Recent Developments in Income Tax 2019 Explained by Vivek Jalan

Income Tax 2019 And Recent

Developments

By –

Vivek Jalan

[FCA, LL.B, B.Com (H)]

E-Mail –vivek.jalan@taxconnect.co.in

Call - +91 98315 94980

[ MUMBAI

BANGALORE KOLKATA DELHI]

Change in Tax Rates

Exemptions / benefits that cannot be availed:

No claim set-off of any brought forward loss on account of additional depreciation

for an Assessment

Year for which the option has been exercised and for any subsequent Assessment Year.

tax credit of MAT

paid by a domestic company exercising the option under section 115BAA of the Act

shall not be available consequent to exercising of such option.

Additional initial depreciation allowance @ 20% u/s. 32(1)(iia)

SEZ u/s. 10AA

Tea Development Benefit u/s. 33AB

Site Restoration Benefit u/s. 33ABA

Scientific Research Benefit u/s. 35

Additional Allowance on Scientific Research

Section 32AD (investment in P&M in notified backward areas), 32AB (Investment Deposit Account),

35CCC (Expenditure on Agriculture Extension project), 35CCD (Expenditure on Skill Development

project)

Chapter VI-A Deductions other than Section 80JJAA

Without set off of any loss carried forward from any earlier Assessment Year if such loss is

attributable to any of the above deductions

Option needs to be exercised before filing of return. Once exercised, it cannot be revoked.

Imp Aspects

As there is no timeline within which the option under section 115 BA can be exercised,

it may be noted that

a domestic company with brought forward losses on account of

additional depreciation may, if it so desires exercise the option after setting off the

losses so accumulated.

As there is no timeline within which the option under section 115BAA can be

exercised, it may be noted that a domestic company having MAT credit may, if it so

desires exercise the option after utilising the said credit against the regular tax payable

under the taxation regime existing prior to the promulgation of the Ordinance.

New Manufacturing Companies

Exemptions / benefits that cannot be availed:

Company has been set up & registered on or after 1st October, 2019 and commenced

manufacturing operations on or before 31st March, 2023.

This benefit is available to companies which do not avail any exemption/incentive and

commences their production on or before 31st March, 2023

The Company is not formed by splitting up, reconstruction of a business already in

existence.

The Company does not use any plant & machinery previously used for any purpose.

MAT will not be applicable to such Companies

Pertinent Questions:

What is manufacture

Only New Plant & Machinery to be used

Effective Rates

Domestic Transfer Pricing

TP u/s

92BA

TP u/s

92BA

MAT

Form Of Business

The Finance (No 2) Act 2019, introduced increased surcharge at 25 % & 37 % of income-

tax apply if the total income exceeds INR 2 Cr and INR 5 Cr, respectively. The Ordinance

provides relief from the increased Surcharge in case of a FIIs as referred in section 115AD

of the IT Act, in respect of income from capital gains arising on sale of securities.

The surcharge rate in respect of capital gains covered by section 111A and section 112A

of the IT Act capped at 15 %. The revised surcharge rate is tabulated hereunder:

Surcharge on capital gains

Authorities

-

· A ‘

National e-Assessment Centre

’ to facilitate and centrally control the e-assessment.

· ‘

Regional e-Assessment Centres

’ under the jurisdiction of the regional Principal Chief Commissioner for

making assessment.

· ‘

Assessment units

’ for identifying points or issues, material for the determination of any liability (including

refund), analysing information, and such other functions.

· ‘

Verification units

’ for enquiry, cross verification, examination of books of accounts, witness and recording of

statements, and such other functions.

· ‘

Technical units

’ for technical assistance including any assistance or advice on legal, accounting, forensic,

information technology, valuation, transfer pricing, data analytics, management or any other technical matter.

· ‘

Review units

’ for reviewing the draft assessment order to check whether the facts, relevant evidence and law

and judicial decisions have been considered in the draft order.

All the communications between all the units mentioned above, for the purpose of making an assessment

under this scheme would be through the National e-Assessment Centre.

· The National e-Assessment Centre may at any stage of the assessment, if it considers necessary, transfer the

case to the Assessing Officer having jurisdiction over such case

Faceless Assessments

Change brought by FA 2019 u/s 115QA of IT Act -

Individual has subscribed to a company in IPO stage at Rs.100/-

The company announced a buyback at Rs 500

The company would pay the buyback tax at 20 % on Rs 400

Earlier –

The individual would have paid LTCG at 10% or STCG @ 15% on Rs 400 in listed

companies.

