s ex-wife, whom he had divorced around

the time his mother died. Her trail led to Port Isabel, Texas, where she was last seen driving a

champagne-colored Cadillac.

51

Obviously, anyone knowing of all these clues would have checked the probate file, and

prevented the forgery. But the escrow officer didn’t talk to the examiner about the

identification issue, and the examiner didn’t talk to the escrow officer about the probate – so

no one put the pieces together.

52

A power of attorney is a legal document by which a person, “the grantor”, authorizes another, the

“attorney-in-fact”, to make decisions or contract for the grantor.

This home is a suburb of Washington, D.C. was owned by a mother and daughter who were

Korean citizens living in Japan. The home was occupied by Sung-Joon, also known as “Alex”, a son

and brother of the owners.

When Alex’s business investments soured he arranged, through a mortgage broker, to borrow

$40,000 secured by a third deed of trust against the home.

To enable himself to sign loan documents without his mother or sister’s knowledge, Alex forged

powers of attorney containing their falsified signatures making him their attorney-in-fact. He

next signed a deed from his mother and sister into his mother, sister and himself (relying on the

forged powers of attorney) – and then signed the $40,000 deed of trust on behalf of his mother

and sister (again relying on the forged powers of attorney) as well as himself.

All of this paperwork must have looked pretty impressive, but in truth it wasn’t worth the price of

postage to mail it across the street.

53

The $40,000 deed of trust was insured by an agent of First American. Apparently the agent

was satisfied with the explanation that powers of attorney were used because Alex’s co-

owners were in Japan.

When the loan fell delinquent, the lender got a letter from an attorney for the mother and

sister claiming the insured deed of trust was a fraud.

First American hired lawyers to investigate – and the forgeries were confirmed. The

Company paid its insured lender $40,000, and incurred legal expenses topping $17,000.

Meanwhile, Alex was arrested and he named an accomplice. The two of them faced criminal

charges, with Alex looking at deportation in the bargain.

First American was not the biggest loser here. It turned out there was a second deed of trust,

for $239,000, made using the same scheme. A different lender, perhaps insured by some

other title company, faced that loss.

54

Lots of lessons here:

First, title examiners are cautioned against relying too heavily on power of attorney where

the attorney-in-fact is benefitted by use of the power. It’s a built-in conflict of interest. It

should cause the examiner to give the transaction careful scrutiny.

Second, an examiner should always want to know why a power of attorney is being used.

Why is the grantor unavailable? If the grantor is in another state or a foreign country, it may

be better to have documents signed there and notarized by an out-of-state notary or at a U.S.

Embassy.

Third, if the reason given for the power of attorney is that the grantor is sick or incapacitated,

the examiner should look to see whether the power of attorney is of the “durable” type – that

is, whether it authorizes the attorney-in-fact to act while the grantor is incapacitated. And,

the examiner should also be satisfied the grantor was mentally competent at the time the

power was signed.

Finally, if the grantor is deceased, a power of attorney shouldn’t be relied on. Any real

property in a grantor’s estate after death should pass through probate.

55

Holding the Bag

Holding the Bag

An old credit line – rises again!

An old credit line – rises again!

Switcheroo

Switcheroo

Paying off the wrong loan.

Paying off the wrong loan.

The Pirated Payoff

The Pirated Payoff

When this home was refinanced the owner saw his ship come in.

When this home was refinanced the owner saw his ship come in.

56

When our title agent was asked to handle a purchase of this home, there was one mortgage

to be paid off through closing.

The mortgage secured a bank line of credit, which the seller had mainly to finance his

businesses. The credit limit was $450,000.

Before closing, the seller went to the bank and told them he was selling his home, but wanted

to keep his line of credit open and would provide substitute collateral. The bank agreed, and

the seller instructed the closing officer to disburse net sale proceeds of $414,987 to the bank.

The closing officer called the bank, getting verbal confirmation the bank would be releasing

its mortgage. The transaction closed, the payment was made to the bank and title policies

were issued to the new owners and lender including coverage against the ‘old’ mortgage.

57

Two years later, when the new owners applied for a loan, they were told the old mortgage

remained “open” – still affecting their home. So they contacted our agent.

The agent contacted the bank, and was told that the credit line now had a balance due of

more than $300,000 – and the seller was delinquent.

Our investigation showed that the seller had offered the bank substitute collateral, but it was

turned down. At the same time, the bank continued to allow the seller to draw funds from

the original credit line. Now, a new bank officer in charge didn’t know anything about a

promise to release the mortgage – and they wanted to be paid.

Ultimately, First American paid $50,000 to the bank for a release of the credit line mortgage.

58

In most parts of the country, it’s customary to close real estate transactions with releases “to

come” for paid-off mortgages and liens.

Where these customs prevail, the risk that a secured credit line will not be closed – but

merely paid “down” and later re-accessed by the borrower – is substantial.

Title insurance is your best protection against this risk.

59

One risk of buying property is that funds to pay off a prior mortgage may get misallocated.

A First American title agent was asked to handle a purchase of this home on University

Boulevard in Denver. The home had an existing mortgage in the original amount of

$138,500. The seller, Charlie, was in the business of buying neglected properties, fixing them

up, and re-selling them.

The escrow officer sent a fax to Charlie asking for “payoff info for the house on University.”

Soon, Charlie called in and provided a loan number. The escrow officer contacted the lender,

referenced the loan number, and requested a payoff demand. The lender sent a fax to the

escrow officer, referencing the loan number, and giving the payoff figure of $138,408.

60

Unfortunately, no one noticed that this payoff demand also referenced a “Property Address”

on “Granby Street.”

The transaction closed, the payoff check was mailed, and First American’s title policy was

issued to the new lender.

Here’s the problem: The “old” lender applied the payoff check to satisfy a mortgage against

another property owned by Charlie – his residence, actually. When Charlie realized his

residence was free and clear, he sold it – pocketing substantial sale proceeds – and moved

with his family to San Diego.

We paid $151,724 for a release of the “old” mortgage against the home on University.

A year and a half and legal expenses later, Charlie agreed to reimburse all but about $25,000

of our losses.

