Understanding Marketing in Banking Industry

Marketing in the banking sector involves helping customers with various financial services like account operations, transfers, loans, and forex. Acquiring, retaining, and growing customer relationships is key, understanding their needs and preferences. Mobile and net banking have emerged as popular choices. Relationship managers play a crucial role in offering personalized services, from opening accounts to handling investments and utility bill payments, providing doorstep convenience.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. Download presentation by click this link. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

E N D

Presentation Transcript

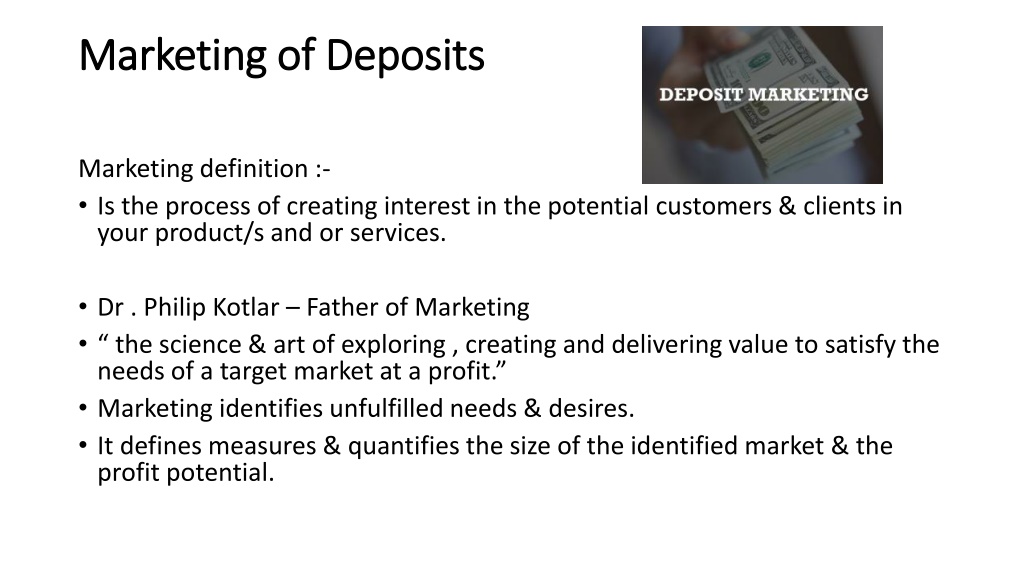

Marketing of Deposits Marketing of Deposits Marketing definition :- Is the process of creating interest in the potential customers & clients in your product/s and or services. Dr . Philip Kotlar Father of Marketing the science & art of exploring , creating and delivering value to satisfy the needs of a target market at a profit. Marketing identifies unfulfilled needs & desires. It defines measures & quantifies the size of the identified market & the profit potential.

Principles of Marketing Seven P formula Product nature , innovation , acceptability Price competitive homework, acceptable Promotion reach target group , advertisement, (print-electronic); brochure; hoardings etc. Place Requirement of the place; geographical & demographic study. Packaging Debit card ICICI Bank , Attractive, convenient. Positioning Efforts to reach customers, time period of launch; (vehicle loans in festivals). People Target group ; Teachers for consumer loan ; police for vehicle loans identify needs of a group.

Difference Selling Marketing Needs of the seller Needs of Buyer Products into cash Satisfy needs of the buyer. Goods producing process Customer satisfying process. Involves Push strategy Marketing is more pull than push. To find customer for the product. To find the right product for your customer.

Products need to change as per times Warren Buffet $84.8 Billion $67.40 Billion $103.9 Billion $93.90 Billion $38.40 Billion $114.00 Billion $64.80 Billion Investment a) HMT watches ; Swiss watches Japan , Korea, china. Nokia mobiles market share 80% down Bajaj two wheelers market share declined & captured by Honda. List of rich persons changed shift of focus Mark Zuckerberg Bill Gates I.T. Facebook b) I.T. Microsoft c) Bernard Arnaut Jack Ma Investment d) I.T. Alibaba Jeff Bezos Amazon Larry Ellison Oracle Comp. I.T. Rothshilds , Morgans , Rockfellers are behind.

Marketing in Banking Helping customer/s to open &operate accounts ; making transfers, availing various loans, forex requirements etc. Marketing in Banks aims at Acquiring, Retaining & Growing Customers. Customer as human being have needs, wants, demands and desires . To start with we should understand these needs. Mobile and Net Banking becoming most popular.

Relationship managers i. ii. iii. Account opening scanning of KYC documents photo , signature need not go to branch. iv. Debit card ; Credit card; Investment plans, personal loans; Travels- forex; everything is taken care. v. Payment of utility bills online. Create a customer base. High value customers. All their requirements door step service.