This amendment is effective from 5 July 2019. There were instances where public

announcement for buy-back were made before 5 July 2019 but necessary approvals received

post 5 July 2019. Such cases also came within the ambit of section 115QA of the IT Act and

would be subject to buy-back tax. In order to give relief to such cases, the Ordinance has

inserted a proviso to section 115QA of the IT Act to provide that the buy-back tax shall not

apply to listed Companies where public announcement with respect to buy-back was made

before 5 July 2019.

Grandfathering

of Tax on Buy Back of Shares

CBDT notified the Income-tax Authorities which shall exercise and perform, concurrently,

the powers and functions of Assessing Officer, to facilitate the conduct of

E-assessment

proceeding in a centralised manner in respect of returns furnished under Section 139 or

in response to notice under Section 142 (1) during any financial year commencing on or

after 1st day of April, 2018

All authorities are head quartered in New Delhi

N No 72/2019 dated 23

rd

Sep.

CBDT notifies Additional depreciation on motor Car and Motor vehicles i.e. 15% to 30%

and 30% to 45% respectively, acquired on or after the 23rd day of August, 2019 but

before the 1

st

day of April, 2020 and is put to use before the 1

st

day of April, 2020

N No 69/2019 dated 23

rd

Sep.

CBDT notifies tolerance range for wholesale trading & for other cases for AY 19-20 w.r.t.

the calculation of arm length price related to International transaction determined as per

section 92C i.e. 1% in case of wholesale trading and 3% in other cases

For the purposes of this notification, “

wholesale trading

” means an international

transaction or specified domestic transaction of trading in goods, which fulfils the

following conditions, namely:-

(i) purchase cost of finished goods is eighty per cent. or more of the total cost

pertaining to such trading activities; and

(ii) average monthly closing inventory of such goods is ten per cent. or less of sales

pertaining to such trading activities.

N No 64/2019 dated 13

th

Sep.

CBDT as a one-time measure provides relaxation of time filling of compounding

application, with a view to mitigate unintended hardship to taxpayers in deserving cases,

and to reduce the pendency of existing prosecution cases before the courts

Cir 25/2019 – Relaxation for Compounding

CBDT lays down the procedure to identify & process Income Tax cases for prosecution in

respect of certain Income Tax related offences such as Failure to pay tax to the credit of

Central Government, Failure to pay the tax collected at Source, Wilful attempt to evade

tax, etc.

i.

Offences u/s 276B:

Failure to pay tax to the credit of Central Government under

Chapter XII-D or XVII-B.

ii.

Offences u/s 276BB:

Failure to pay the tax collected at Source

iii.

Offences u/s 276C(1):

Wilful attempt to evade tax, etc.

iv.

Offences u/s 276CC:

Failure to furnish returns of income.

Cir 24/2019 – Relaxation for Compounding

Appeal filing limit not applies to cases of Bogus LTCG / STCG-Exception to monetary limits

for filing appeals specified in any Circular issued under Section 268A. Similar instructions

has been issued vide instructions no. F. No. 279/Misc./M-93/2018-ITJ(Pt.) dated 16th

September 2019.

Appeals may be filed on merits as an exception to said circular, where Board, by way of

special order direct filing of appeal on merit in cases involved in organised tax evasion

activity

Cir 23/2019 – Non Filing of Appeals by Dept

Any communication issued manually under the exceptional circumstances as mentioned

has to be

regularised within 15 working days

of its issuance by –

(i) uploading the manual communication on the systems

(ii) Compulsorily generating the DIN on the Systems

(iii) Communicating the DIN so generated to the assessee/any other person as per

electronically generated proforma available on the Systems

ITBA Inst 3: Regularizing of Manual Letters

Functionality for processing of returns having refund claims which were not processed within

the time allowed u/s 143(1) due to some technical or other reasons has been issued

Pre-Conditions:

(i) Valid return for the assessment years is filed under permitted time limit u/s 139 or 142(1).

(ii) Assesse has claimed refund in return of income.

(iii) On computation, the resultant outcome is refund.

(iv) The returns of income should not have been remained unprocessed due to any reason attributable to the

concerned assessee.

(v) The returns of income should not be under Scrutiny assessment in view of provisions of sub- section (1D) of

section 143 of the Act.

Processes to be followed:

(i) Prior administrative approval of concerned Pr.CCIT/CCIT must be obtained for processing of such eligible time-

barred returns.

