Actuarial Perspective on Value Added Benefits in Indian Health Insurance

Serving

the Cause of Public Interest

Indian Actuarial Profession

28

th

India Fellowship Seminar

Value added benefits in health insurance – an

actuarial perspective to the viability and are they

worth for the customers

Guide Name:

A V Karthikeyan

Presenters Name:

1.

Swati Anil Umre

2.

Mansi Kukreja

3.

Safder Jaffer

Date: 09 November 2017

Mumbai

Agenda

•

Introduction to the Indian Healthcare Industry

•

Defining Value Added Benefits

•

Benefits and Limitations: For the Customer

•

Benefits and Limitations: For the Insurer

•

Pricing Approaches: Risks & Challenges Associated With

Pricing

•

Conclusions

www.actuariesindia.org

2

www.actuariesindia.org

3

Source: * IBEF

^

World Health Organization (WHO), BMI

3

4

5

1

2

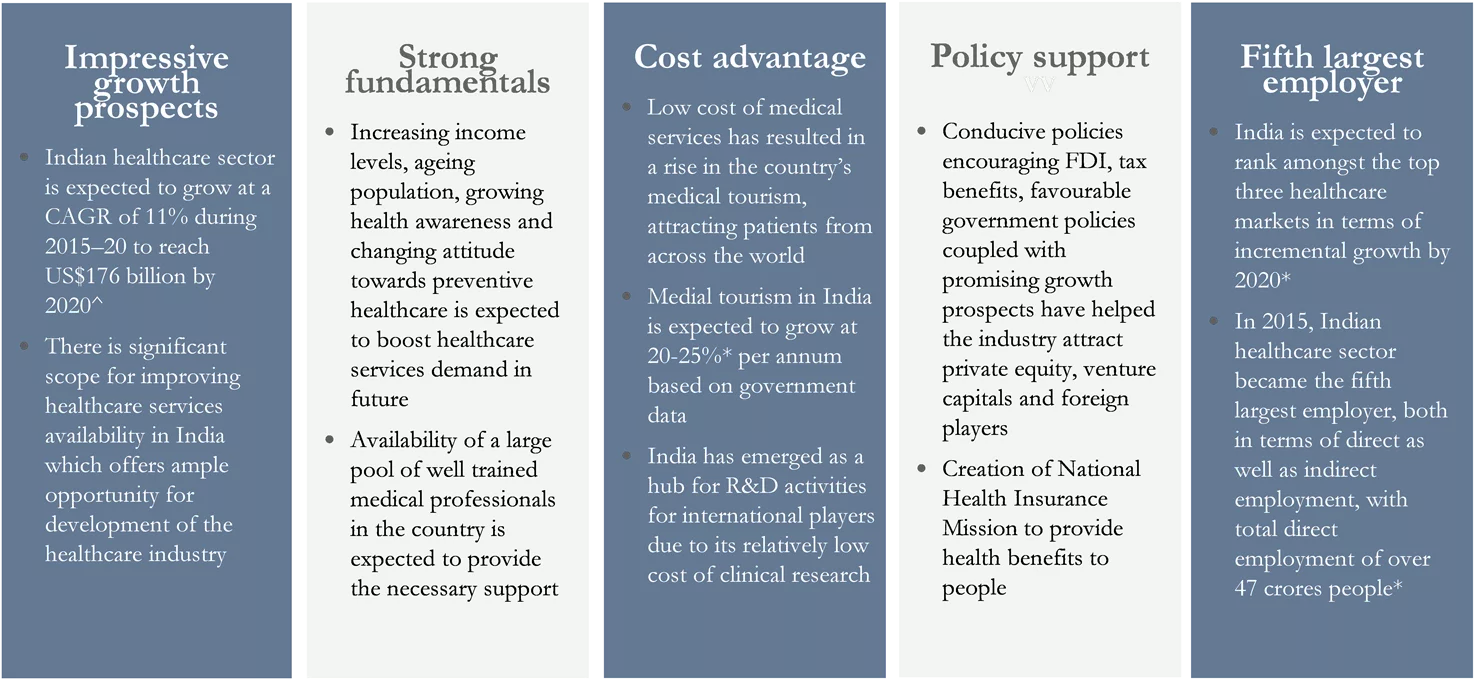

Salient features of Indian healthcare industry

Health care is one of the most promising sectors of the

Indian economy

Overview of the Indian health insurance market

* Not a significant portfolio

Agency

►

Traditional agents

►

Variable agency model

►

Brokers

►

Bancassurance

►

Corporate agents

►

Web aggregators

Third party

Limited Indemnity

Group

►

Group health insurance

cover (either employer-

employee or non employer-

employee (like holders of the

same credit card, etc.)