Investment Avenues Real estate gloomy market ; stock of unsold flats and houses; no immediate prospects. Share Market Volatile; Mutual Funds-SIPs. Gold prices stationary for last 3 years now prices are 39000/-+; Limitations of Pan card for 1lac or more; No recurring income; Risk of theft; Wealth Tax ; Ornaments making charges. Insurance no surrender value for 5 years; premature encashment return very low; Risk cover lesser returns; medical insurance.

Deposits Demand & Time. Types of deposit A/Cs to suit individual requirements. Current Accounts Traders, Businessmen, Professionals Saving Account Individuals ,Housing societies, HUF etc. Monthly Income Depo. Pensioners; Sr. citizens. Reinvestment - Time bound requirements. Recurring - Periodical requirements. Quarterly Int. Pay-out Fixed Deposit.

Strengths of Deposits Premature encashment Loan up to 90% of deposit. Overdraft against deposit. Age old popular investment. Fixed contracted Interest Rate. Any period from 7 days to 10 years. HCs and B.Gs can be availed Margin. DICGC Cover up to 1 lac.

Challenges in Marketing Deposits i. ii. iii. TDS- on int. pay out 10000/-plus. iv. Form 15H &15-G. v. Competition of SIP. vi. Co-op. Banks Risk element. Competitive rate of interest Deposits out of savings A/C.

Marketing CASA Deposits Demand Deposits in nature. Financial strength depends on % of CASA. Higher the % better is the profitability. CASA deposits affect Net Interest Margin (NIM). Special efforts required for CASA. Door to Door campaigning- Package to salary earners- Current A/C No cheque book charges, Remittance at par Debit card email A/C statement. Selected CASA accounts Accident Insurance Increase in % of CASA cost of funds decreases profitability increases 0 Competitive lending rates possible.

Widening Customer Base i. ii. iii. iv. v. vi. vii. Enunciate importance of savings . viii. Financial advice to technocrats. ix. Use of clubs such as Rotary, Lions etc. x. Celebrate your foundation day call customers over a cup of tea. xi. Ganesh Chaturthi, Haldi kunku programmes. xii. Teachers day; Engineers Day, Doctors Day etc. xiii. All employees to work as TEAM . xiv. Senior citizens health camps computer awareness programmes. Study of command Area Residential/Commercial. Obtain lists of Doctors, CA, Engineers, Teachers etc. Ensure requirements of present client s met. Satisfied existing customer can help to generate leads. Banking awareness campaign amongst workers. Mock banking counters for Primary & High Schools.

Self Help Groups a) b) c) d) e) f) g) National priority Urban Semi urban Villagers. Minimum 10 women to form group. Choose Secretary; Chairman, Treasurer. Develop Savings habit get togethers. Develop market for their products. Exhibitions can be arranged at regular intervals. Scheme of Financing Marketing Education Training be approved by NABARD. Expenses for training, Exhibitions etc. are compensated by NABARD. Sizable CASA Good advances Excellent Recovery. Low Costing Housing Loans. h) i) j)

Know your Bank Financially Sound Well Managed FSWM Bank Net worth of the Bank positive CRAR- Capital to Risk Asset Ratio 10% + NPAs Gross more relevant than Net NPAs lessthan 7%. Profit / Earnings Last 3 years. No defaults in CRR & SLR. Sound internal control system 2 professional Directors on board CAMELS Rating Capital Adequacy, Asset Quality, Management, Earnings, Liquidity & systems. RBI Inspection Grade. FSWM - On site / off site ATMs Branch expansion, Extension- area of operation Shifting of premises etc. Keep latest information regarding deposits & lending rates.

Loan Products Clean Loan Shareholder 50,000 to 5,00,000 Easy process Quick disbursement. reasonable Rate of Interest. Sanctioning Power to Branch Manager. Compare with Pvt. Sector / Nationalized Bank. Most powerful product with good return.

Clean Loan rates & charges Name Of Bank Interest Rate Processing Fees SBI 10.55 TO 14.95 1% HDFC 10.75 TO21.30 2.5% BOB 11.35 TO 16.35 2% AXIS 10.85 TO 24.00 2% ICICI 11.25 TO 22.00 2.25% CANARA 11.35 TO 15.05 0.5% BANDHAN 15.00 TO 16.19 1% KOTAK MAHINDRA 10.99 TO 24.00 2.5% YES BANK 13.99 TO 16.99 2.5%

Vehicle Loans Applicant (most) known to the Bank. page loan application. Simple, Easy & quick appraisal. Reasonable Processing Charges. Bulk/ Group Financing. Police, Government Employees, Pvt. Companies Etc. Disbursement with Function.

Consortium Lending Requirement beyond Exposure Limit. More than one bank to finance. Single window document. Retaining High Value Borrowers. Group Accounts- Salaries etc. Documentation on IBA sight. Lead Bank undertakes appraisal. Lead Bank executes documents D.P. is communicated by Lead Bank. Quaterly Review Meeting.