(ii) Once administrative approval is accorded by the concerned PCCIT/CCIT, the concerned Pr.CIT/CIT would make

reference to the Pr. DGIT (Systems), to provide necessary enablement in system to the assessing officer on case

to case basis.

143(1) Not Issued Cases

Seeks to raise threshold of revenue effect for issue of certificates under section 197/195

needing approval of the

CIT (Intl. Taxation) to Rs. 10 Crore. This threshold will be applicable for

all stations in respect of all applications of non-resident taxpayers either pending as on date or

filed hereafter.

Office Memorandum:

Sec 197 Certificate for NRIs

F. No.279/Misc/M-93/2018-ITJ

No appeal shall be filed in respect of an assessment year or years in which the tax effect is less

than the monetary’ limit specified in para 3.

the revised monetary limits so mentioned is applicable, to all pending SLPs/ appeals/ cross

objections/references. All such pending appeals within the revised limits shall be withdrawn

on or before 31.10.2019

Cir 17/2019 & 3/2018 :

Limit for filing of appeals

THANK YOU

E-

m

ail

-

Vivek.jalan@taxconnect.co.in

Call:

+91 98315 94980

[ MUMBAI

BANGALORE

KOLKATA

DELHI]

Vivek Jalan

[FCA, LL.B, B.Com (H)]

Explore the latest changes in income tax for the year 2019, including new tax rates, exemptions, and important aspects to consider. Learn about Section 115BAA for all companies and Section 115BAB for new manufacturing companies, with detailed insights on tax rates, surcharges, and key regulations. Find out how to navigate these recent developments effectively and make informed decisions for your financial planning.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. Download presentation by click this link. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

E N D

Presentation Transcript

Income Tax 2019 And Recent Developments By Vivek Jalan [FCA, LL.B, B.Com (H)] E-Mail vivek.jalan@taxconnect.co.in Call - +91 98315 94980 [ MUMBAI BANGALORE KOLKATA DELHI]

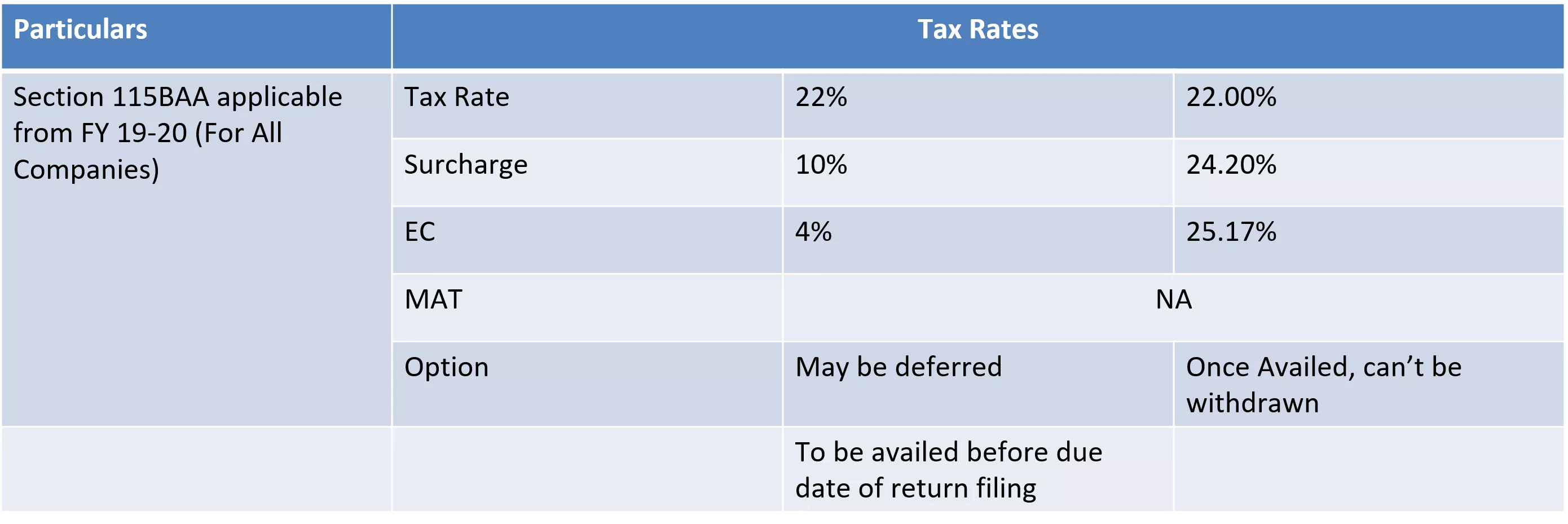

Change in Tax Rates Particulars Tax Rates Section 115BAA applicable from FY 19-20 (For All Companies) Tax Rate 22% 22.00% Surcharge 10% 24.20% EC 4% 25.17% MAT NA Option May be deferred Once Availed, can t be withdrawn To be availed before due date of return filing