61

There’s lots of opportunity for error in handling payoffs. Title insurance protects against the

risk that a payoff was not received and properly applied to clear secured debts.

62

First American insured a refinancing of this residence for $107,800.

Weeks before funding the closing agent mailed a request for payoff information to the

existing lender. There was no immediate reply.

On the eve of closing a secretary called the lender and took down the following payoff

demand:

“Per Audrey at Central File $44,591.81 – payoff as of 7/27 - $14.57 per diem – (loan

number) 50011200017.”

After closing, the payoff check was sent with a request that the canceled mortgage be

forwarded by return mail.

Months later First American was contacted by its insured lender. It seems the borrower had

two mortgages with the prior lender, one against his home and the other against his boat.

When the payoff check was received the lender canceled the boat mortgage and sent boat

title documents to the borrower.

63

The borrower made a few more home mortgage payments, then abruptly moved out of his

house, abandoned his business and sailed away on his free-and-clear boat.

First American hired attorneys to file suit for judicial foreclosure, and for a declaration of

priority over the prior lender. But the judge ruled for the prior lender, concluding they were

without fault and shouldn’t bear the loss.

First American paid $62,927 to satisfy the offending mortgage, plus legal expenses of

$18,032.

The borrower’s whereabouts remain unknown.

64

Although not a favored practice, real estate transactions are sometimes closed based on

verbal instructions or payoff demands.

When this is done, the opportunities for misunderstandings are limitless. The better practice

is to get all instructions and demands in writing, with all essential understandings spelled

out.

65

A Life Estate

A Life Estate

Foreclosure on hold, indefinitely.

Foreclosure on hold, indefinitely.

Blind Spot

Blind Spot

Unreleased mortgages were thought paid off.

Unreleased mortgages were thought paid off.

Insuring the ‘Gap’

Insuring the ‘Gap’

Owners cash out equity, just ahead of the IRS.

Owners cash out equity, just ahead of the IRS.

66

This home on 37 acres is just north of Colonial Williamsburg.

The owners of record were Bruce and Gracie, who borrowed $60,000 secured by a deed of

trust against the property.

In researching the title, our agent learned that Bruce and Gracie acquired the property six

years earlier by gift deed from a Mrs. Graves. There was a first deed of trust for $7,956

recorded six months earlier, and now the $60,000 deed of trust would be insured as a second

by First American.

More than a year later, the insured deed of trust was in default and the lender hired a local

attorney to do a foreclosure. But the attorney reported the property was still occupied by

Mrs. Graves, who claimed to own a “life estate.” A what?

67

Many different estates or interests in land were recognized by English common law, which is the

main origin of American law. Among these, the most commonly seen today are the free estate

(absolute ownership by a person and his heirs and assigns forever), the leasehold estate (a

tenancy with the owner of the fee as landlord), and the life estate (an interest akin to ownership

for the duration of the life of the holder, or of some other person).

The insured lender made a claim and First American investigated. Sure enough, there in the gift

deed from Mrs. Graves to Bruce and Gracie, on page two following all the boilerplate “less and

except,” “together with” and “subject to” language, there was this:

“There is specifically reserved by the grantor herein the right to reside on, use and occupy the

property herein conveyed for the rest of her natural life …”

So there it was. Because of this, the lender can presently foreclose only the remainder interest of

Bruce and Gracie. They can’t disturb Mr. Graves’ use of the property as long as she lives. We

won’t reveal her age, but Mrs. Graves reports excellent health and a family history of longevity.

First American paid $60,664 to purchase the insured deed of trust.

68

Interests created by “reservation”, buried within a document – and not disclosed by its title,

are more frequently missed by title searchers and examiners than are interests created by

direct grant.

69

When this home was being refinanced, our attorney agent was told there was only one existing

mortgage to be paid off. But the agent’s search disclosed two more mortgages, both in favor of

Georgia Mortgage Center, which were prior to the existing mortgage and were still “open” –

unreleased – in the public records.

The last transaction involving this property had been a refinancing done six months earlier. The

agent called the law firm that handled the previous closing, and was told that both Georgia

Mortgage Center mortgages had not been received for recording. The law firm provided copies of

its settlement statement and cancelled check evidencing the payoffs.

With this evidence in hand, the agent was authorized to insure the pending refinancing without

exception for the Georgia Mortgage Center mortgage. At closing, the agent paid off the existing

mortgage, disbursed about $30,000 to the borrower, Herbert, and insured the new “first”

mortgage.

Cookie-cutter deal. But this closing would be haunted by the unforeseen.

70

The Georgia Mortgage Center mortgages had secured one loan in the amount of $69,000, and

a second in the amount of $81,000. Shortly after these loans were made, the $81,000 loan

(and mortgage) was purchased by an investor. Since no notice of assignment was recorded,

there was no way for anyone to know of the investor’s purchase of the $81,000 mortgage

from an inspection of the public records.

You can probably see where this is headed. When the property was first refinanced, the law

firm was given a payoff figure for the $69,000 mortgage only. No one told them about the

$81,000 mortgage being owned by an investor, so the information later given to our agent

was erroneous. The $81,000 mortgage remained “open.”

Herbert stopped making payments and the $81,000 mortgage foreclosed, wiping out our

insured lender’s mortgage.

The lender made a claim, and First American paid $193,084 to purchase our insured’s note

and foreclosed-out mortgage.

71

It frequently happens that open mortgages or deeds of trust have been satisfied, but paid-off

lenders do not cooperate by providing release documents for recording. In such cases it’s

common for title companies to rely on third parties for evidence of payoff, as was done here.

But this practice isn’t foolproof. When the unforeseen becomes a problem, title insurance

can be an owner or lender’s salvation.

72

When Gary left his employment at the Rocky Flats plutonium plant he received severance

pay of $270,000.

Some of the money was used to buy this home for Gary and his new wife, Diane. The rest

may have been used to pay debts from Gary’s former marriage. None of it, however, went to

the Internal Revenue Service.

Months later, Gary and Diane applied to refinance their home. The new loan amount would

be $98,000. After paying off the existing loan and costs of refinancing, Gary and Diane would

receive about $30,000.