►

Reimbursement

against the

costs of medical expenses

►

Direct payment to provider as

an option, known as cashless

Indian

Health

Insurance

sector

Critical Illness*

►

Lump sum payment on

diagnosis of

one of the

specific life threatening

illness

Add on coverages (e.g. Dental)

Category accounts for major

share of the segment

www.actuariesindia.org

3

Increasing

Healthcare costs

Healthcare expenditures

continue to rise as the

government modernizes

India’s healthcare system

4

Technology

New technologies

disrupting health

insurance

Insurers launching

mobile apps & internet

based services

5

Regulatory

reforms and tax

incentives

Recognition of Health

insurance as a

standalone class;

allowing more

opportunities through

open architecture

Increase in tax benefits

in 80D from 15K to

25K

1

Increased

Awareness

Increasing awareness

of health insurance and

growing perception of

insurance needs among

people, evidenced by

~21% growth in the

retail health insurance

2

High out of

expenditure

62%

per cent of the

total health care

expenditure in the

country was borne by

households out of their

pockets in 2014

In

INR

Bn.

Key growth drivers for health insurance

Source: WHO Study; IRDA Annual reports

CAGR: 16.9%

Complementing the growth in healthcare industry, health insurance sector

has also experienced an impressive CAGR of ~17% between FY 12-16

Health insurance GWP

www.actuariesindia.org

Health insurance products falls under two main categories

Health Insurance Products

Health Insurance Products

www.actuariesindia.org

www.actuariesindia.org

7

Value

Added Benefits in

Health Insurance

www.actuariesindia.org

8

www.actuariesindia.org

9

The

KANO

Analysis

for ever changing customer needs

DELIGHTERS

•

Wellness Coach

•

Gym Membership

•

Health Checkups

•

Health Reward Points

•

Air Ambulance

•

Hospitalization Benefits

•

Quick Claim settlement

•

Outpatient Treatment

•

24 * 7 helpdesk

•

Road Ambulance

EXPECTATION

www.actuariesindia.org

10

•

Perceived Satisfaction:

More delighters, higher

satisfaction

•

Motivation to Stay Fit

•

Lifestyle Disease Management

•

Access to more Appropriate Care

•

Low Utilization risk

•

Onerous T&C - Complexity in Understanding

•

Data Security and Privacy issues

For the Customer

www.actuariesindia.org

11

What does Regulation Says?

www.actuariesindia.org

12

•

Way Forward:

Opportunity to create distinctive brand image

•

Year-round Engagement with the Customer:

Higher

persistency and higher reviewability

•

Potential to Increase Profitability

•

Data Analytics & Better Risk Management

For the Insurer

•

Administration Complexity

•

Huge Expenses involved in the Setup, Marketing,

Sales Training

•

Anti-Selection Risk

•

Low Take Up Rate

•

Pricing Challenges

www.actuariesindia.org

13

Pricing Approaches –

Considerations &

Challenges

www.actuariesindia.org

14

•

Buildup

•

Density

•

Tabular

•

Stochastic

•

Linear

Pricing

Approaches

Measure the Past

Evaluate &

Normalize to

Baseline

Project to Future

Expectations

All methods follow the same process:

Pricing Approaches

www.actuariesindia.org

15

Pricing Components in Health - Sample

Categories

Strategic plan and profit goals.

Existing products: expectations, rate philosophy, experience.

Regulation: IRDAI, pricing, actuarial standards

Distribution : impact on customer behavior

Claims Adjudication Systems (TPA vs In-House).

The market: competitive and pricing pressure.

www.actuariesindia.org

16

Rating Happens Within a Context

www.actuariesindia.org

17

Experience Rating (group)

& Projected Loss Ratio

Methods (individual).