Exemptions / benefits that cannot be availed: No claim set-off of any brought forward loss on account of additional depreciation for an Assessment Year for which the option has been exercised and for any subsequent Assessment Year. tax credit of MAT paid by a domestic company exercising the option under section 115BAA of the Act shall not be available consequent to exercising of such option. Additional initial depreciation allowance @ 20% u/s. 32(1)(iia) SEZ u/s. 10AA Tea Development Benefit u/s. 33AB Site Restoration Benefit u/s. 33ABA Scientific Research Benefit u/s. 35 Additional Allowance on Scientific Research Section 32AD (investment in P&M in notified backward areas), 32AB (Investment Deposit Account), 35CCC (Expenditure on Agriculture Extension project), 35CCD (Expenditure on Skill Development project) Chapter VI-A Deductions other than Section 80JJAA Without set off of any loss carried forward from any earlier Assessment Year if such loss is attributable to any of the above deductions Option needs to be exercised before filing of return. Once exercised, it cannot be revoked.

Imp Aspects As there is no timeline within which the option under section 115 BA can be exercised, it may be noted that a domestic company with brought forward losses on account of additional depreciation may, if it so desires exercise the option after setting off the losses so accumulated. As there is no timeline within which the option under section 115BAA can be exercised, it may be noted that a domestic company having MAT credit may, if it so desires exercise the option after utilising the said credit against the regular tax payable under the taxation regime existing prior to the promulgation of the Ordinance.

New Manufacturing Companies Corporate tax rate reduced to 15 % for new manufacturing Companies Section 115BAB applicable from 01.10.2019 Newly Set Up Manufacturing Companies) Company set-up and registered on or after 1 October 2019 and commenced manufacturing on or before 31 March 2023 Not formed by splitting up, or the reconstruction, of a business (For All No machinery or plant previously used for any purpose Not engaged in ANY business other than manufacture, research & distribution of any article Company does not avail specified exemptions/ incentives Option Once Availed, can t be withdrawn Tax Rate Basic 15% + Surcharge 10% + EC 4% Total = 17.16% MAT - NA

Exemptions / benefits that cannot be availed: Company has been set up & registered on or after 1st October, 2019 and commenced manufacturing operations on or before 31st March, 2023. This benefit is available to companies which do not avail any exemption/incentive and commences their production on or before 31st March, 2023 The Company is not formed by splitting up, reconstruction of a business already in existence. The Company does not use any plant & machinery previously used for any purpose. MAT will not be applicable to such Companies Pertinent Questions: What is manufacture Only New Plant & Machinery to be used

Effective Rates Total Income (INR) Where turnover in FY 2017-18 does not exceed INR 400 Cr Companies opting to be governed by section 115BAA Companies opting to be governed by section 115BAB Company not covered by (2) to (4) (1) (2) (3) (4) (5) 31.20% (30% + 4% EC) 26.00% (25% + 4% EC) 17.16% 25.168% Upto 1 Cr (15% + 10% SC + 4% EC) (22% + 10% SC + 4% EC) 33.384% 27.82% 25.168% 17.16% 1 Cr 10 (30% + 7% SC + 4% EC) (25% + 7% SC + 4% EC) (22% + 10% SC + 4% EC) (15% + 10% SC + 4% EC) 34.944% 29.12% 25.168% 17.16% Above 10 Cr (30% + 12% SC + 4% EC) (25% + 12% SC + 4% EC) (22% + 10% SC + 4% EC) (15% + 10% SC + 4% EC)

Domestic Transfer Pricing TP u/s 92BA TP u/s 92BA The definition of the Specified Domestic Transaction (SDT) contained in Section 92BA of the IT Act is amended to bring the Companies opting to be covered by section 115BAB within the ambit of Transfer Pricing. Thus, any transactions entered into by newly set up manufacturing company, opting for reduced rate of 15%, with any of its related parties (domestic or otherwise) are to be at Arm s Length. This amendment shall be effective from fiscal year 2019-20.