The loan documents were signed on Monday, November 8. The three-day recission period,

provided by federal law, would have expired at midnight on Thursday, November 11. But

November 11 was Veterans Day, a holiday, so the rescission period expired at midnight on

Friday, November 12.

73

The lender would have funded the loan the next business day, on Monday, November 15, but

they had a problem with a local mortgage broker so the loan funded on Tuesday, November

16. The lender’s deed of trust recorded November 18.

Meanwhile, on Monday, November 15, the IRS filed a tax lien against Gary and Diane in the

amount of $139,007. This represented the taxable portion of Gary’s severance pay, plus

penalties and interest.

The First American agent who had handled the closing became aware of the tax lien even

before the lender’s title policy was issued. Since the tax lien had priority over our to-be

insured lender, the Company immediately contacted the IRS to ask for a release.

Because Gary and Diane received only about $30,000 from the refinancing, the IRS accepted

$30,717 from First American to release its lien.

74

Dear John

Dear John

One ex’s answer to who gets what.

One ex’s answer to who gets what.

Scapegoat

Scapegoat

Who would pay for the lawyer’s mistake?

Who would pay for the lawyer’s mistake?

Short Sale

Short Sale

A favor to the seller was fateful for the buyers.

A favor to the seller was fateful for the buyers.

75

Returning home from work one day John found this note tacked to the door:

John, sold the place. I filed for divorce. The marriage is over. You have 30 days to get out! Good

Bye, Jan.”

He didn’t know where she’d gone, and after a few weeks he forgot about the note. Then one

day while napping on the couch John was awakened by voices. There is his living room were

Mr. & Mrs. Schaer, who claimed to be new owners of his home.

When John objected to them moving in, the Schaers retreated to make a claim under their

title policy. First American hired an attorney to represent them.

76

It turned out that Jan had sold the property for $30,000, and forged John’s signature to a

deed. Then she moved to a mobile home park in nearby Peoria.

Since the Schaers’ deed was hopelessly defective, First American paid them the policy

amount of $30,000. Then the Company made claims for reimbursement against Jan and the

hapless notary on the forged signature. This turned out to be an expensive quest.

Ultimately, John agreed to pay for Jan’s half interest in the property by giving a note and

mortgage to First American (as successor to Jan). Then John filed a chapter 13 bankruptcy

and things got complicated again.

Although the Company recovered most of the $30,000 it had paid, unrecoverable legal

expenses totaled more than $50,000.

77

After a split-up, exes sometimes leave title to property that was once jointly owned open to

question. Of course, Jan overdid it – and she faced criminal charges. Title insurance is great

protection against becoming entangled in the personal problems of others.

78

This stately home on Long Island had to be sold. The owners business had failed and lenders

threatened to foreclose. There were five mortgages against the property, three of which were

held by one major bank.

The bank referred two of its mortgages to outside counsel, Michael, for foreclosure. Michael was

a sole practitioner in Brooklyn.

Meanwhile, Boris and Dora contracted to buy the property and a New York City law firm was

asked to handle the closing.

In response to a closing attorney’s inquiry, Michael provided two letters containing payoff

demands for the bank’s loans. Both letters referenced loan account numbers and the address of

the property. One demand was for $289,301, and the other was for $149,721.

The deal closed and the closing attorney issued payoff checks to the bank in the amounts

provided by Michael. First American title policies were issued to the new owners and lender.

79

Within months the new owners were notified that the old first mortgage had not been released,

and the bank intended to foreclose.

It seems the payoff figure of $149,721 had been given in error, since that figure related to yet

another loan to the same borrowers secured by a different property in Brooklyn. With the

borrowers consent, the bank had gone ahead and credited the $149,721 payment to this other

mortgage, and now wanted another $309,000 to satisfy its first mortgage against the insured

property.

The new owners made a claim, and First American contacted the bank. The bank was adamant.

The bank’s attorney, Michael, blamed the closing attorney for the mistake since the loan number

referenced on his erroneous letter did not match the loan number on the first mortgage. It was

“obviously” wrong.

To make matters worse, the borrowers had moved to Florida and would be of no help settling this

disagreement. A lawsuit ensued with First American paying for the defense of its insured owners,

to prevent foreclosure of the first mortgage.

After wallowing in litigation for more than two years, the bank gave up and released the old

mortgage. First American paid legal expenses of $67,047 in defense of its insureds.

80

Another example of how the interests of innocent homeowners, and their lender, can be

jeopardized by the errors and egos of others.

81

Horst and Inger contracted to buy this duplex from Pete, a local developer. The closing would

be handled by David, an attorney.

With the closing date near David realized this would be a short sale. After paying off the

existing first mortgage, remaining sale proceeds ($58,000) would be insufficient to pay the

balance due on the second mortgage ($81,000).

The holder of the second mortgage was a local bank. At Pete’s suggestion David called the

Senior Vice President of the bank, who told him the bank would release the mortgage

without payment since Pete was a good “developer” customer.

David closed the transaction without having received the bank’s release. Unfortunately, as he

would later explain, this deal closed at a time when his conveyancing practice was starting to

grow, and he did not yet have in place procedures to follow up and get the bank’s release.

In other words, Oops.

82

Horst and Inger had an owner’s policy from First American. When they later went to

refinance, the old second mortgage showed up as still unreleased; and since it was

unreleased it now appeared as a first mortgage.

Horst and Inger made a claim and First American contacted David to get the release.

But it was too late. Things had changed at the bank. Mainly, the bank had failed and was

taken over by the FDIC. So now we couldn’t get a release. Worse yet, Pete filed bankruptcy

and went out of business.

The Company paid $80,823 for the elusive release, plus legal expenses of $9,204. Most of this

was later reimbursed by David’s professional liability insurance.

83

Title companies are frequently asked by real estate investors and developers to “write-over”

an existing mortgage with the promise of a payoff to come from some other transaction.

This is pure risk, and in some states the practice is regulated by law.

Since this risk was not authorized by First American, it was David who ultimately paid for

the bank’s favor to its “good customer.”

