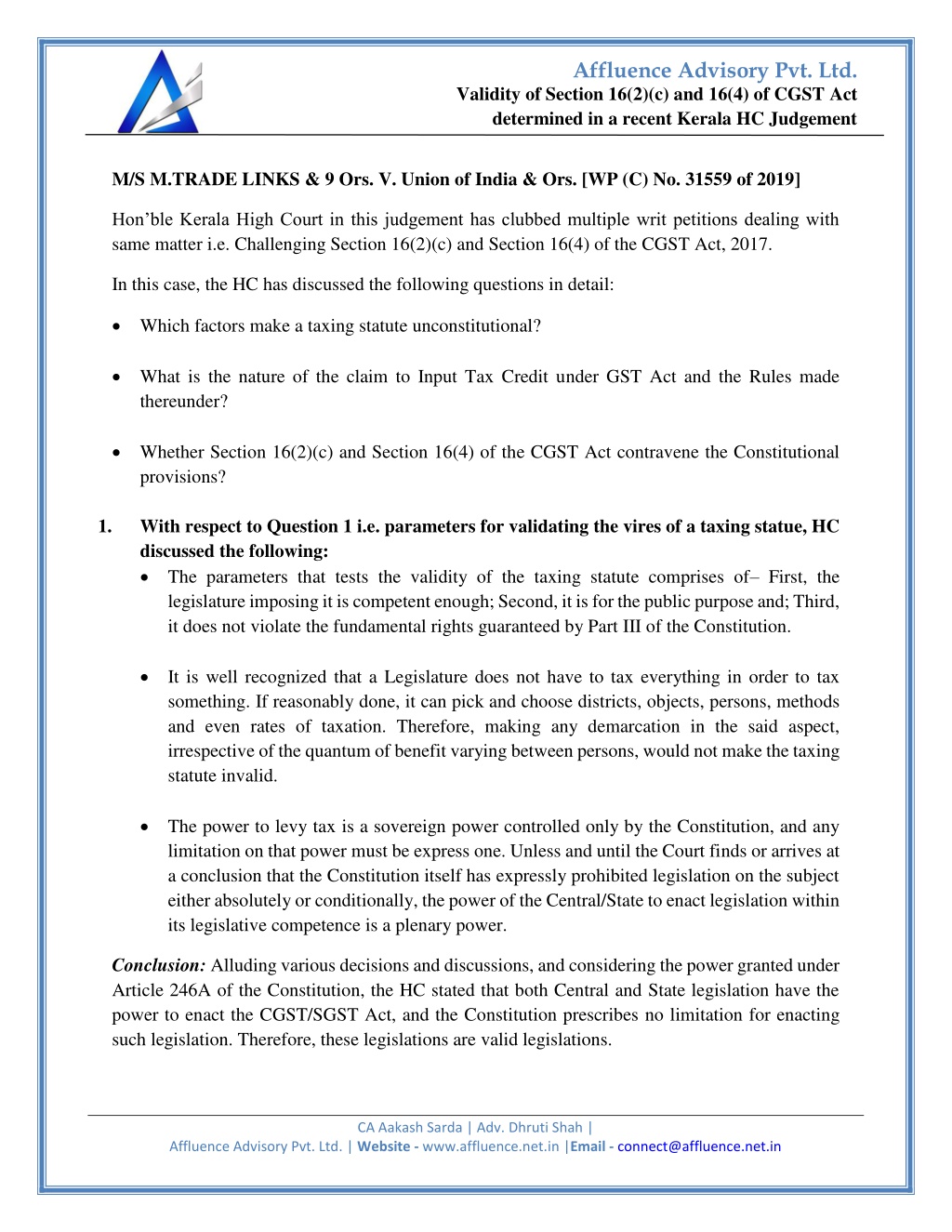

Validity of Section 16(2)(c) and 16(4) of CGST Act determined in HC Judgement

The Kerala High Court upheld Sections 16(2)(c) and 16(4) of the CGST Act, affirming their constitutional validity. The court ruled that Input Tax Credit (ITC) is a conditional entitlement, not an absolute right. The judgement emphasized the importance of the statutory scheme, rejecting challenges to the provisions' validity.

- Kerala HC

- CGST Act

- Section 16(2)(c)

- Section 16(4)

- Input Tax Credit

- GST law

- constitutional validity

- tax statute

- ITC conditions

- GST amendments

- CGST ruling

- tax compliance

- tax legislation

- HC judgement

- tax law update

- GST provisions

- ITC claims

Download Presentation

Please find below an Image/Link to download the presentation.

The content on the website is provided AS IS for your information and personal use only. It may not be sold, licensed, or shared on other websites without obtaining consent from the author. Download presentation by click this link. If you encounter any issues during the download, it is possible that the publisher has removed the file from their server.