MAT Total Income (INR) Companies opting to be governed by section 115BA (Not opting for new scheme) Companies opting to be governed by section 115BAA Companies opting to be governed by section 115BAB (1) (2) (3) (4) 15.60% (15% + 4% EC) Earlier 19.24% Upto 1 Cr NO MAT NO MAT 16.69% 1 Cr 10 (15% + 7% SC + 4% EC) Earlier 20.59% NO MAT NO MAT 17.47% Above 10 Cr (15% + 12% SC + 4% EC) Earlier 21.55% NO MAT NO MAT

Form Of Business Particulars Tax (Considering Highest Rate) Partnership Firm 34.94% LLP 34.94% Company 25.17% (30% + 12% SC + 4% EC) 21.54% (30% + 12% SC + 4% EC) 21.54% (22% + 10% SC + 4% EC) NIL MAT/AMT (18.5% + 12% SC + 4% EC) (18.5% + 12% SC + 4% EC) 20.55% (17.65% grossed + 12% SC + 4% EC) DDT NIL NIL

Surcharge on capital gains The Finance (No 2) Act 2019, introduced increased surcharge at 25 % & 37 % of income- tax apply if the total income exceeds INR 2 Cr and INR 5 Cr, respectively. The Ordinance provides relief from the increased Surcharge in case of a FIIs as referred in section 115AD of the IT Act, in respect of income from capital gains arising on sale of securities. The surcharge rate in respect of capital gains covered by section 111A and section 112A of the IT Act capped at 15 %. The revised surcharge rate is tabulated hereunder: Income other than Capital gains covered under section 111A and section 112A Capital gains covered under section 111A and section 112A Total CG (INR) Upto 50 L 50L 1 Cr 1 Cr 2 Cr 2 Cr 5 Cr Above 5 Cr NIL 10% 15% 25% 37% NIL 10% 15% 15% 15%

Faceless Assessments Authorities - A National e-Assessment Centre to facilitate and centrally control the e-assessment. Regional e-Assessment Centres under the jurisdiction of the regional Principal Chief Commissioner for making assessment. Assessment units for identifying points or issues, material for the determination of any liability (including refund), analysing information, and such other functions. Verification units for enquiry, cross verification, examination of books of accounts, witness and recording of statements, and such other functions. Technical units for technical assistance including any assistance or advice on legal, accounting, forensic, information technology, valuation, transfer pricing, data analytics, management or any other technical matter. Review units for reviewing the draft assessment order to check whether the facts, relevant evidence and law and judicial decisions have been considered in the draft order. All the communications between all the units mentioned above, for the purpose of making an assessment under this scheme would be through the National e-Assessment Centre. The National e-Assessment Centre may at any stage of the assessment, if it considers necessary, transfer the case to the Assessing Officer having jurisdiction over such case

Grandfathering of Tax on Buy Back of Shares Change brought by FA 2019 u/s 115QA of IT Act - Individual has subscribed to a company in IPO stage at Rs.100/- The company announced a buyback at Rs 500 The company would pay the buyback tax at 20 % on Rs 400 Earlier The individual would have paid LTCG at 10% or STCG @ 15% on Rs 400 in listed companies. This amendment is effective from 5 July 2019. There were instances where public announcement for buy-back were made before 5 July 2019 but necessary approvals received post 5 July 2019. Such cases also came within the ambit of section 115QA of the IT Act and would be subject to buy-back tax. In order to give relief to such cases, the Ordinance has inserted a proviso to section 115QA of the IT Act to provide that the buy-back tax shall not apply to listed Companies where public announcement with respect to buy-back was made before 5 July 2019.

N No 72/2019 dated 23rdSep. CBDT notified the Income-tax Authorities which shall exercise and perform, concurrently, the powers and functions of Assessing Officer, to facilitate the conduct of E-assessment proceeding in a centralised manner in respect of returns furnished under Section 139 or in response to notice under Section 142 (1) during any financial year commencing on or after 1st day of April, 2018 All authorities are head quartered in New Delhi

N No 69/2019 dated 23rdSep. CBDT notifies Additional depreciation on motor Car and Motor vehicles i.e. 15% to 30% and 30% to 45% respectively, acquired on or after the 23rd day of August, 2019 but before the 1stday of April, 2020 and is put to use before the 1stday of April, 2020

N No 64/2019 dated 13thSep. CBDT notifies tolerance range for wholesale trading & for other cases for AY 19-20 w.r.t. the calculation of arm length price related to International transaction determined as per section 92C i.e. 1% in case of wholesale trading and 3% in other cases For the purposes of this notification, wholesale trading means an international transaction or specified domestic transaction of trading in goods, which fulfils the following conditions, namely:- (i) purchase cost of finished goods is eighty per cent. or more of the total cost pertaining to such trading activities; and (ii) average monthly closing inventory of such goods is ten per cent. or less of sales pertaining to such trading activities.

