Energy Sector Challenges and Solutions in Pakistan

Khalid Saeed

Head

Energy Research Centre

COMSATS Institute of Information Technology,

Lahore Campus

Introduction

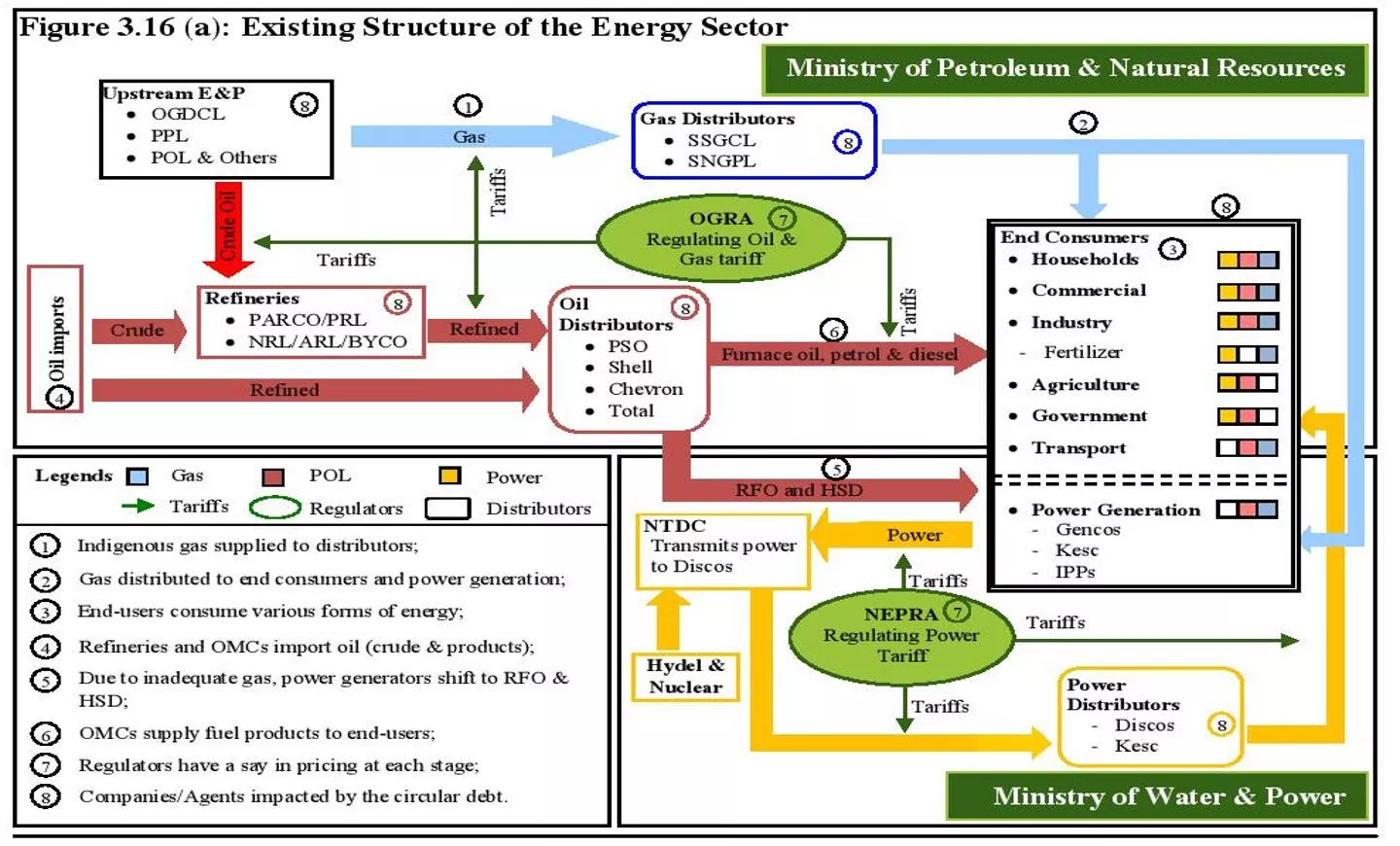

Existing Structure of Energy Sector

2

Major Challenges

Demand and Supply Gap: 6000-7000MW (1/3

rd

of

total demand)

