All About Credit Cards: A Comprehensive Guide

Explore the world of credit cards, from understanding the basics to managing credit wisely. Delve into the advantages and disadvantages, learn about different types of credit cards, and discover how to use credit cards responsibly. Discuss whether high school students, college students, and adults should have credit cards. Engage with interactive resources and videos to enhance your knowledge on credit card usage and management.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

You are allowed to download the files provided on this website for personal or commercial use, subject to the condition that they are used lawfully. All files are the property of their respective owners.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.

E N D

Presentation Transcript

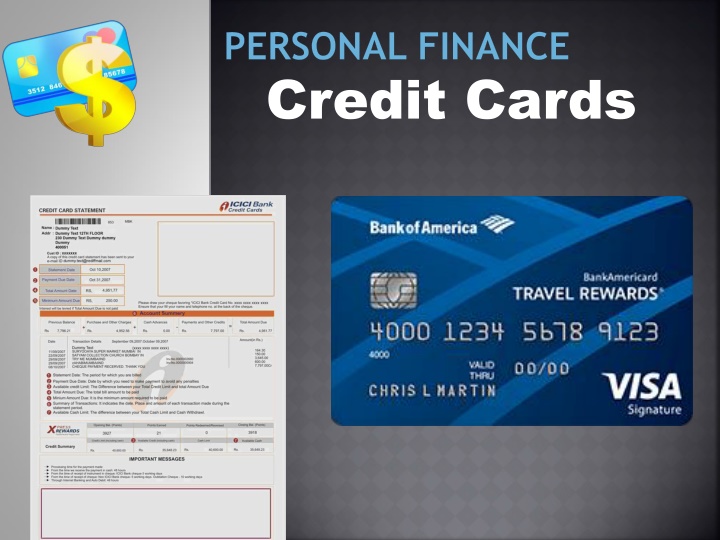

PERSONAL FINANCE Credit Cards

UNITED STATES TOTAL DEBT Website: https://www.newyorkfed.org/microeconomi cs/hhdc.html Complete worksheet and be prepared to discuss questions.

DISCUSSION PROMPT Do you think it s a good idea for high school students to have a credit card? What about college students? Adults? Explain why

QUESTION: Prior years was How can I get credit? Now it is How can I wisely manage credit?

WHAT YOUNG ADULTS SAY ABOUT CREDIT CARDS https://www.youtube.com/watch?v=NtXwlU DK2co After hearing the opinions of the students in this video, do you think YOU would want a credit card in college? Why or why not?

CREDIT CARD BASICS https://www.youtube.com/watch?v=-OSc- Mm0tJo#t=44 In your notes, summarize the Difference between credit & debit Three types of credit cards, and At least 3 benefits of using a credit card for purchases.

COSTS WHAT?! - CREDIT CARD PREMIER http://www.thirteen.org/finance/games/itc ostswhat_creditcard.html Read the text & push NEXT on this interactive to learn about credit cards. Then, take the 6-question quiz to test what you've learned.

CREDIT CARDS The credit of today Transactions that require a credit card Log into Lapointe s Padlet: https://padlet.com/jl01128/vd6yrfvgtf40 Stores are encouraging customers to use their credit cards to purchase goods & services Log into Lapointe s Padlet: Which stores are famous for their department store credit cards. https://padlet.com/jl01128/p2y5bkgn0hyh People have overextended their credit. Part of lifestyle making ends meet.

CREDIT CARDS: ADVANTAGES & DISADVANTAGES Advantages Used correctly expands purchasing power & raise your standard of living Provides emergency funds if you don t have the cash Line of credit - money available when you need it Convenient and better service (for ex. Problem with purchase withhold payment) Deferred Billing Service available to charge customers where payment is billed at a later date. For example item purchased in October billed in January, payment is due February

CREDIT CARDS: ADVANTAGES & DISADVANTAGES Disadvantages Credit purchases might cost more than cash Merchants must pay fees usually a % of the sale at no additional cost to the customer Finance Charge 18% or more per year (1 % per month) Purchases on credit cards could equal overspending No cash has been transferred don t realize the amount if in debt that is so high - bankruptcy http://www.youtube.com/watch?v=7U6pmkT C8i0 Credit Card Debt - A Student's Story

TYPES & SOURCES OF CREDIT Open-End Credit Borrower can use credit up to a stated limit Credit can be used again & again as long as balance owed doesn t exceed the credit limit Charge Cards An agreement made to pay the balance in full owed each month Usually 25-day billing period Visa, Master Card, Discover, American Express Nationwide and overseas Rewards or rebates based on purchases made

DECIPHER CREDIT CARDS WITH THE SCHUMER BOX Review this reference sheet: Decipher Credit Card Offers With the Schumer Box While ALL the information in a Schumer Box is important, which items do you think matter most on a day-to-day basis? (Add this to your notes)

UNDERSTAND YOUR CREDIT AGREEMENT Follow the directions on the worksheet to complete this activity. Schumar box worksheet 1

TYPES & SOURCES OF CREDIT Revolving Accounts Borrower has option each month to pay balance in full or make monthly payments Most All-purpose cards are: Visa, Mastercard, Discover, gasoline cards, and store cards

TYPES & SOURCES OF CREDIT Credit Card Agreements Annual Percentage Rate (APR) cost of credit expressed as a yearly percentage. Can be variable rate Truth-in-Lending Law will discuss later Credit Utilization Paying bill on time Fee if over credit limit Grace Period Time frame to pay current bill in full incur no interest charges Usually 25 days Annual Fees Fee charged annually range from $15+ is paid whether you use the card or not.

