The Banking System and Money Supply

Topic 6

1

The Banking System and the Money Supply

2

What Counts as Money

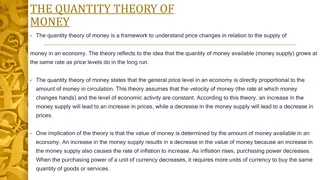

•

Definition of Money

Money is an asset that is widely accepted as a means of payment

•

Only assets—things of value that people own—can be considered as

money

–

Can credit cards be considered as money?

•

Only things that are widely acceptable as a means of payment are

regarded as money

–

Can stocks or bonds be considered as money?

•

Money has two useful functions

–

Provides a unit of account

•

Standardized way of measuring value of things that are traded

–

Serves as store of value

•

One of several ways in which households can hold their wealth

3

Measuring the Money Supply

•

Money Supply

–

Total amount of money held

by the public

•

Governments use different measures of the money supply

–

Each measure includes a selection of assets that are widely

acceptable as a means of payment and are relatively liquid

•

An asset is considered liquid if it can be converted to cash quickly and

at little cost

–

So, an illiquid asset can be converted to cash only after a delay, or at

considerable cost

4

Assets and Their Liquidity

•

Most liquid asset is cash in the hands of the public

•

Next in line are asset categories of about equal liquidity

–

Demand deposits (Checking accounts)

–

Other checkable deposits

–

Travelers checks

•

Then, savings-type accounts

–

less liquid than checking-type accounts, since they do not allow

you to write checks

•

Next on the list are deposits in retail money market mutual

funds

–

Time deposits (called certificates of deposit, or CDs)

•

Require you to keep your money in the bank for a specified period of

time (usually six months or longer)

–

Impose an interest penalty if you withdraw early

5

M1 And M2

•

Standard measure of money stock (supply) is M1

–

Sum of the first four assets in our list

•

M1 = cash in the hands of the public + demand deposits +

other checking account deposits + travelers checks

–

When economists or government officials speak about

“money supply,” they usually mean M1

•

Another common measure of money supply, M2,

adds some other types of assets to M1

–

M2 = M1 + savings-type accounts + retail MMMF

balances + small denomination time deposits

Figure 1: M1 & M2

7

Money Supply

•

We will assume money supply consists of just two

components

–

Cash in the hands of the public and demand deposits

•

Our definition of the money supply corresponds closely to

liquid assets that our national monetary authority—the

Federal Reserve—can control

8

The Banking System: Financial

Intermediaries

•

What are banks?

–

Financial intermediaries—business firms that specialize in

•

Collecting loanable funds from households and firms whose revenues

exceed their expenditures

•

Channeling those funds to households and firms (and sometimes the

government) whose expenditures exceed revenues

•

Intermediaries must earn a profit for providing brokering

services

–

By charging a higher interest rate on funds they lend than rate they

pay to depositors

9

A Bank’s Balance Sheet

•

A balance sheet is a financial statement that provides information

about financial conditions of a bank

at a particular point in time

–

On one side, a bank’s assets are listed

•

Everything of value that it owns

–

Property and buildings

–

Bonds

–

Loans

–

Vault cash

–

Account with the Federal Reserve

–

On the other side, the bank’s liabilities are listed

•

Amounts it owes

–

Deposits

–

Net worth = Total assets – Total liabilities

•

What bank would owe to its owners if it went out of business

–

A balance sheet always balances

10

A Bank’s Balance Sheet

•

Explanations for vault cash and accounts with Federal

Reserve

–

On any given day, some of the bank’s customers might want to

withdraw more cash than other customers are depositing

–

Banks are required by law to hold reserves

•

Sum of cash in vault and accounts with Federal Reserve

•

Required reserve ratio

tells banks the fraction of their

checking accounts that they must hold as required

reserves

–

Set by Federal Reserve

11

Figure 2: The Geography of the

Federal Reserve System

12

Figure 3: The Structure of the

Federal Reserve System

Federal Reserve Functions

•

Issue currency

•

Set reserve requirements

•

Lend money to banks

•

Collect checks

•

Act as a fiscal agent for U.S. government

•

Supervise banks

•

Control the money supply

Federal Reserve Independence

•

Established by Congress as an

independent agency

•

Protects the Fed from political pressures

•

Enables the Fed to take actions to

increase interest rates in order to stem

inflation as needed

15

The Federal Open Market Committee

•

Federal Open Market Committee (FOMC)