3

4

Sources: Overseas Investors Chamber of Commerce & Investments (OICCI)

Pakistan, Energy Sub Committee, NEPRA’s State of Industry Report 2013

Major Challenges

High cost fuel mix for power generation

Major Challenges

5

High cost fuel mix for power generation

– Low hydel share;

decrease in gas allocation for power sector

Major Challenges

Fall in share of investments in Energy Sector: While in

mid 90’s, 26% of total and 51% of public sector

investments, the share of energy (including power)

dropped to 4% and 26% by 2009-10.

Trust Deficit – a reason for inability to undertake large

hydel projects over last 25 years (except Ghazi- Barotha)

6

Major Challenges

7

High T & D losses and poor recoveries by DISCOs

8

System Losses and Revenue Recoveries

DISCO

Distribution

Losses Recovery

(2011-12)

(2011-12)

PESCO

35%

68%

HESCO

28%

69%

SEPCO

49%

53%

QESCO

21%

36%

IESCO, JEPCO,

FESCO, LESCO

(average)

9.5%-13.5%

95%-98%

Source: NEPRA: State of Industry Report: 2012

The table below indicates the level of losses and percentage of dues being

recovered by various DISCOS.

9

DISTRIBUTION LOSSES IN DIFFERENT COUNTRIES

Country %age of output

Transmission &Distribution Losses

Australia

7%

USA

6%

Canada

8%

Germany

4%

France

6%

UK

7%

S. Korea

4%

Malaysia

4%

Iran

17%

China

5%

Egypt

11%

India

24%

Pakistan

20%

Source: World Development Indicators Report: 2012

Major Challenges

Unsustainable tariff regime

10

Major Challenges

2% loss to GDP

– Impact on employment/

exports/budget deficits and circular debt

11

Major Challenges

Degeneration/ Derating of Public Sector Gencos

Uniform national tariff – No incentive for efficiency/

better recovery/ cutting theft and losses

Circular Debt/ Inability to fully operate all available

generation capacity due to shortage of funds to get

fuel.

12

Road Ahead: Way Forward

1.

Diversity – More reliance on renewable energy

(hydel/solar/wind)

2.

More gas allocation – Add coal based power

generation

3.

Improve efficiency of public sector Gencos – Also

introduce efficiency for industrial machinery,

transport and household appliances

4.

Manage demand through conservation measures

13

Road Ahead: Way Forward (Cont.)

5.

Rationalize tariff regime

6.

More investments – Public and Private sector to

upgrade Power sector T & D infrastructure

7.

Timely payments to avoid circular debts

8.

Develop political consensus on energy security issues

14

Road Ahead: Way Forward (Cont.)

9.

Improve governance to cut theft/corruption and

inefficiency

10.

Improve governance at policy level inter-ministerial

coordination – single Energy Ministry

15

Salient Features of National Power

Policy 2014

To achieve the long-term vision of the power sector and

overcome its challenges, following goals have been set:

i.

Build a power generation capacity that can meet

Pakistan’s energy needs in a sustainable manner.

ii.

Create a culture of energy conservation and responsibility

16

Salient Features of National Power

Policy 2014

iii.

Ensure the generation of inexpensive and affordable

electricity for domestic, commercial, and industrial use

by using indigenous resources such as coal (Thar coal)

and hydel.

iv.

Minimize pilferage and adulteration in fuel supply

v.

Promote world class efficiency in power generation

vi.

Create a cutting edge transmission network

17

Salient Features of National Power

Policy 2014

vii.

Minimize inefficiencies in the distribution system

viii.

Minimize financial losses across the system

ix.