Few with credible data use

GLM approaches.

Very few apply global

benchmarks and adjust for

local market conditions.

New players rely on

competitors rates and

secondary research.

1

2

3

4

Current Market Pricing Approaches

www.actuariesindia.org

18

Actuarial Pricing Challenges

www.actuariesindia.org

19

Actuarial Pricing Challenges

www.actuariesindia.org

20

Poor

Information

Risk

Volatility

Competitive

Market

Internal

Issues

Time

Pressure

•

Limited exposure period.

•

Incomplete or inaccurate data.

•

IBNR.

•

No time for deep interrogation

of data.

•

Medical inflation

•

Catastrophic claims (historic

& expected).

•

Developing markets (trends

are harder to predict).

•

Changes in benefits &

demographics.

•

Buying business & irrational

pricing.

•

Churning.

•

Forced credibility.

•

Conflicts of interest (e.g.

Revenue v Profit).

•

Poor quality tools &

systems.

•

Experience & skill

shortages.

The Underwriter’s Challenge

w

w

w

.

a

c

t

u

a

r

i

e

s

i

n

d

i

a

.

o

r

g

21

21

Limited actuarial evidence of customer gains with respect to some add ons (such as wellness

programs, gym membership etc).

Limited needs analysis at design stage (appears to be a mimic from other

markets).

Limited interaction with underwriting and claims adjudication teams (lack of

clinical and actuarial synergies).

Lack of market maturity and hence scarcity of data in pricing for these

benefits.

Lack of robust IT platforms (actuarial and clinical) in monitoring

experience.

Health care is one of the most promising sector of the Indian Economy.

Conclusions

Customers have high perceived value for such benefits. Hence, huge potential for

Insurers.

Explore the viability and customer benefits of value added benefits in health insurance from an actuarial perspective at the 28th India Fellowship Seminar. The Indian healthcare industry's growth prospects, policy support, and the role of health insurance are discussed, highlighting the opportunities and challenges in pricing approaches. With a strong focus on public interest, the seminar delves into the evolving landscape of healthcare services in India.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. Download presentation by click this link. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

E N D

Presentation Transcript

28th India Fellowship Seminar Value added benefits in health insurance an actuarial perspective to the viability and are they worth for the customers Guide Name: A V Karthikeyan Presenters Name: 1. Swati Anil Umre 2. Mansi Kukreja 3. Safder Jaffer Date: 09 November 2017 Mumbai Indian Actuarial Profession Serving the Cause of Public Interest

Agenda Introduction to the Indian Healthcare Industry Defining Value Added Benefits Benefits and Limitations: For the Customer Benefits and Limitations: For the Insurer Pricing Approaches: Risks & Challenges Associated With Pricing Conclusions 2 www.actuariesindia.org

Health care is one of the most promising sectors of the Indian economy Salient features of Indian healthcare industry Policy support vv Strong fundamentals Cost advantage Fifth largest employer Impressive growth prospects Low cost of medical services has resulted in a rise in the country s medical tourism, attracting patients from across the world Conducive policies encouraging FDI, tax benefits, favourable government policies coupled with promising growth prospects have helped the industry attract private equity, venture capitals and foreign players India is expected to rank amongst the top three healthcare markets in terms of incremental growth by 2020* Increasing income levels, ageing population, growing health awareness and changing attitude towards preventive healthcare is expected to boost healthcare services demand in future Indian healthcare sector is expected to grow at a CAGR of 11% during 2015 20 to reach US$176 billion by 2020^ Medial tourism in India is expected to grow at 20-25%* per annum based on government data In 2015, Indian healthcare sector became the fifth largest employer, both in terms of direct as well as indirect employment, with total direct employment of over 47 crores people* There is significant scope for improving healthcare services availability in India which offers ample opportunity for development of the healthcare industry 3 4 5 www.actuariesindia.org 1 2 Availability of a large pool of well trained medical professionals in the country is expected to provide the necessary support India has emerged as a hub for R&D activities for international players due to its relatively low cost of clinical research Creation of National Health Insurance Mission to provide health benefits to people Source: * IBEF ^ World Health Organization (WHO), BMI 3

