Strategic Decision of Share Buyback in Corporate Finance

A buy-back is when a company repurchases its own shares, providing value to shareholders and optimizing its capital structure. It can be done via existing shareholders, the open market, or employee schemes. Changes in tax laws, effective from 1st Oct

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

You are allowed to download the files provided on this website for personal or commercial use, subject to the condition that they are used lawfully. All files are the property of their respective owners.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.

E N D

Presentation Transcript

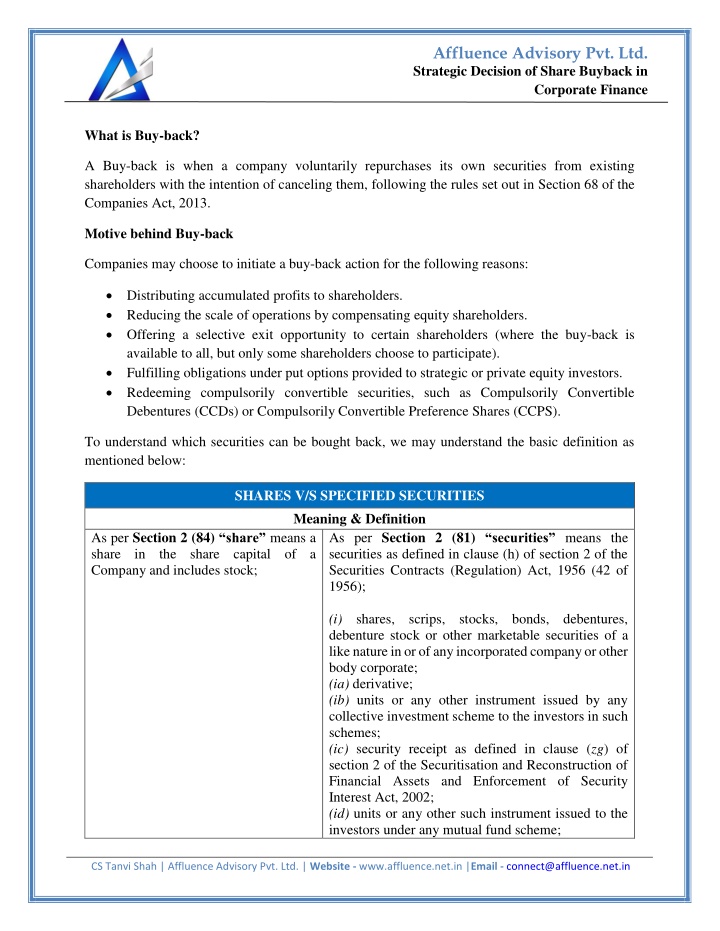

Affluence Advisory Pvt. Ltd. Strategic Decision of Share Buyback in Corporate Finance What is Buy-back? A Buy-back is when a company voluntarily repurchases its own securities from existing shareholders with the intention of canceling them, following the rules set out in Section 68 of the Companies Act, 2013. Motive behind Buy-back Companies may choose to initiate a buy-back action for the following reasons: Distributing accumulated profits to shareholders. Reducing the scale of operations by compensating equity shareholders. Offering a selective exit opportunity to certain shareholders (where the buy-back is available to all, but only some shareholders choose to participate). Fulfilling obligations under put options provided to strategic or private equity investors. Redeeming compulsorily convertible securities, such as Compulsorily Convertible Debentures (CCDs) or Compulsorily Convertible Preference Shares (CCPS). To understand which securities can be bought back, we may understand the basic definition as mentioned below: SHARES V/S SPECIFIED SECURITIES Meaning & Definition As per Section 2 (81) securities means the securities as defined in clause (h) of section 2 of the Securities Contracts (Regulation) Act, 1956 (42 of 1956); (i) shares, scrips, stocks, bonds, debentures, debenture stock or other marketable securities of a like nature in or of any incorporated company or other body corporate; (ia) derivative; (ib) units or any other instrument issued by any collective investment scheme to the investors in such schemes; (ic) security receipt as defined in clause (zg) of section 2 of the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002; (id) units or any other such instrument issued to the investors under any mutual fund scheme; As per Section 2 (84) share means a share in the share capital of a Company and includes stock; CS Tanvi Shah | Affluence Advisory Pvt. Ltd. | Website - www.affluence.net.in |Email - connect@affluence.net.in