Align the ministries involved in the energy sector and

improve the governance of all related federal and

provincial departments as well as regulators

18

19

The Energy Research Centre at COMSATS Institute of Information Technology, Lahore Campus, highlights major challenges in Pakistan's energy sector, including demand-supply gaps, high fuel costs, investment declines, and distribution losses. The table comparison of distribution losses in different countries underscores the need for sustainable tariff reforms.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

You are allowed to download the files provided on this website for personal or commercial use, subject to the condition that they are used lawfully. All files are the property of their respective owners.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.

E N D

Presentation Transcript

Khalid Saeed Head Energy Research Centre COMSATS Institute of Information Technology, Lahore Campus

Introduction Existing Structure of Energy Sector 2

Major Challenges Demand and Supply Gap: 6000-7000MW (1/3rd of total demand) 3

Major Challenges High cost fuel mix for power generation Sources: Overseas Investors Chamber of Commerce & Investments (OICCI) Pakistan, Energy Sub Committee, NEPRA s State of Industry Report 2013 4

Major Challenges High cost fuel mix for power generation Low hydel share; decrease in gas allocation for power sector 5

Major Challenges Fall in share of investments in Energy Sector: While in mid 90 s, 26% of total and 51% of public sector investments, the share of energy (including power) dropped to 4% and 26% by 2009-10. Trust Deficit a reason for inability to undertake large hydel projects over last 25 years (except Ghazi- Barotha) 6

Major Challenges High T & D losses and poor recoveries by DISCOs 7

The table below indicates the level of losses and percentage of dues being recovered by various DISCOS. System Losses and Revenue Recoveries DISCO Distribution Losses Recovery (2011-12) (2011-12) PESCO 35% 68% HESCO 28% 69% SEPCO 49% 53% QESCO 21% 36% IESCO, JEPCO, FESCO, LESCO (average) 9.5%-13.5% Source: NEPRA: State of Industry Report: 2012 95%-98% 8

DISTRIBUTION LOSSES IN DIFFERENT COUNTRIES Country %age of output Transmission &Distribution Losses Australia 7% USA 6% Canada 8% Germany 4% France 6% UK 7% S. Korea 4% Malaysia 4% Iran 17% China 5% Egypt 11% India 24% Pakistan 20% Source: World Development Indicators Report: 2012 9

Major Challenges Unsustainable tariff regime 10

Major Challenges 2% loss to GDP Impact on employment/ exports/budget deficits and circular debt 11

Major Challenges Degeneration/ Derating of Public Sector Gencos Uniform national tariff No incentive for efficiency/ better recovery/ cutting theft and losses Circular Debt/ Inability to fully operate all available generation capacity due to shortage of funds to get fuel. 12

Road Ahead: Way Forward Diversity More reliance on renewable energy (hydel/solar/wind) 2. More gas allocation Add coal based power generation 3. Improve efficiency of public sector Gencos Also introduce efficiency for industrial machinery, transport and household appliances 4. Manage demand through conservation measures 1. 13

Road Ahead: Way Forward (Cont.) 5.Rationalize tariff regime 6. More investments Public and Private sector to upgrade Power sector T & D infrastructure 7. Timely payments to avoid circular debts 8. Develop political consensus on energy security issues 14

Road Ahead: Way Forward (Cont.) 9. Improve governance to cut theft/corruption and inefficiency 10. Improve governance at policy level inter-ministerial coordination single Energy Ministry 15

Salient Features of National Power Policy 2014 To achieve the long-term vision of the power sector and overcome its challenges, following goals have been set: Build a power generation capacity that can meet Pakistan s energy needs in a sustainable manner. i. ii. Create a culture of energy conservation and responsibility 16

Salient Features of National Power Policy 2014 iii. Ensure the generation of inexpensive and affordable electricity for domestic, commercial, and industrial use by using indigenous resources such as coal (Thar coal) and hydel. iv. Minimize pilferage and adulteration in fuel supply v. Promote world class efficiency in power generation vi. Create a cutting edge transmission network 17

Salient Features of National Power Policy 2014 vii. Minimize inefficiencies in the distribution system viii. Minimize financial losses across the system ix. Align the ministries involved in the energy sector and improve the governance of all related federal and provincial departments as well as regulators 18

")

")