–

A committee of Federal Reserve officials that establishes U.S.

monetary policy

•

Consists of all 7 governors of Fed, along with 5 of the 12

district bank presidents

•

Not even President of United States knows details behind

the decisions, or what FOMC actually discussed at its

meeting, until summary of meeting is finally released

–

The FOMC exerts control over nation’s money supply by buying

and selling bonds in public (“open”) bond market

16

The Fed and the Money Supply

•

Suppose Fed wants to change nation’s money supply

–

It buys or sells government bonds to bond dealers, banks, or other

financial institutions

•

Actions are called open market operations

•

We’ll make two

special assumptions

to keep our analysis

of open market operations simple for now

–

Households and business are satisfied holding the amount of cash

they are currently holding

•

Any additional funds they might acquire are deposited in their

checking accounts

•

Any decrease in their funds comes from their checking accounts

–

Banks never hold reserves in excess of those legally required by

law

17

How the Fed Increases the Money

Supply

•

T

o

i

n

c

r

e

a

s

e

m

o

n

e

y

s

u

p

p

l

y

,

F

e

d

w

i

l

l

b

u

y

g

o

v

e

r

n

m

e

n

t

b

o

n

d

s

–

Called an open market purchase

•

Suppose, by writing a check, Fed buys $1,000 bond from

Lehman Brothers, which deposits the total into its checking

account

–

Two important things have happened

•

Fed has injected reserve into banking system

•

Money supply has increased

–

Demand deposits have increased by $1,000 and demand deposits are

part of money supply (for instance, M1)

–

Lehman Brothers’ bank now has excess reserves

»

Reserves in excess of required reserves

»

If required reserve ratio is 10% bank has excess reserves of $900 to

lend

»

Demand deposits increase each time a bank lends out excess

reserves

18

The Demand Deposit Multiplier

•

How much will demand deposits increase in total?

–

Each bank creates less in demand deposits than the bank before

–

In each round, a bank lends 90% of deposit it received

–

So, the total increase in demand deposits is

•

Whatever the injection of reserves, demand deposits will increase by a

factor of 10, so we can write

–

Δ

DD = 10 x reserve injection

19

The Demand Deposit Multiplier

•

For any value of required reserve ratio (RRR), formula for

demand deposit multiplier is 1/RRR

•

Using general formula for demand deposit multiplier, can

restate what happens when Fed injects reserves into

banking system as follows

–

Δ

DD = (1 / RRR) x

Δ

Reserves

•

With the assumption that the amount of cash in the hands

of the public (the other component of the money supply)