Cir 25/2019 Relaxation for Compounding CBDT as a one-time measure provides relaxation of time filling of compounding application, with a view to mitigate unintended hardship to taxpayers in deserving cases, and to reduce the pendency of existing prosecution cases before the courts

Cir 24/2019 Relaxation for Compounding CBDT lays down the procedure to identify & process Income Tax cases for prosecution in respect of certain Income Tax related offences such as Failure to pay tax to the credit of Central Government, Failure to pay the tax collected at Source, Wilful attempt to evade tax, etc. i. Offences u/s 276B: Failure to pay tax to the credit of Central Government under Chapter XII-D or XVII-B. ii. Offences u/s 276BB: Failure to pay the tax collected at Source iii. Offences u/s 276C(1): Wilful attempt to evade tax, etc. iv. Offences u/s 276CC: Failure to furnish returns of income.

Cir 23/2019 Non Filing of Appeals by Dept Appeal filing limit not applies to cases of Bogus LTCG / STCG-Exception to monetary limits for filing appeals specified in any Circular issued under Section 268A. Similar instructions has been issued vide instructions no. F. No. 279/Misc./M-93/2018-ITJ(Pt.) dated 16th September 2019. Appeals may be filed on merits as an exception to said circular, where Board, by way of special order direct filing of appeal on merit in cases involved in organised tax evasion activity

ITBA Inst 3: Regularizing of Manual Letters Any communication issued manually under the exceptional circumstances as mentioned has to be regularised within 15 working days of its issuance by (i) uploading the manual communication on the systems (ii) Compulsorily generating the DIN on the Systems (iii) Communicating the DIN so generated to the assessee/any other person as per electronically generated proforma available on the Systems

143(1) Not Issued Cases Functionality for processing of returns having refund claims which were not processed within the time allowed u/s 143(1) due to some technical or other reasons has been issued Pre-Conditions: (i) Valid return for the assessment years is filed under permitted time limit u/s 139 or 142(1). (ii) Assesse has claimed refund in return of income. (iii) On computation, the resultant outcome is refund. (iv) The returns of income should not have been remained unprocessed due to any reason attributable to the concerned assessee. (v) The returns of income should not be under Scrutiny assessment in view of provisions of sub- section (1D) of section 143 of the Act. Processes to be followed: (i) Prior administrative approval of concerned Pr.CCIT/CCIT must be obtained for processing of such eligible time- barred returns. (ii) Once administrative approval is accorded by the concerned PCCIT/CCIT, the concerned Pr.CIT/CIT would make reference to the Pr. DGIT (Systems), to provide necessary enablement in system to the assessing officer on case to case basis.

Office Memorandum: Sec 197 Certificate for NRIs Seeks to raise threshold of revenue effect for issue of certificates under section 197/195 needing approval of the CIT (Intl. Taxation) to Rs. 10 Crore. This threshold will be applicable for all stations in respect of all applications of non-resident taxpayers either pending as on date or filed hereafter.

Cir 17/2019 & 3/2018 : Limit for filing of appeals F. No.279/Misc/M-93/2018-ITJ No appeal shall be filed in respect of an assessment year or years in which the tax effect is less than the monetary limit specified in para 3. the revised monetary limits so mentioned is applicable, to all pending SLPs/ appeals/ cross objections/references. All such pending appeals within the revised limits shall be withdrawn on or before 31.10.2019 Appellate Forum Existing Monetary Limit Revised Monetary Limit Before ITAT 20,00,000 50,00,000 Before High Court 50,00,000 1,00,00,000 Before Supreme Court 1,00,00,000 2,00,00,000

THANK YOU E-mail- Vivek Jalan [FCA, LL.B, B.Com (H)] Vivek.jalan@taxconnect.co.in Call: +91 98315 94980 [ MUMBAI BANGALORE KOLKATA DELHI]

Not Issued Cases")