Affluence Advisory Pvt. Ltd. Strategic Decision of Share Buyback in Corporate Finance (ii) Government securities; (iia) such other instruments as may be declared by the Central Government to be securities; and (iii) rights or interest in securities; Specified securities includes employees stock option or other securities as may be notified by the Central Government from time to time. Method of Buy-back: Under Section 68(5) of the Companies Act, 2013, there are three main methods for a company to buy back its shares or other securities: 1.Existing Shareholders: The Company can buy back shares from its current shareholders based on their existing proportionate ownership. 2.Open Market: This method allows the company to purchase its own shares directly from the stock market. Only available for listed companies. 3.Employee Schemes: The Company can buy back securities issued to its employees under stock option plans or sweat equity schemes. Selective Buy-back: 1.A company can choose to do a selective buy-back, which means it can repurchase shares from specific shareholders or groups. This approach allows for targeted adjustments to the company's capital structure. 2.On the other hand, selective capital reduction isn t permitted. Instead, any reduction in capital must be applied broadly, affecting all shareholders uniformly. This makes selective buy-back a more flexible option for companies looking to make specific changes. Prerequisite for Buy-back a.Companies empowered by Articles of Association. b.Share and Other Specified Securities must be fully paid. c.One year has lapsed from the previous Buy-back offer. d.The default has been corrected, and three years have passed since the issue was resolved. e.The Debt-equity ratio cannot exceed 2:1. f.The total amount allocated for the buy-back cannot surpass 25% of the company s paid-up share capital and free reserves. CS Tanvi Shah | Affluence Advisory Pvt. Ltd. | Website - www.affluence.net.in |Email - connect@affluence.net.in

Affluence Advisory Pvt. Ltd. Strategic Decision of Share Buyback in Corporate Finance g.Additionally, the maximum number of equity shares that can be repurchased within a financial year must not exceed 25% of the total paid-up equity capital for that year. Condition Subsequent to Buy-back: a.The debt-to-equity ratio after the buy-back must not exceed 2:1. b.The company cannot make another buy-back offer within one year from the closing date of the previous buy-back offer. c.The company is prohibited from issuing or allotting the same type of securities that were bought back for a period of 6 months, except in cases of bonus issues or to meet existing obligations like the conversion of warrants, stock options, sweat equity, or preference shares/debentures into equity shares. Sources of Buy-back: a.Free Reserves; b.Securities Premium account; or c.Proceeds of the issue of any shares or other specified securities but not through proceeds from the issuance of equity shares of the same class. As per Section 2 (43) free reserves means such reserves which, as per the latest audited balance sheet of a company, are available for distribution as dividend: Provided that i. Any amount representing unrealized gains, notional gains or revaluation of assets, whether shown as a reserve or otherwise, or any change in carrying amount of an asset or of a liability recognized in equity, including surplus in profit and loss account on measurement of the asset or the liability at fair value, shall not be treated as free reserves; ii. Course of action for Buy-back Step Action Details 1. Board Meeting Convene a Board Meeting by giving notice to all directors as per Section 173 of the Companies Act, 2013. Pass the necessary resolution to approve the notice of the general meeting and the letter of offer for the buy-back. Note: The Explanatory Statement under Section 102, attached to the general meeting notice, must disclose the particulars specified in Section 68(3) and Rule 17(1). CS Tanvi Shah | Affluence Advisory Pvt. Ltd. | Website - www.affluence.net.in |Email - connect@affluence.net.in

Affluence Advisory Pvt. Ltd. Strategic Decision of Share Buyback in Corporate Finance 2. Filing MGT-14 Form Submit Form MGT-14 to the Registrar of Companies within 30 days of passing the board resolution. 3. General Meeting Convene a General Meeting to pass the special resolution for buy- back. Submit Form MGT-14 to the Registrar of Companies within 30 days of passing the resolution. 4. Letter of Offer (Form SH.8) File the letter of offer in Form SH.8 with the Registrar of Companies. Ensure the letter is dated and signed by at least two directors, one of whom must be the Managing Director, if applicable. 5. Declaration of Solvency (Form SH.9) File a Declaration of Solvency in Form SH.9 with the Registrar of Companies and SEBI (if the company is listed). The declaration must be verified by an affidavit as prescribed in Section 68(6) and signed by at least two directors, including the Managing Director, if any. 6. Dispatch Letter of Offer Send the Letter of Offer to shareholders/security holders within 21 days of filing it with the Registrar of Companies, ensuring compliance with Rule 17(10) of the Companies (Share Capital and Debentures) Rules, 2014. 7. Offer Period The buy-back offer must remain open for a minimum of 15 days and a maximum of 30 days from the date of dispatch of the Letter of Offer. 8. Proportionate Acceptance If the shares or securities offered exceed the total number to be bought back, acceptance per shareholder/security holder will be on a proportionate basis. 9. Verification of Offers Complete the verification of offers received within 15 days from the date of closure of the offer. 10. Bank Account Immediately after the offer closes, open a separate bank account and deposit the total sum due for the buy-back consideration. 11. Payment Return Securities and of Within 7 days of offer verification: i.Pay the buy-back consideration in cash to shareholders/security holders whose offers have been accepted. ii.Return the share certificates to those whose offers were not accepted or return the balance securities in case of partial acceptance. 12. Extinguishment of Securities Extinguish and physically destroy the bought-back shares or other specified securities within 7 days of the final buy-back completion date. CS Tanvi Shah | Affluence Advisory Pvt. Ltd. | Website - www.affluence.net.in |Email - connect@affluence.net.in

