Lessons from March 2020 AQR Asset Management Institute

undefined

undefined

Anil Kashyap

External member of the Financial Policy Committee

T

h

e

D

a

s

h

f

o

r

C

a

s

h

a

n

d

t

h

e

L

i

q

u

i

d

i

t

y

M

u

l

t

i

p

l

i

e

r

:

L

e

s

s

o

n

s

f

r

o

m

M

a

r

c

h

2

0

2

0

A

Q

R

A

s

s

e

t

M

a

n

a

g

e

m

e

n

t

I

n

s

t

i

t

u

t

e

a

t

L

o

n

d

o

n

B

u

s

i

n

e

s

s

S

c

h

o

o

l

A

n

n

u

a

l

I

n

s

i

g

h

t

s

S

u

m

m

i

t

N

o

v

e

m

b

e

r

1

7

,

2

0

2

0

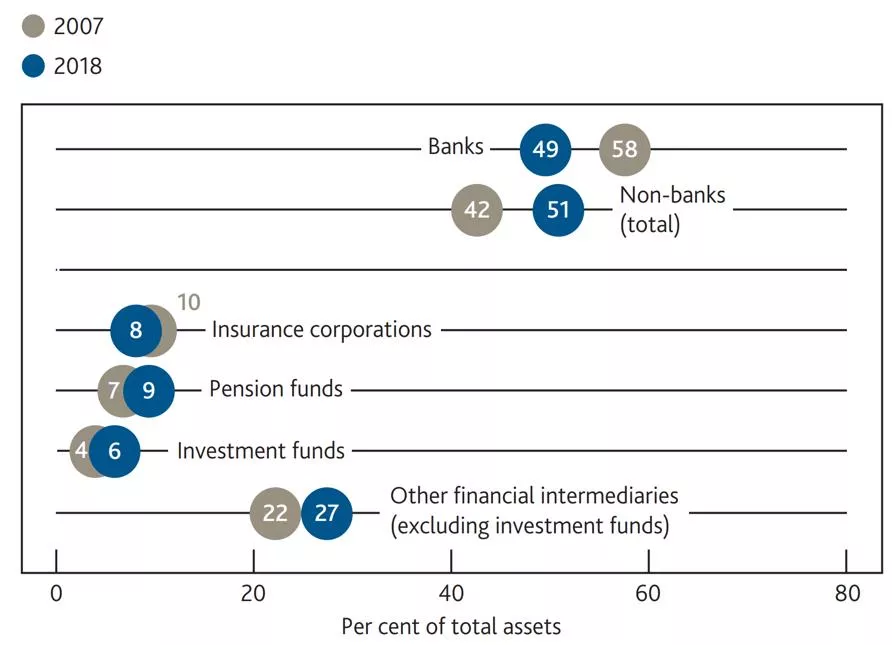

Figure 1: The share of non-bank UK financial sector assets has

grown over the past decade

Sources: The Association for Financial Markets in Europe, Bank of England, Bloomberg Finance L.P, FCA, Morningstar, ONS, published

accounts and Bank calculations. Please see the July 2019 Bank of England Financial Stability Report for full details.

Plan for the talk

1.

Funding chains

2.

The dash for cash drains on liquidity

3.

The liquidity multiplier

4.

Some open policy questions

A hypothetical market based finance funding chain

?

?

?

Figure 2: Bid-offer spreads

in selected gilts

Source: Eikon from Refinitiv and Bank calculations.

Figure 3: Changes in 10-

year nominal yields

Source: Bloomberg Finance L.P. and Bank calculations..

Figure 4: Variation margin on

centrally cleared derivatives

Source: Bank of England supervisory returns

Figure 5: Initial margin on

centrally cleared derivatives

Source: Bank of England supervisory returns

Figure 6: Weekly sterling MMF outflows

Sources: Crane data and Bank calculations

Note: Large inflows that occurred as a result of new funds being introduced to the sample have been removed.

Figure 7: Changes in repo stock from January 2020 average

Source: Bank of England Sterling Money Market data collection and Bank calculations

Note: For all gilt repo and reverse gilt repo maturities up to one year. Non-banks include: Hedge Funds, Pension Funds, Liability Driven

Investment Asset Managers, and Insurers

Figure 8: Stylised pension fund chain

Figure 9:

Defensive actions taken by parties in the chain

Some open questions

1.