84

Analyzing countrywide financial figures including assets, liabilities, surpluses, and leverage ratios. Detailed breakdown for 2010, 2009, and 2008 including net premiums earned, net losses incurred, underwriting expenses, investment incomes, and taxes incurred.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

You are allowed to download the files provided on this website for personal or commercial use, subject to the condition that they are used lawfully. All files are the property of their respective owners.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.

E N D

Presentation Transcript

Joseph L. Petrelli, ACAS, MAAA President & Co-Founder, Demotech, Inc. Buckeye Actuarial Continuing Education Inaugural Meeting, April 26, 2011

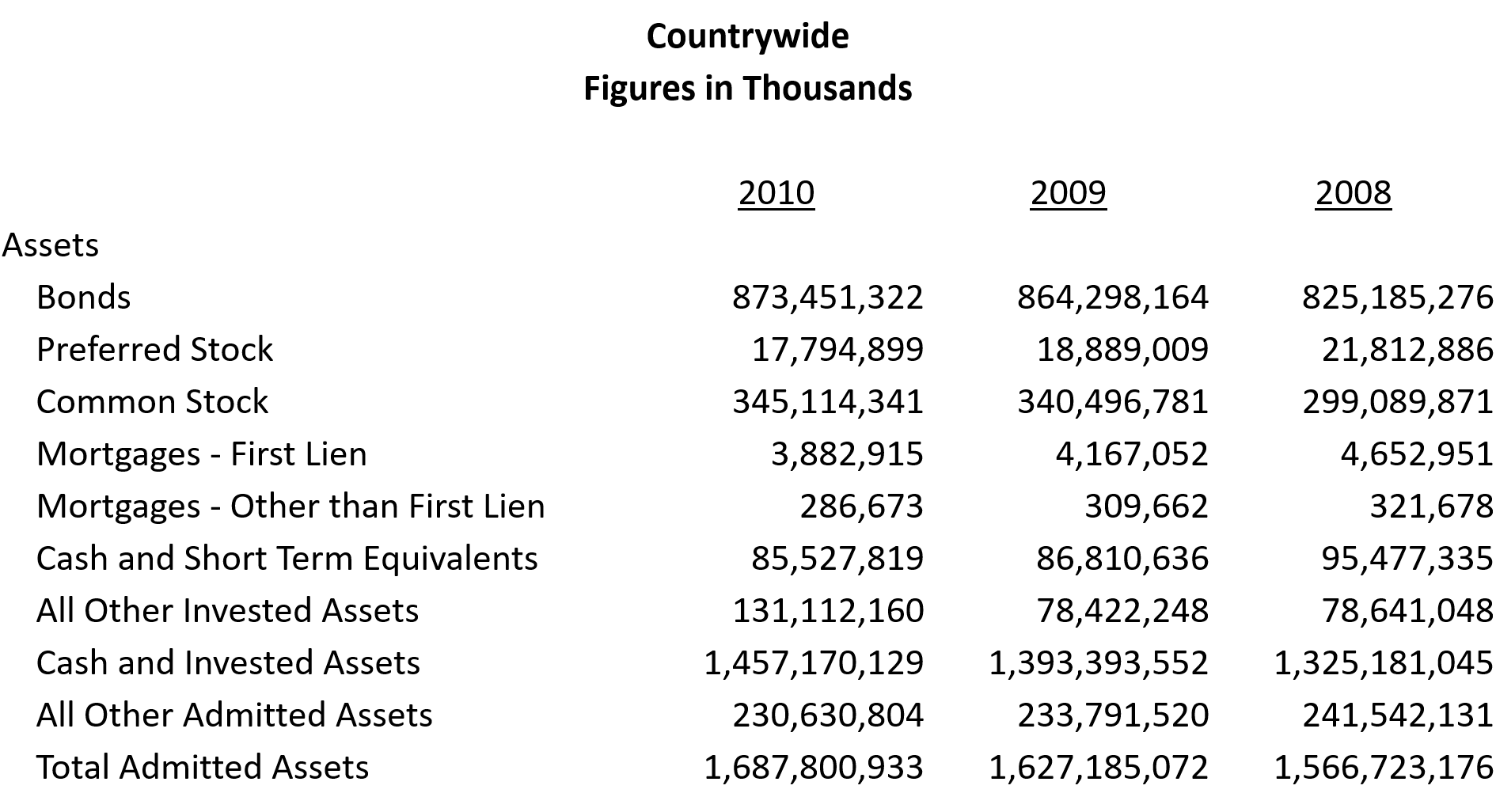

Countrywide Figures in Thousands 2010 2009 2008 Assets Bonds Preferred Stock Common Stock Mortgages - First Lien Mortgages - Other than First Lien Cash and Short Term Equivalents All Other Invested Assets Cash and Invested Assets All Other Admitted Assets Total Admitted Assets 873,451,322 17,794,899 345,114,341 3,882,915 286,673 85,527,819 131,112,160 1,457,170,129 230,630,804 1,687,800,933 864,298,164 18,889,009 340,496,781 4,167,052 309,662 86,810,636 78,422,248 1,393,393,552 233,791,520 1,627,185,072 825,185,276 21,812,886 299,089,871 4,652,951 321,678 95,477,335 78,641,048 1,325,181,045 241,542,131 1,566,723,176 2

Countrywide Figures in Thousands 2010 2009 2008 Liabilities Losses Loss Adjustment Expenses Unearned Premiums All Other Liabilities Total Liabilities 468,061,625 101,036,222 200,946,233 216,304,063 986,348,143 463,819,216 98,923,238 199,197,178 211,140,464 973,080,096 468,258,965 97,157,385 203,257,367 213,690,789 982,364,507 Reported Surplus 701,452,790 654,104,976 584,358,670 Leverage Ratio 140.6% 148.8% 168.1% 3