Affluence Advisory Pvt. Ltd. Strategic Decision of Share Buyback in Corporate Finance 13. Return of Buy- back SH.11) File the Return of Buy-back with the Registrar of Companies and SEBI (if listed) in Form SH.11 within 30 days of completing the buy- back. Include a certificate in Form SH.15 signed by two directors, one of whom must be the Managing Director, if any, confirming compliance with the Act and rules. (Form 14. Register Bought-back Securities (Form SH.10) of Maintain a register of bought-back shares/securities in Form SH.10 at the company s registered office. This register should be in the custody of the Company Secretary, or another person authorized by the Board, with entries authenticated by the authorized person. Consent required for Buyback of Shares and other Specified Securities: Board Resolution up to 10% of total paid-up equity share capital and free reserves. Shareholders approval through Special Resolution - beyond the limit of 10%, but within the limit of 25% as discussed separately herein. Note: The limits must be evaluated on a standalone basis. Determination of Buy-back Offer price: The Companies Act, 2013 does not specify the method for determining the buyback price. However, it requires that the buyback price and the basis for its calculation be clearly stated. In our opinion, the purpose of a buyback is to return value to the shareholders who are exiting. Therefore, the price should reflect the fair value of the shares. Tax Provisions Effective from 1st October 2024 1. Amendments Related to Share Buybacks (Finance Act, 2024) From 1st October 2024, the following changes will apply to the taxation of share buybacks: a.Deemed Dividend: A new subsection (f) under Section 2(22) treats any payment made by a company to repurchase its own shares, as per Section 68 of the Companies Act, 2013, as a deemed dividend in the hands of the shareholder. b.Exemption Removal: Section 10(34A) now includes a proviso stating that the exemption for income from buybacks will no longer apply to transactions conducted on or after 1st October 2024. CS Tanvi Shah | Affluence Advisory Pvt. Ltd. | Website - www.affluence.net.in |Email - connect@affluence.net.in

Affluence Advisory Pvt. Ltd. Strategic Decision of Share Buyback in Corporate Finance c.Capital Gains Calculation: Under Section 46A, if a shareholder receives any consideration under Section 2(22)(f) for a buyback occurring on or after 1st October 2024, the consideration for computing capital gains will be considered nil. d.Non-Applicability of Section 115QA: Section 115QA, which governs tax implications for companies during buybacks, will not apply to any buybacks occurring on or after 1st October 2024. 2. Summary of Tax Implications a.For the Company: No tax implications will arise for the company due to the inapplicability of Section 115QA(1) from 1st October 2024. b.For Shareholders: The entire buyback consideration will be treated as deemed dividend and taxed at applicable slab rates due to the introduction of Section 2(22)(f). The exemption under Section 10(34A) will no longer apply. For capital gains purposes, the consideration received will be treated as nil, leading to a capital loss equal to the initial acquisition cost. This capital loss can be carried forward and offset against capital gains for up to 8 assessment years (AYs) under Section 74. 3. Shareholder Taxation Under the New Regime a.Applicable Tax Rate: The buyback consideration will be taxed as deemed dividend at the shareholder's applicable slab rate. b.Utilization of Capital Losses: The capital loss arising from the buyback can be carried forward for up to 8 AYs and offset against future capital gains. c.TDS Obligation: TDS on the buyback consideration will apply as per Section 194, at a rate of 10% if the dividend amount exceeds Rs. 5,000. CS Tanvi Shah | Affluence Advisory Pvt. Ltd. | Website - www.affluence.net.in |Email - connect@affluence.net.in

Affluence Advisory Pvt. Ltd. Strategic Decision of Share Buyback in Corporate Finance 4. Applicability Date of the New Buyback Tax Regime: The crucial date for the new buyback tax regime is when the payment or consideration is made or deemed to have been made. CONCLUSION: A buy-back is a corporate action where a company repurchases its own shares or specified securities, following the guidelines of the Companies Act, 2013. It serves multiple purposes, such as returning value to shareholders, reducing capital, and fulfilling specific financial strategies. The process involves various methods and legal prerequisites to ensure compliance. Significant changes in taxation, effective from 1st October 2024, will impact both companies and shareholders, particularly concerning deemed dividends and capital gains. These changes underscore the need for careful planning and adherence to regulatory requirements in buy-back transactions. Disclaimer:This article provides general information existing at the time of preparation and we take no responsibility to update it with the subsequent changes in the law. The article is intended as a news update and Affluence Advisory neither assumes nor accepts any responsibility for any loss arising to any person acting or refraining from acting as a result of any material contained in this article. It is recommended that professional advice be taken based on specific facts and circumstances. This article does not substitute the need to refer to the original pronouncement CS Tanvi Shah | Affluence Advisory Pvt. Ltd. | Website - www.affluence.net.in |Email - connect@affluence.net.in