Overview of the Indian health insurance market IRDAI licensed health insurance Self funded schemes Group Retail Group health insurance cover (either employer- employee or non employer- employee (like holders of the same credit card, etc.) Many governmental and public sector institutions, as well as some private corporates (e.g. Unilever, P&G) have self-funded health insurance schemes Certain government schemes are self-funded as well 4 public sector, 18 private sector general insurers that can sell health insurance 6 stand-alone health insurers with Aditya Birla as a new entrant in 2016 Few life insurance players* provide health insurance such as LIC Individual or family floater Tax benefit under section 80D Government Sponsored Segments Players RSBY (Rashtiya Swasthiya Bima Yojana) Other State sponsored insurance schemes Indian Health Insurance sector Personal Accident* Limited Indemnity Third party Agency Products Channels Loss of life due to accident Permanent temporary disability Brokers Bancassurance Corporate agents Web aggregators Reimbursement against the costs of medical expenses Direct payment to provider as an option, known as cashless Traditional agents Variable agency model and Online/Digital Critical Illness* Overseas Travel* Direct / Telesales Lump sum payment on diagnosis of one of the specific life threatening illness Website sales Tablet / mobile app Aggregators E-commerce tie ups Direct sales staff Call-centre Overseas Mediclaim insurance Loss of flight & luggage Add on coverages (e.g. Dental) * Not a significant portfolio Category accounts for major share of the segment www.actuariesindia.org

Complementing the growth in healthcare industry, health insurance sector has also experienced an impressive CAGR of ~17% between FY 12-16 Health insurance GWP In INR Bn. 485 244 201 175 155 131 - FY 12 FY 13 FY 14 FY 15 FY 16 FY 20 (P) Key growth drivers for health insurance Regulatory reforms and tax incentives Increasing Healthcare costs Increased Awareness High out of pocket expenditure Technology New technologies disrupting health insurance Insurers launching mobile apps & internet based services Recognition of Health insurance as a standalone class; allowing more opportunities through open architecture Increase in tax benefits in 80D from 15K to 25K Healthcare expenditures continue to rise as the government modernizes India s healthcare system Increasing awareness of health insurance and growing perception of insurance needs among people, evidenced by ~21% growth in the retail health insurance 62% per cent of the total health care expenditure in the country was borne by households out of their pockets in 2014 3 4 5 1 2 www.actuariesindia.org Source: WHO Study; IRDA Annual reports

Health insurance products falls under two main categories Limited indemnity Fixed benefit 10% 90% In-patient cover Hospital cash Covers hospital treatment that requires a stay of one or more nights Pays an assured amount for days spent in hospital irrespective of type and amount of the bill 01 06 Surgical cash Out-patient (OPD) Pays for any in-patient or day surgery, depending on the severity of the operation and typical recovery period Health Insurance Products Covers hospital treatment that doesn t requires an overnight stay 05 02 Health + Savings Critical illness Health insurance that rewards you with saving points on adoption of healthy practices Provides lump-sum benefit on diagnosis of Critical Illness / Major Medical Illnesses and procedures 04 03 In India, currently 90% of health insurance products are indemnity but fixed benefit products have started gaining traction in recent times www.actuariesindia.org

Value Added Benefits in Health Insurance Maternity benefit Dental cover Restoration Wellness programs Cover for all the expenses involved in the delivery of a child and/or expenses related to medically necessary and lawful termination of pregnancy. 1 Reimbursement of medical expenses incurred in connection with treatment of any injury or illness to natural tooth/teeth. Reinstatement of 100% of Sum Insured (once in a policy year) if the claim is not related to the illness for which a claim has been made earlier in the year. 3 To promote, incentivise and reward the policyholder for his healthy behaviour through various wellness services. 4 www.actuariesindia.org 2 7

Are Value Added Benefits Worth for the Customers and Insurance Companies? www.actuariesindia.org 8

The KANO Analysis for ever changing customer needs DELIGHTERS Wellness Coach Gym Membership Health Checkups Health Reward Points Air Ambulance EXPECTATION Hospitalization Benefits Quick Claim settlement Outpatient Treatment 24 * 7 helpdesk Road Ambulance Satisfying Basic Needs Satisfying Performance Needs Satisfying Excitement Needs Allows a company to sustain and remain competitive Allows a company to excel and be world class Allows a company to get into the market www.actuariesindia.org 9