Countrywide Figures in Thousands 2010 424,240,335 258,960,244 53,249,448 121,140,843 (812,961) 432,537,573 (8,297,239) 57,082,100 7,825,747 64,907,847 (1,263,888) 3,181,890 (903,754) 1,014,248 57,624,856 2,701,810 54,923,046 8,892,368 46,030,678 2009 426,424,221 257,717,986 53,163,122 119,079,048 (2,337,143) 427,623,013 (1,198,792) 54,379,694 (7,807,627) 46,572,066 (1,553,143) 3,074,684 (668,448) 853,093 46,226,367 2,132,730 44,093,637 8,673,493 35,420,144 2008 442,666,077 290,499,743 52,237,311 120,874,917 (1,393,011) 462,218,961 (19,552,884) 57,878,422 (20,083,547) 37,794,875 (1,417,288) 2,955,620 (1,138,205) 400,127 18,642,118 2,189,994 16,452,124 7,868,492 8,583,631 Net Premiums Earned Net Losses Incurred Net Loss Adjustment Expenses Incurred Other Underwriting Expenses Incurred Write-Ins For Underwriting Deductions Total Underwriting Deductions Net Underwriting Gain/(Loss) Net Investment Income Earned Net Realized Capital Gains/(Losses) Less Tax Net Investment Gain/(Loss) Net Gain/(Loss) From Agents' Or Prem Bal Charged Off Finance & Service Charges Not Included In Premium Write-Ins For Miscellaneous Income Total Other Income Net Income Before Div to Polhdrs Before Fed Inc Tax Dividends To Policyholders Net Income After Div to Polhdrs Before Fed Inc Tax Federal & Foreign Income Taxes Incurred Net Income 4

Countywide Figures in Thousands Line of Business 2010 69,638,523 32,559,751 10,500,021 35,725,815 44,168,691 99,400,293 17,970,901 64,572,437 5,270,451 82,104,360 461,911,243 2009 66,385,766 33,244,773 10,667,334 36,668,038 44,694,077 96,453,656 18,381,404 64,822,736 5,632,320 83,966,086 460,916,189 2008 63,651,108 34,114,933 11,034,204 41,334,348 47,911,214 95,210,270 19,985,218 65,932,643 6,377,015 89,368,900 474,919,853 Homeowners multiple peril Commercial multiple peril Medical professional liability Workers' compensation Other liability Private passenger auto liability Commercial auto liability Private passenger auto physical damage Commercial auto physical damage All other lines of business Total 5

Ohio Figures in Thousands Line of Business 2010 2,154,274 1,029,566 358,911 -8,030 1,356,974 2,889,631 523,443 2,146,397 167,500 2,212,768 12,831,433 2009 2,043,116 1,067,420 384,583 18,225 1,370,661 2,840,594 541,024 2,147,348 175,872 2,281,955 12,870,798 2008 1,919,260 1,077,995 421,127 18,300 1,438,475 2,849,817 593,271 2,145,084 191,506 2,403,704 13,058,539 Homeowners multiple peril Commercial multiple peril Medical professional liability Workers' compensation Other liability Private passenger auto liability Commercial auto liability Private passenger auto physical damage Commercial auto physical damage All other lines of business Total 6

Countrywide Figures in Thousands Line of Business 2010 40,188,873 16,602,924 3,982,272 23,125,740 24,952,877 62,592,652 10,534,197 37,619,708 3,204,120 51,175,167 273,978,530 2009 40,419,226 17,519,687 4,459,480 23,082,713 23,641,839 61,363,621 10,859,689 38,013,506 3,238,923 60,455,505 283,054,189 2008 42,083,994 18,347,355 4,736,241 22,847,770 25,054,826 60,445,538 11,583,206 39,901,286 3,869,662 52,277,506 281,147,384 Homeowners multiple peril Commercial multiple peril Medical professional liability Workers' compensation Other liability Private passenger auto liability Commercial auto liability Private passenger auto physical damage Commercial auto physical damage All other lines of business Total 7

Ohio Figures in Thousands Line of Business 2010 1,621,870 497,969 84,538 12,719 616,948 1,691,824 256,625 1,225,275 100,972 1,171,270 7,280,009 2009 1,722,626 686,144 120,408 20,943 568,067 1,718,597 258,995 1,223,927 93,052 1,418,109 7,830,869 2008 1,801,526 680,987 107,736 23,767 562,380 1,700,125 299,444 1,311,497 114,362 1,334,162 7,935,985 Homeowners multiple peril Commercial multiple peril Medical professional liability Workers' compensation Other liability Private passenger auto liability Commercial auto liability Private passenger auto physical damage Commercial auto physical damage All other lines of business Total 8

Countrywide Figures in Thousands Line of Business 2010 41,451,086 16,286,570 3,386,559 26,358,130 23,947,723 66,662,218 9,438,978 37,525,072 3,144,380 45,241,603 273,442,318 2009 38,624,458 15,167,322 3,847,317 24,727,103 24,244,807 65,792,920 10,071,387 37,772,121 3,191,620 55,754,304 279,193,360 2008 45,139,917 19,632,541 3,957,324 25,834,743 25,446,109 62,450,756 11,053,455 40,188,312 3,838,792 81,267,578 318,809,527 Homeowners multiple peril Commercial multiple peril Medical professional liability Workers' compensation Other liability Private passenger auto liability Commercial auto liability Private passenger auto physical damage Commercial auto physical damage All other lines of business Total 9

Ohio Figures in Thousands Line of Business 2010 1,666,744 474,025 15,067 24,478 519,482 1,686,405 212,034 1,225,668 107,990 1,139,069 7,070,961 2009 1,619,338 528,093 68,740 21,211 628,584 1,708,438 221,456 1,204,093 92,838 1,343,206 7,435,998 2008 1,956,355 739,769 81,733 27,502 512,933 1,637,933 250,457 1,333,759 113,149 1,630,698 8,284,288 Homeowners multiple peril Commercial multiple peril Medical professional liability Workers' compensation Other liability Private passenger auto liability Commercial auto liability Private passenger auto physical damage Commercial auto physical damage All other lines of business Total 10