Does the regulatory system addresses these challenges adequately?

2.

What will be expected of central banks in future stress episodes?

•

Is there a way to charge the beneficiaries of the support for the liquidity insurance that central banks are

providing ex-post?

3.

Can we make a map of the most important funding chains so that we can

monitor them and potentially catch problems before they appear?

Questions?

Anil Kashyap

External member of the Financial Policy Committee

References

On the FPC:

On the Dash for Cash

‘Come with me to the FPC’, Speech by Anil Kashyap given at the Official Monetary and Financial

Institutions Forum, 13 June 2018.

‘My Reflections on the FPC’s Strategy” Speech by Anil Kashyap at the “50th Anniversary of the Journal

of Money, Credit and Banking, Frankfurt, 28

th

March 2019.

‘Seven Moments in Spring

’

, Speech by Andrew Hauser, 4 June 2020

‘

Financial System Resilience

’

, Speech by Jon Cunliffe, 9 June 2020.

‘The impact of leveraged investors on market liquidity and financial stability

’, Speech by

Jon Cunliffe, 12

November 2020.

A look at the effects of the "dash for cash" and liquidity multiplier in the UK financial sector, discussing funding chains, liquidity issues, and policy implications raised during the November 2020 Insights Summit.

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

You are allowed to download the files provided on this website for personal or commercial use, subject to the condition that they are used lawfully. All files are the property of their respective owners.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author.

E N D

Presentation Transcript

The Dash for Cash and the Liquidity Multiplier: Lessons from March 2020 AQR Asset Management Institute at London Business School Annual Insights Summit November 17, 2020 Anil Kashyap External member of the Financial Policy Committee

Figure 1: The share of non-bank UK financial sector assets has grown over the past decade Sources: The Association for Financial Markets in Europe, Bank of England, Bloomberg Finance L.P, FCA, Morningstar, ONS, published accounts and Bank calculations. Please see the July 2019 Bank of England Financial Stability Report for full details.

Plan for the talk 1. Funding chains 2. The dash for cash drains on liquidity 3. The liquidity multiplier 4. Some open policy questions

A hypothetical market based finance funding chain Repo Repo Pension fund Money market fund Hedge fund Broker-dealer ? ? ? Bank deposits

Figure 2: Bid-offer spreads in selected gilts Figure 3: Changes in 10- year nominal yields Source: Eikon from Refinitiv and Bank calculations. Source: Bloomberg Finance L.P. and Bank calculations..

Figure 4: Variation margin on centrally cleared derivatives Figure 5: Initial margin on centrally cleared derivatives Source: Bank of England supervisory returns Source: Bank of England supervisory returns

Figure 6: Weekly sterling MMF outflows Sources: Crane data and Bank calculations Note: Large inflows that occurred as a result of new funds being introduced to the sample have been removed.

Figure 7: Changes in repo stock from January 2020 average Source: Bank of England Sterling Money Market data collection and Bank calculations Note: For all gilt repo and reverse gilt repo maturities up to one year. Non-banks include: Hedge Funds, Pension Funds, Liability Driven Investment Asset Managers, and Insurers

Some open questions 1. Does the regulatory system addresses these challenges adequately? 2. What will be expected of central banks in future stress episodes? Is there a way to charge the beneficiaries of the support for the liquidity insurance that central banks are providing ex-post? 3. Can we make a map of the most important funding chains so that we can monitor them and potentially catch problems before they appear?

Questions? Anil Kashyap External member of the Financial Policy Committee

References On the FPC: Come with me to the FPC , Speech by Anil Kashyap given at the Official Monetary and Financial Institutions Forum, 13 June 2018. My Reflections on the FPC s Strategy Speech by Anil Kashyap at the 50th Anniversary of the Journal of Money, Credit and Banking, Frankfurt, 28th March 2019. On the Dash for Cash Seven Moments in Spring , Speech by Andrew Hauser, 4 June 2020 Financial System Resilience , Speech by Jon Cunliffe, 9 June 2020. The impact of leveraged investors on market liquidity and financial stability , Speech by Jon Cunliffe, 12 November 2020.