For the Customer Perceived Satisfaction: More delighters, higher satisfaction Motivation to Stay Fit Lifestyle Disease Management Access to more Appropriate Care Low Utilization risk Onerous T&C - Complexity in Understanding Data Security and Privacy issues www.actuariesindia.org 10

What does Regulation Says? Insurers must factor such costs into the product pricing Wellness and preventive elements as part of product design a) Using health services like Ensure How Encourages Outpatient consultations Pharmaceuticals Health Check-ups b) Offer discounts on renewal premiums based on the fitness and wellness criteria www.actuariesindia.org 11

For the Insurer Way Forward: Opportunity to create distinctive brand image Year-round Engagement with the Customer: Higher persistency and higher reviewability Potential to Increase Profitability Data Analytics & Better Risk Management Administration Complexity Huge Expenses involved in the Setup, Marketing, Sales Training Anti-Selection Risk Low Take Up Rate Pricing Challenges www.actuariesindia.org 12

Pricing Approaches Considerations & Challenges www.actuariesindia.org 13

Pricing Approaches Advanced Buildup Density Tabular Basic Pricing Approaches Stochastic Linear All methods follow the same process: Evaluate & Normalize to Baseline Project to Future Expectations Measure the Past www.actuariesindia.org 14

Pricing Components in Health - Sample Categories Non-Maternity Hospital Physician Other Inpatient/Outpatient Medical Surgery Prescription Drugs Inpatient/Outpatient Surgical Anesthesia PDN/Home Health Observation Wellness Exams Ambulance Office Visites Appliances Other Diagnostics/Radiology www.actuariesindia.org 15

Rating Happens Within a Context The market: competitive and pricing pressure. Existing products: expectations, rate philosophy, experience. Distribution : impact on customer behavior Claims Adjudication Systems (TPA vs In-House). Regulation: IRDAI, pricing, actuarial standards Strategic plan and profit goals. www.actuariesindia.org 16

Current Market Pricing Approaches Very few apply global benchmarks and adjust for local market conditions. Experience Rating (group) & Projected Loss Ratio Methods (individual). 4 1 3 2 New players rely on competitors rates and secondary research. Few with credible data use GLM approaches. www.actuariesindia.org 17

Actuarial Pricing Challenges Lack of data granularity to price from first principles. Thin experience new products. Lack of underwriting data from existing products. Lack of clinical coding. Lack of synergy between actuarial and clinical teams. Market competition cross subsidy. Rates rationalisation. Lack of sufficient longitudinal data for durational impact analysis. Scarcity of experience resource. Internal coordination and approvals on benefit design. Unable to keep pace with the increasing medical costs due to lag in filing & approvals. www.actuariesindia.org 18

Actuarial Pricing Challenges Understanding medical trends for add-on benefits. Lack of understanding of adverse selection and selective lapsing. Quantifying moral hazard from Providers and Policyholders. Quantifying disease burden from changing lifestyle. www.actuariesindia.org 19

The Underwriters Challenge No time for deep interrogation of data. Limited exposure period. Incomplete or inaccurate data. IBNR. Time Pressure Poor Information Conflicts of interest (e.g. Revenue v Profit). Poor quality tools & systems. Experience & skill shortages. Medical inflation Catastrophic claims (historic & expected). Developing markets (trends are harder to predict). Changes in benefits & demographics. Internal Issues Risk Volatility Competitive Market Buying business & irrational pricing. Churning. Forced credibility. www.actuariesindia.org 20

Conclusions Health care is one of the most promising sector of the Indian Economy. Customers have high perceived value for such benefits. Hence, huge potential for Insurers. Limited needs analysis at design stage (appears to be a mimic from other markets). Lack of market maturity and hence scarcity of data in pricing for these benefits. Lack of robust IT platforms (actuarial and clinical) in monitoring experience. Limited interaction with underwriting and claims adjudication teams (lack of clinical and actuarial synergies). Limited actuarial evidence of customer gains with respect to some add ons (such as wellness programs, gym membership etc). www.actuariesindia.org 21