Assets 2010 2009 2008 Bonds $ 4,974,886,567 $ 4,979,545,408 $ 4,381,947,098 Preferred Stocks $ 54,502,171 $ 70,240,115 $ 79,842,924 Common Stocks $ 2,242,193,110 $ 2,398,466,510 $ 2,284,646,628 First liens $ 51,600,980 $ 51,122,288 $ 53,812,048 Other than first liens Cash, cash equivalents and short-term investments $ 1,395,833 $ 600,000 $ 600,000 $ 854,734,172 $ 846,739,378 $ 1,289,237,061 Subtotals, cash and invested assets $ 8,785,244,757 $ 8,911,430,312 $ 8,686,465,587 ALL Other $ 1,152,915,687 $ 1,265,968,041 $ 1,405,933,689 TOTALS $ 9,938,160,444 $ 10,177,398,353 $ 10,092,399,276 11

Liabilities 2010 2009 2008 Known claims reserve $ 879,970,066 $ 928,007,408 $ 1,019,478,719 Statutory premium reserve Aggregate of other reserves required by law $ 3,914,442,453 $ 3,894,463,003 $ 4,157,062,579 $ 1,270,000 $ 1,793,665 $ 1,460,603 Supplemental reserve $ 4,183,283 $ 155,147,160 $ 118,325,763 All Other $ 1,239,469,888 $ 1,185,077,018 $ 1,451,085,651 Total liabilities $ 6,039,335,690 $ 6,164,488,254 $ 6,747,413,315 Surplus as regards policyholders $ 3,898,824,754 $ 4,012,926,385 $ 3,344,982,486 Leverage Ratio 155% 154% 202% 12

Operations 2010 2009 2008 Title insurance premiums earned Escrow and settlement services Other title fees and service charges Aggregate write-ins for other operating income Total Operating Income Losses and loss adjustment expenses incurred Operating expenses incurred $ 9,423,295,853 $ 412,462,527 $ 663,903,004 $ 37,753,082 $ 10,537,414,606 $ 1,105,144,277 $ 9,638,705,200 $ 9,360,571,606 $ 416,455,120 $ 691,854,768 $ 38,428,050 $ 10,507,309,544 $ 997,571,946 $ 9,601,108,318 $ 10,199,673,342 $ 401,717,658 $ 713,538,073 $ 21,908,187 $ 11,336,837,260 $ 1,315,496,516 $ 10,731,573,196 Aggregate write-ins for other operating deductions Total Operating Deductions $ 224,910 $ 10,744,074,386 $ 840,352 $ 639,274 $ 10,599,520,615 $ 12,047,708,987 Net operating gain or (loss) Net investment income earned $ (206,659,780) $ 507,264,427 $ (92,211,072) $ 635,420,608 $ (710,871,727) $ 603,197,569 Net realized capital gains and (losses) less capital gains tax Net investment gain or (loss) $ (79,595,869) $ 427,668,558 $ (21,727,704) $ 613,692,904 $ (176,766,153) $ 426,431,416 Aggregate write-ins for miscellaneous income or (loss) Net income, after capital gains tax and before all other federal income taxes $ 20,301,135 $ 241,309,913 $ (39,670,500) $ 481,811,332 $ (1,052,095) $ (285,492,406) Federal and foreign income taxes incurred Net income $ 15,202,162 $ 226,107,751 $ (34,189,325) $ 516,000,657 $ (67,894,311) $ (217,598,095) 13

Countrywide Direct Premiums Written (in Millions) $18,000 $16,000 $14,000 $12,000 $10,000 $8,000 $6,000 $4,000 $2,000 $- 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 14

Title insurance rates vary by state. The premium is typically determined based upon a rate per thousand dollars of exposure. The one-time premium covers the parties as long as they have an insurable interest in the real property. A limited number of states have Title insurance rating bureaus. The majority of states do not. 15

Escrow and settlement services are defined as part of the Title insurance process in some states and specifically excluded from Title insurance in others. Typically, premiums are regulated by the states but fees and work charges are not regulated. 16

The basic Title insurance products are an Owners policy or a Loan policy. Although there are approximately thirty endorsements available to expand coverage, in some states there is a premium associated with the endorsements and in other states the endorsements can be requested at no charge. 17

Policies, forms and endorsements are promulgated but not filed by the American Land Title Association. Each state has a land title association that represents the interests of the local agents and domestic Title underwriters. Licensing requirements including continuing education requirements vary by state. 18

The overwhelming majority of the items that can adversely impact the marketability of Title to real property are discovered, addressed and resolved prior to policy issuance. As Title insurance coverage is retrospective and not prospective, it is my opinion that the financial reporting practices in place today cannot measure the value proposition of Title insurance. From a property and casualty insurance perspective, a Title insurance policy is more like a closed claim file than it is a P&C policy. 19

In 1994, the Federal National Mortgage Association issued Bulletin 94-13. This bulletin simplified the process for identifying acceptable title insurance companies and to minimize the potential for losses related to the type of coverage or the financial strength of the title insurer. Other participants in the secondary mortgage marketplace imposed similar requirements. 20

While Title insurance coverage looks backward from a certain date, P&C insurance coverage looks forward, utilizing a finite future period, to evaluate liability. The timeframe of coverage and cost containment activities are a fundamental difference between Title and P&C coverages. This distinction for Title underwriters has not been properly reflected in financial reporting requirements nor statistical reporting requirements. 21

Subject to the exclusions from coverage, the exceptions from coverage contained in Schedule B and the conditions and stipulations, the Title insurance company, as of the Date of Policy shown in Schedule A, against loss or damage Coverage is Retrospective. 22

In Consideration of the Provisions and Stipulations herein, the Property and Casualty Insurance Company, for the term of this date at 12:01 a.m. to one year later at 12:01 a.m. at the location of the property involved, does insure Coverage is Prospective. 23

P & C is Prospective Title is Retrospective Date of Policy Date of Policy Incident must have occurred prior to policy date to be considered covered Incident must occur within policy period considered covered to be 24

Loss adjustment expenses include allocated loss adjustment expenses and unallocated loss adjustment expenses. Allocated loss adjustment expenses are those expenses, such as attorneys fees and other legal costs, that are incurred in connection with and assigned to specific claims. Unallocated loss adjustment expenses are all other claim adjustment expenses and include salaries, utilities and rent apportioned to support the claim adjustment function although not readily assignable to any specific claim. 25