does not change, we can also write

–

Δ

Money Supply = (1 / RRR) x

Δ

Reserves

20

How the Fed Decreases the Money

Supply

•

Just as Fed can decrease money supply by selling

government bonds

•

An open market sale

•

Banks have to call in loans in order to meet the required

reserve amount with Fed

•

Process of calling in loans will involve many banks

–

Each time a bank calls in a loan, demand deposits are destroyed

–

Total decline in demand deposits will be a multiple of initial

withdrawal of reserves

–

Using demand deposit multiplier—1/(RRR), we can calculate the

decrease in money supply with the same formula

•

Δ

DD = (1/RRR) x

Δ

reserves

•

This time, the change in reserve is negative

21

Some Important Provisos About the

Demand Deposit Multiplier

•

Although process of money creation and destruction as

we’ve described it illustrates the basic ideas, formula for

demand deposit multiplier—1/RRR—is oversimplified

–

In reality, multiplier is likely to be smaller than formula suggests, for

two reasons

•

We’ve assumed that as money supply changes, public does

not change its holdings of cash

•

We’ve assumed that banks will always lend out all of their

excess reserves

22

Other Tools for Controlling the

Money Supply

•

There are two other tools Fed can use to increase or

decrease money supply

–

Changes in required reserve ratio

–

Changes in discount rate

•

Changes in either required reserve ratio or discount rate

could set off the process of deposit creation or deposit

destruction in much the same way outlined in this chapter

–

In reality, neither of these policy tools is used very often

•

Why are these other tools used so seldom?

–

Partly because they can have unpredictable effects

The Financial Crisis of 2007 and 2008

•

Mortgage Default Crisis

•

Many causes

–

Government programs that

encouraged home ownership

–

Declining real estate values

–

Bad incentives provided by

mortgage-backed bonds

The Financial Crisis of 2007 and 2008

•

Securitization- the process of slicing up

and bundling groups of loans into new

securities

•

As loans defaulted, the system collapsed

•

“Underwater” homeowners abandoned

homes and mortgages

Velocity of Money (V)

25

•

V

e

l

o

c

i

t

y

i

s

a

m

e

a

s

u

r

e

o

f

t

h

e

s

p

e

e

d

m

o

n

e

y

c

h

a

n

g

e

s

h

a

n

d

s

i

n

t

r

a

n

s

a

c

t

i

o

n

s

f

o

r

f

i

n

a

l

g

o

o

d

s

a

n

d

s

e

r

v

i

c

e

s

–

Nominal GDP is the price level (P) times

real GDP (Y)

–

M is the money stock. So,

Velocity in the U.S., 2013

26

•

M1 = $2,638.8 billion

•

M2 = $10,968.3 billion

•

Nominal GDP = $16,768.1 billion

•

Using M1, velocity is 6.35

•

Using M2, velocity is 1.53

•

Velocity is determined by a number of factors

including technology such as ATMs and debit cards

$16,768.1

2,638.8

V =

Money and Inflation in the Long Run

27

•

T

h

e

q

u

a

n

t

i

t

y

e

q

u

a

t

i

o

n

s

t

a

t

e

s

t

h

a

t

m

o

n

e

y

t

i

m

e

s

v

e

l

o

c

i

t

y

e

q

u

a

l

s

n

o

m

i

n

a

l

G

D

P

,

M

x

V

=

P

x

Y

–

Restatement of the velocity definition

•

Shows a relationship between money and price level

–

Suppose velocity and real GDP are constant

•

The quantity equation becomes

–

An increase in the money supply by a given

percentage would increase the price level by the

same percentage

Exploring the concept of money, its functions, what counts as money, measuring the money supply, asset liquidity, and the standard measures M1 and M2 in the context of the banking system and economy.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

You are allowed to download the files provided on this website for personal or commercial use, subject to the condition that they are used lawfully. All files are the property of their respective owners.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.

E N D

Presentation Transcript

Topic 6 The Banking System and the Money Supply 1

What Counts as Money Definition of Money Money is an asset that is widely accepted as a means of payment Only assets things of value that people own can be considered as money Can credit cards be considered as money? Only things that are widely acceptable as a means of payment are regarded as money Can stocks or bonds be considered as money? Money has two useful functions Provides a unit of account Standardized way of measuring value of things that are traded Serves as store of value One of several ways in which households can hold their wealth 2

Measuring the Money Supply Money Supply Total amount of money held by the public Governments use different measures of the money supply Each measure includes a selection of assets that are widely acceptable as a means of payment and are relatively liquid An asset is considered liquid if it can be converted to cash quickly and at little cost So, an illiquid asset can be converted to cash only after a delay, or at considerable cost 3