Presentation Transcript

Affluence Advisory Pvt. Ltd. Validity of Section 16(2)(c) and 16(4) of CGST Act determined in a recent Kerala HC Judgement M/S M.TRADE LINKS & 9 Ors. V. Union of India & Ors. [WP (C) No. 31559 of 2019] Hon ble Kerala High Court in this judgement has clubbed multiple writ petitions dealing with same matter i.e. Challenging Section 16(2)(c) and Section 16(4) of the CGST Act, 2017. In this case, the HC has discussed the following questions in detail: Which factors make a taxing statute unconstitutional? What is the nature of the claim to Input Tax Credit under GST Act and the Rules made thereunder? Whether Section 16(2)(c) and Section 16(4) of the CGST Act contravene the Constitutional provisions? 1. With respect to Question 1 i.e. parameters for validating the vires of a taxing statue, HC discussed the following: The parameters that tests the validity of the taxing statute comprises of First, the legislature imposing it is competent enough; Second, it is for the public purpose and; Third, it does not violate the fundamental rights guaranteed by Part III of the Constitution. It is well recognized that a Legislature does not have to tax everything in order to tax something. If reasonably done, it can pick and choose districts, objects, persons, methods and even rates of taxation. Therefore, making any demarcation in the said aspect, irrespective of the quantum of benefit varying between persons, would not make the taxing statute invalid. The power to levy tax is a sovereign power controlled only by the Constitution, and any limitation on that power must be express one. Unless and until the Court finds or arrives at a conclusion that the Constitution itself has expressly prohibited legislation on the subject either absolutely or conditionally, the power of the Central/State to enact legislation within its legislative competence is a plenary power. Conclusion: Alluding various decisions and discussions, and considering the power granted under Article 246A of the Constitution, the HC stated that both Central and State legislation have the power to enact the CGST/SGST Act, and the Constitution prescribes no limitation for enacting such legislation. Therefore, these legislations are valid legislations. CA Aakash Sarda | Adv. Dhruti Shah | Affluence Advisory Pvt. Ltd. | Website - www.affluence.net.in |Email - connect@affluence.net.in

Affluence Advisory Pvt. Ltd. Validity of Section 16(2)(c) and 16(4) of CGST Act determined in a recent Kerala HC Judgement 2. With respect to Question 2 i.e. nature of claim related to ITC under GST, the HC discussed the following: The claim to Input Tax Credit is not an absolute right, but it can be termed as an entitlement; however, the entitlement is subject to conditions and restrictions as envisaged in the provisions of the GST Act and corresponding Rules made thereunder. Conclusion: Although, the learned counsels for the petitioners contended that Section 16(1) of the GST Act provides an absolute right to claim Input Tax Credit which cannot be taken away by way of conditions in Section 16 (2) of the CGST Act. However, HC held that ITC is in nature of a benefit or concession extended under the statutory scheme and the rule-making authority is empowered to provide for abridgement or curtailment while extending a concession. Thus, the ITC claim shall be allowed subject to the conditions and restrictions as envisaged in Sections 16(2) of CGST Act. 3. With respect to Question 3 i.e. vires of Section 16(2) (c) and Section 16(2)(4) of CGST Act, the Court discussed the following: GST is a destination-based consumption tax with ITC available on payment of tax on supply of goods or services at each stage which can be availed in the next stage of supply chain, thereby removing cascading effect. The same is irrespective of the destination, be it an intra- state or inter-state supply. The Input tax credit plays a major role in determining the tax collection. Thus, consideration of tax credits at such large scale cannot be allowed to linger on indefinitely which would have a direct effect on the tax collection, estimates and budgetary allocations and in turn, revenue deficit. Section 53 of the CGST Act wherein the statutory obligation of the Central and State Governments is prescribed with respect to transfer of credit. Considering a scenario without Section 16(2)(c) of CGST Act, where a supplier in the originating State defaults in payment of tax and the recipient supplier is allowed to take credit based on their invoice, the originating State Government will have to transfer the amounts it never received in the tax period in a financial year to the destination State, causing loss to the tune of several crores in each tax period, thus rendering the whole GST law unworkable. Further, drawing a comparison between the provisions applicable post amendment i.e. w.e.f 01.01.2022 and period prior to that, HC (realizing the difficulty in the initial stage of GST era) CA Aakash Sarda | Adv. Dhruti Shah | Affluence Advisory Pvt. Ltd. | Website - www.affluence.net.in |Email - connect@affluence.net.in

Affluence Advisory Pvt. Ltd. Validity of Section 16(2)(c) and 16(4) of CGST Act determined in a recent Kerala HC Judgement held that for period prior to the amendment from 1.01.2022, petitioner was granted liberty to claim benefit of the two Circulars, namely, Circular No. 183/15/2022- GST dated 27.12.2022 and Circular No. 193/05/2023- GST dated 17.07.2023 to make ITC claim before the appropriate authority who shall examine the same and process it. With respect to the amendment to Section 39 of the CGST Act which extended the return filing date from 30 September to 30 November, HC held that the amendment being procedural has to be given retrospective effect and, therefore w.e.f 1.07.2017, the petitioners who had filed their returns for the month of September on or before 30th November should be allowed ITC, if they are otherwise eligible for ITC. Also, while interpreting a statute one has to consider the meaning behind the context and the scheme of the statute. Mere text cannot be read in isolation. Further, Section 16(2) is the restriction on eligibility and Section 16(4) is the restriction on the time for availing ITC. These provisions cannot be read to restrict other restrictive provisions, i.e., Section 16(3) and 16(4). Therefore, the challenge to the constitutional validity of Section 16(2) (c) and Section 16(4) of the CGST Act cannot be sustained and thus, rejected. Disclaimer:This article provides general information existing at the time of preparation and we take no responsibility to update it with the subsequent changes in the law. The article is intended as a news update and Affluence Advisory neither assumes nor accepts any responsibility for any loss arising to any person acting or refraining from acting as a result of any material contained in this article. It is recommended that professional advice be taken based on specific facts and circumstances. This article does not substitute the need to refer to the original pronouncement CA Aakash Sarda | Adv. Dhruti Shah | Affluence Advisory Pvt. Ltd. | Website - www.affluence.net.in |Email - connect@affluence.net.in