Access Denied This motel was landlocked after a neighbor s foreclosure. Bumped and Stumped Was it too much to ask that the mortgage be recorded? Partnership Pie The managing partner knew to manage for himself. 26

Located on Interstate 40 (old Route 66), at midpoint of the long haul between Oklahoma City and Amarillo, is the Highway 8 Motel at Elk City. For many years business flourished. When the owner was tired of turning away travelers, he bought more land behind the motel and built an addition. Construction was paid for by a new loan secured by a deed of trust against the rear lot. 27

The motels success did not go unnoticed. Others bought land across the interstate, and soon a new Holiday Inn appeared, then an Econo-Lodge. Business fell off at the old Highway 8. When the owner fell behind in payments, his lenders foreclosed. The lender on the rear lot was in for unpleasant news. There was no right of access anywhere to connect it with a public road, and the lender on the frontage lot would no longer allow it to be used to access the rear. Who, after all, needs competition? Following litigation over the true amount of its damages, the insured lender received about $83,000 from the title company. 28

Title insurance includes coverage for a right of access. This coverage is included in all owner, loan and leasehold policies. Any prospective insured wanting a specific right-of-way should be careful to make sure that the same is expressly insured by the policy to be issued. Otherwise, the insured may be surprised to learn that the desired right-of-way cannot be used, and instead, access is allowed by some less desirable way. 29

After closing a $1.6 million construction loan on this apartment project in South Philly, the closing agent made the most serious of mistakes: he forgot to record the mortgage. By the time the mistake was discovered, the developer was in serious trouble, with 24 tax and judgment liens filed against him totaling more than $800,000 in liabilities. When the insured lender began foreclosure, they learned that because of the recording snafu their priority was bumped from 1st to 25th! 30

It only got worse. Before the original mortgage could be located (it was in the agents file), the developer filed bankruptcy. Now the trustee in bankruptcy threatened to void the insured mortgage altogether using section 544(a)(3) of the Bankruptcy Code. That section permits a trustee in bankruptcy (or a debtor-in-possession) to avoid any interest in real property which is not perfected (in this case, by recording) as of the date of commencement of bankruptcy. However, because the mortgage was only partially funded, and thanks to contribution from the agent s errors and omissions insurance carrier, First American s loss was limited to $55,000. 31

Whenever an interest in real property is not perfected by recording, three things can wipe out the interest: The grantor may sell or mortgage the property to another (bona fide purchaser/encumbrancer) without disclosing the unperfected interest; 1. Intervening liens or encumbrances may be recorded, gaining priority; or 2. The grantor may go into bankruptcy, whereupon the trustee avoiding power (Bankruptcy Code section 544 (a)(3)) may be invoked to avoid the interest as against the debtor s real property. 3. 32

It seemed like a great opportunity, a limited partnership owning this luxury home on a bluff overlooking the Pacific. This property had it all: 11,000 square feet of living space, a swimming pool, tennis courts and panoramic view of Malibu s beaches. In all, 15 limited partnership shares were offered to investors throughout Los Angeles. After renovation, the home would be put on the market for $6 million. Who cared if it didn t sell? Sooner or later the market would have to catch up. So it was one evening as two of the partners watched Lifestyles of the Rich and Famous on television. Something Robin Leach was saying, something about Malibu and the man with the Midas touch, caught their attention. There on screen was their managing partner. The young multi-millionaire, gushed Leache, who sees opportunities and seizes them. But wait! Now on screen was their house, their investment, his magnificent mansion that serves as international headquarters! It was unmistakable. It had all the wood From the old Vanderbilt Mansion on Long Island, bragged the general partner. 33

The partners investigated. Soon they learned that their general partner, using his broad powers under their limited partnership agreement, had deeded the property to himself. Then he borrowed $2.3 million from an unsuspecting bank, secured by a deed of trust against the property. While some of this money was used to retire partnership debts, the rest (about $900,000) disappeared in the general partner s personal accounts. Tricked out of their shoes, the partners got together and filed suit to get the property back and avoid the deed of trust. Their attorneys would claim that the deed of trust was unauthorized, not given for partnership purpose. The deed of trust was insured by First American. The Company hired lawyers to represent the lender s interests. Dozens of depositions were taken. After a trial lasting several weeks, the judge ruled in favor of the lender. He concluded the partners had given the general partner such broad authority that the lender was justified in dealing with him solely. After recouping court-awarded costs, First American paid legal expenses of $365,280. 34

In every real estate transaction, the title company must be satisfied that parties involved are mentally competent or, where a business entity is involved, legally authorized to act. Where partnerships are involved, the title examiner should review the partnership agreement to see that the person with whom he or she is dealing has authority to contract on behalf of the partnership, and that this authority is broad enough to include the transaction at hand. Frequently, partnership agreements provide that there be no sale, lease or mortgaging of partnership property without the vote or consent of a majority of partners. This basic risk of incompetency, incapacity or lack of authority of parties is typically covered by insurance. 35

Access To Come Please, Mr. Postman The lament of the landlocked. First Name First ABC s of searching records. NSF Some bad advice, a bad check and two former partners. 36

Plans called for this retirement and convalescent facility to have two driveways. Set back from March Lane, a busy thoroughfare, the facility was to have access both to March Lane and to a nearby side street. The neighbor who owned the surrounding property agreed; it was a done deal. The developer was anxious to get started, but the escrow officer had yet to receive easement deeds from the holder of the neighbor s mortgage, a savings and loan association. Yielding to the developer s wishes, escrow was closed with easement deeds to be received and recorded later. The deeds failed to arrive and were eventually forgotten about Details. 37

Meanwhile, the neighbor lost his land through foreclosure, and it was acquired by the foreclosing S&L. Then the foreclosing S&L failed and was taken over by FSLIC. FSLIC inspected the land and told the developer to forget about getting any easements, even though one concrete driveway was already in place. FSLIC threatened to tear it up. First American hired a lawyer to represent the insured owner and lender, and peace was made with FSLIC. The Company paid $35,000 for confirmation of an easement where the concrete driveway is located, and in the process incurred legal expenses of $10,000. 38