Assets and Their Liquidity Most liquid asset is cash in the hands of the public Next in line are asset categories of about equal liquidity Demand deposits (Checking accounts) Other checkable deposits Travelers checks Then, savings-type accounts less liquid than checking-type accounts, since they do not allow you to write checks Next on the list are deposits in retail money market mutual funds Time deposits (called certificates of deposit, or CDs) Require you to keep your money in the bank for a specified period of time (usually six months or longer) Impose an interest penalty if you withdraw early 4

M1 And M2 Standard measure of money stock (supply) is M1 Sum of the first four assets in our list M1 = cash in the hands of the public + demand deposits + other checking account deposits + travelers checks When economists or government officials speak about money supply, they usually mean M1 Another common measure of money supply, M2, adds some other types of assets to M1 M2 = M1 + savings-type accounts + retail MMMF balances + small denomination time deposits 5

Money Supply We will assume money supply consists of just two components Cash in the hands of the public and demand deposits Our definition of the money supply corresponds closely to liquid assets that our national monetary authority the Federal Reserve can control 7

The Banking System: Financial Intermediaries What are banks? Financial intermediaries business firms that specialize in Collecting loanable funds from households and firms whose revenues exceed their expenditures Channeling those funds to households and firms (and sometimes the government) whose expenditures exceed revenues Intermediaries must earn a profit for providing brokering services By charging a higher interest rate on funds they lend than rate they pay to depositors 8

A Banks Balance Sheet A balance sheet is a financial statement that provides information about financial conditions of a bank at a particular point in time On one side, a bank s assets are listed Everything of value that it owns Property and buildings Bonds Loans Vault cash Account with the Federal Reserve On the other side, the bank s liabilities are listed Amounts it owes Deposits Net worth = Total assets Total liabilities What bank would owe to its owners if it went out of business A balance sheet always balances 9

A Banks Balance Sheet Explanations for vault cash and accounts with Federal Reserve On any given day, some of the bank s customers might want to withdraw more cash than other customers are depositing Banks are required by law to hold reserves Sum of cash in vault and accounts with Federal Reserve Required reserve ratio tells banks the fraction of their checking accounts that they must hold as required reserves Set by Federal Reserve 10

Figure 2: The Geography of the Federal Reserve System 11

Figure 3: The Structure of the Federal Reserve System 12

Federal Reserve Functions Issue currency Set reserve requirements Lend money to banks Collect checks Act as a fiscal agent for U.S. government Supervise banks Control the money supply

Federal Reserve Independence Established by Congress as an independent agency Protects the Fed from political pressures Enables the Fed to take actions to increase interest rates in order to stem inflation as needed

The Federal Open Market Committee Federal Open Market Committee (FOMC) A committee of Federal Reserve officials that establishes U.S. monetary policy Consists of all 7 governors of Fed, along with 5 of the 12 district bank presidents Not even President of United States knows details behind the decisions, or what FOMC actually discussed at its meeting, until summary of meeting is finally released The FOMC exerts control over nation s money supply by buying and selling bonds in public ( open ) bond market 15

The Fed and the Money Supply Suppose Fed wants to change nation s money supply It buys or sells government bonds to bond dealers, banks, or other financial institutions Actions are called open market operations We ll make two special assumptions to keep our analysis of open market operations simple for now Households and business are satisfied holding the amount of cash they are currently holding Any additional funds they might acquire are deposited in their checking accounts Any decrease in their funds comes from their checking accounts Banks never hold reserves in excess of those legally required by law 16

How the Fed Increases the Money Supply To increase money supply, Fed will buy government bonds Called an open market purchase Suppose, by writing a check, Fed buys $1,000 bond from Lehman Brothers, which deposits the total into its checking account Two important things have happened Fed has injected reserve into banking system Money supply has increased Demand deposits have increased by $1,000 and demand deposits are part of money supply (for instance, M1) Lehman Brothers bank now has excess reserves Reserves in excess of required reserves If required reserve ratio is 10% bank has excess reserves of $900 to lend Demand deposits increase each time a bank lends out excess reserves 17