TYPES & SOURCES OF CREDIT Credit Card Agreements Transaction Fee 3% to 10% maybe be charged if use a credit card check, pay by phone or request a balance transfer Penalty Fee If go over credit limit or make your payment late $25 to $50 is a flat rate Finance Charge A percentage charged monthly for purchases that were not paid for. To calculate that use either of the following formulas:

1. Change Annual Percentage rate into a decimal APR 24% = .24 Annual rate 2. Convert ANNUAL rate into a DAILY rate APR .24 is turned into .24/365 = .0007 daily rate (let s round to the 4th place) 3. Multiply daily rate * existing balance = daily interest 4. Daily interest * # of days in a month = monthly interest

CREDIT CARD INTEREST CALCULATIONS- WHITEBOARD PRACTICE You have a $3,500 credit card balance 1. Your APR is 29% 2. What is your monthly interest assume 31 days in the month? Show your work! 3.

MINIMUM CREDIT CARD PAYMENTS How long does it take to payoff a credit card? Minimum Payment Worksheet

MINIMUM PAYMENT WORKSHEET ANSWERS

CREDIT CARD PAYMENT REVIEW Part two purchasing a computer.

CREDIT CARD DEBT EXPLAINED https://www.youtube.com/watch?v=L5qlbISOA GA How can you avoid paying interest on your credit card? Explain what happens if you make the minimum payment every month. How does the credit card companies' definition of a deadbeat compare to the traditional meaning?

IT COSTS WHAT?! - CASE FILES Read the case files and answer the online questions to solve this interactive case. http://www.thirteen.org/finance/games/itc ostswhat_casefiles.html Answers: Kevin, who paid a total of $360.28 Emma, who paid a total of $714.86 Maria, who paid a total of $350.00 Byron, who paid a total of $514.24

SHOPPING WITH INTEREST Socrative Review:

WHY WE SPEND MORE WHEN WE PAY WITH CREDIT CARDS Read: http://www.wisebread.com/why-we- spend-more-when-we-pay-with-credit-cards In your own words, write in your notebook two reasons we tend to spend more with credit than with cash. Be prepared to be called on.

HOW DO WE KEEP CREDIT CARD SPENDING IN CHECK? Use your credit card only for fixed expenses. Always check prices. Stay within your budget. Make sure you have the cash for it. Go on a cash diet.

WHAT IS A BALANCE TRANSFER? http://www.creditcardfinder.com.au/what- is-a-balance-transfer.html After watching this video, give an example of why someone might want to utilize a balance transfer offer.

POTENTIAL PROBLEMS OF BALANCE TRANSFERS The Transferred Balance Is Usually Credited First The Transferred Balance Is Usually Credited First Balance Transfer Fees Eat Up Savings From Transferring Rewards Can Entice You to Spend More Your Credit Score Can Drop Other Fees May Be Lurking 1. 2. 3. 4. 5. 6.

WHY 0% FINANCING FROM RETAILERS CAN BE A BAD DEAL Interest postponed isn't necessarily interest denied It could hurt your credit 2 balances can add complications Missing payments will stop the 0% interest period

PERSONAL FINANCE 101: WHAT IS A CASH ADVANCE? http://www.thesimpledollar.com/what-is-a- cash-advance/ After reading this article, in your notebook write down the 3 reasons why a cash advance is a costly way of using your credit card.

CREDIT CARD LAWS WEBQUEST RESEARCH: Follow the directions on the worksheet to complete this activity. You may place the answers in your notebook.

UNDERSTANDING YOUR CREDIT CARD STATEMENT

UNDERSTANDING YOUR CREDIT CARD STATEMENT http://www.mycreditunion.gov/Pages/pocket-cents- understanding-credit-card-statement.aspx Learn about credit card statements by hovering over each orange dot. Once you understand the statement, be prepared to answer the questions on Socrative.

UNDERSTANDING YOUR CREDIT CARD STATEMENT How large a payment must this customer make on 4/20/12 to be considered on-time with their payment? 1. If the customer wants to avoid paying interest, how much should she send by 4/20/12? 2. What is this customer s interest rate, going forward? 3. What types of fees are included on this customer s credit card statement for the month? 4. How much did this customer pay last month? 5. If you could offer this customer just ONE piece of advice, what would you choose? 6.

RECAP: TYPES & SOURCES OF CREDIT Service Credit Providing service for which will paid for later Utility Bills, Telephone, Cell Phone Some businesses may extend service credit Doctors, lawyers, repair shops, hospitals, dentists Retail Stores Some stores offer their own credit cards Store Benefits Additional percentage discount, advance notification of sales

RECAP: SOURCES OF CREDIT Credit Card Companies Offers from Visa, Master Card, Discover, etc. Affinity cards (professional organizations, college alumni, etc.) AAA Visa, Walmart Visa Cash Advance ability to borrow cash against your credit card Use an ATM, or writing a check Higher interest rate and transaction fee (immediate) Interest accruals immediately Transfer Funds Teaser rates limited time Transfer Fees Full payment by end back interest is added to charge