Real estate transactions are frequently closed with needed documents promised, but not in hand. This is most often the case with releases or satisfactions of paid-off mortgages or liens. This practice is approved by title companies, and they are willing to insure against paid-off items. When this practice is followed, the escrow or closing officer should have written evidence of the paid-off party s agreement to provide a written release by return mail. On the other hand, where a promised document directly affects immediate rights of use and possession, such as a deed or easement deed, it is too important to go without. Any death, displacement, disability or bankruptcy of the party giving a verbal promise can render the promise useless. 39

This tale begins with foreclosure of this retail store space to satisfy an unpaid mortgage. Four years later, John was served with a lawsuit filed by Joyce, whom John had never heard of, seeking to foreclose a ten year-old mortgage, which also John had never heard of. The unpaid balance of the mortgage was said to be more than $100,000. The successful bidder was John, who after the foreclosure wisely obtained an owner s policy of title insurance from an agent of First American. This policy insured the property free and clear of any mortgages or liens. John called the title agent here s what we learned. The property was formerly owned by a corporation named Anita Lee Gift Shop, Inc. This corporation was owned by William and Joyce, who were husband and wife. When the couple split, William took over the gift shop and promised to pay Joyce $120,000, in monthly installments of $1,000 for ten years. This promise was secured by the aforementioned mortgage, in favor of Joyce, which was duly recorded in Camden County land records. 40

Later, William gave a second mortgage to a financial institution, which was the same mortgage that was later foreclosed resulting in the ownership of our insured, John. In searching the records prior to issuing our policy to John, the searcher checked the recorder s alphabetical index for Lee,Anita rather than AnitaLee, and so missed the mortgage in favor of Joyce. More bad news William had made almost none of his mortgage payments, so the balance now due Joyce was equal to the value of the property. This was a total failure of title. First American paid $116,875 to satisfy the missed mortgage. 41

The protocol for posting, indexing and searching proper names of individuals is last name first, first name last. This rule doesn t apply to corporations, whose names should be listed under the first letter of the name as registered with the state of incorporation. This rule is sometimes misunderstood by county employees who do indexing or posting, and is also misunderstood by title searchers. Experienced searchers know to check every conceivable variation of a name under search. 42

The uptown shopping center was owned by the partnership of John and Ron. The managing partner was John. One January 31st the partnership sent a check for $385,616 to the county tax assessor for second installment property taxes. This check was drawn on the account of Riverfront Plaza Property Management, a company owned solely by John. When they received the check, the office of the tax assessor made a record that the taxes had been paid but then the check bounced ( NSF Refer to Maker ). Meanwhile, John decided to sell his interest in the partnership. A First American agent was asked to handle the transfer of ownership to a new partnership. The closing officer checked for property taxes and received from the Cook County Clerk a Certificate of Payment, dated April 1, showing second installment taxes as paid. The transfer of ownership closed a few days later, and a First American owner s policy was issued with no exception for past-due taxes. 43

After the closing, former partners John and Ron held a post-closing reconciliation meeting in which they settled business matters between themselves and signed mutual releases. More than a year later, First American was notified that the old secondinstallment taxes remained unpaid and now stood as a lien against the property in the amount of $499,552, including penalties and interest. When first contacted, neither of the former partners seemed interested in the problem. One put us off for months saying through his lawyer that the taxes had been paid or, perhaps, an account was established somewhere to cover them. Lawsuits were filed and, after months of wrangling, the former partners settled with John agreeing to pay the taxes. First American continues to pursue John to recover its legal expenses, totaling more than $340,000. 44

Title insurance is your best protection against ineffective payoffs at the time of closing such as resulting from a bad check. 45

Breach of Trust Money to pay off mortgages was missing. Masquerade When he tried to take possession, the buyer got a surprise. Power of Attorney Title stolen through fake authority. 46

Thomas M. Dameron was a successful attorney with a hand in several companies offering title and settlement services in Northern Virginia. One of these companies, Mid-Atlantic Title & Escrow Services, was an authorized agent of First American. Dameron got interested in developing a shopping center and waste treatment plat at Inwood, West Virginia. Rather than borrowing money to finance these projects, he began diverting funds provided to pay off mortgages in connection with property sales and refinancings handled by his Virginia-based companies. (Defalcation) To conceal these diversions Dameron continued monthly payments on mortgages which should have been paid off, and he routinely issued title policies to new owners and lenders as if the old mortgages were released. Obviously, this sort of thing can get out of hand. Every month Dameron had to take more and more money to keep things quiet. But that wasn t what stopped him. 47

Things started to unravel around January when lenders mailed IRS 1099 forms to Damerons clients, showing their mortgage interest payments for the past year. Several clients were surprised at the numbers on their 1099 s. They investigated and wrote letters to the State Bar. Dameron was caught. He was arrested and pleaded guilty to federal charges of bank years. His seven-month spree saw misappropriations totaling about $4 million. With Dameron in the pokey, mortgage payments stopped and lenders began to foreclose. In all, 24 homeowners made claims under First American policies or commitments, and the Company paid a total of $2,564,304 to clear up their titles. The Company also paid accounting and legal expenses of $491,296. 48

First American offers title insurance through thousands of independent company and attorney agents throughout the United States. The Company s goal is to affiliate only with the most competent and ethical agents in the business. And, First American has a large staff of agency representatives trained to do field audits and spot problems and help agents avoid trouble. But occasionally an agent can go wrong. When it happens, the homeowner s best protection is an owner s policy of title insurance. 49

When First American handled the sale of this property, insuring a new owner and lender, there were clues that something was wrong. First, the sale was for a bargain price and to be confidential so not to upset the tenants in six rentals on the property. Second, in checking public records, the examiner encountered an eleven year-old probate opened for a decedent whose name was identical to the name of our seller, Anna X. Even though the name was uncommon, the examiner disregarded the probate and didn t bother to review the courthouse file assuming it was a coincidence. Third, when our seller appeared to sign the deed she had no identification in the name of Anna X. Instead, her driver s license bore the name Patricia Anna McGinnis. She explained that since acquiring the property seventeen years earlier she went through a divorce and changed her name. The escrow officer believer her, and notarized the deed signed by Patricia as Anna X. 50

, at midpoint of the")