The Demand Deposit Multiplier How much will demand deposits increase in total? Each bank creates less in demand deposits than the bank before In each round, a bank lends 90% of deposit it received So, the total increase in demand deposits is + + = 900 1000 DD So, + = 1000 1000 DD ( + = 0.9 1 1000 1 1000 + 100 2 + 9 . 0 ) 9 . 0 1000 1000 810 9 . 0 + 729 + + + 2 3 0 9 . 0 + 3 0.9 = = 1 9 . 0 Required Reserve Ratio = 1000 10 = 10000 Whatever the injection of reserves, demand deposits will increase by a factor of 10, so we can write DD = 10 x reserve injection 18

The Demand Deposit Multiplier For any value of required reserve ratio (RRR), formula for demand deposit multiplier is 1/RRR Using general formula for demand deposit multiplier, can restate what happens when Fed injects reserves into banking system as follows DD = (1 / RRR) x Reserves With the assumption that the amount of cash in the hands of the public (the other component of the money supply) does not change, we can also write Money Supply = (1 / RRR) x Reserves 19

How the Fed Decreases the Money Supply Just as Fed can decrease money supply by selling government bonds An open market sale Banks have to call in loans in order to meet the required reserve amount with Fed Process of calling in loans will involve many banks Each time a bank calls in a loan, demand deposits are destroyed Total decline in demand deposits will be a multiple of initial withdrawal of reserves Using demand deposit multiplier 1/(RRR), we can calculate the decrease in money supply with the same formula DD = (1/RRR) x reserves This time, the change in reserve is negative 20

Some Important Provisos About the Demand Deposit Multiplier Although process of money creation and destruction as we ve described it illustrates the basic ideas, formula for demand deposit multiplier 1/RRR is oversimplified In reality, multiplier is likely to be smaller than formula suggests, for two reasons We ve assumed that as money supply changes, public does not change its holdings of cash We ve assumed that banks will always lend out all of their excess reserves 21

Other Tools for Controlling the Money Supply There are two other tools Fed can use to increase or decrease money supply Changes in required reserve ratio Changes in discount rate Changes in either required reserve ratio or discount rate could set off the process of deposit creation or deposit destruction in much the same way outlined in this chapter In reality, neither of these policy tools is used very often Why are these other tools used so seldom? Partly because they can have unpredictable effects 22

The Financial Crisis of 2007 and 2008 Mortgage Default Crisis Many causes Government programs that encouraged home ownership Declining real estate values Bad incentives provided by mortgage-backed bonds

The Financial Crisis of 2007 and 2008 Securitization- the process of slicing up and bundling groups of loans into new securities As loans defaulted, the system collapsed Underwater homeowners abandoned homes and mortgages

Velocity of Money (V) Velocity is a measure of the speed money changes hands in transactions for final goods and services Velocity = Nominal GDP Money stock Nominal GDP is the price level (P) times real GDP (Y) M is the money stock. So, V = P x Y M 25

Velocity in the U.S., 2013 M1 = $2,638.8 billion M2 = $10,968.3 billion Nominal GDP = $16,768.1 billion Using M1, velocity is 6.35 $16,768.1 $16,768.1 2,638.8 2,638.8 V = V = = 6.35 Using M2, velocity is 1.53 $16,768.1 10,968.3 V = = 1.53 Velocity is determined by a number of factors including technology such as ATMs and debit cards 26

Money and Inflation in the Long Run The quantity equation states that money times velocity equals nominal GDP, M x V = P x Y Restatement of the velocity definition Shows a relationship between money and price level Suppose velocity and real GDP are constant The quantity equation becomes v and Y , respectively M x V = P x Y An increase in the money supply by a given percentage would increase the price level by the same percentage 27

")